Mortgage Rates Today: How to Compare Current and Average Mortgage Rates Before You Buy

Mortgage Rates Today Mortgage rates today can have a major impact on how much homebuyers pay each month and over the life of a loan. …

Mortgage Rates Today Mortgage rates today can have a major impact on how much homebuyers pay each month and over the life of a loan. …

Mortgage Rates in Utah: Everything YouNeed to Know Before Buying a HomePurchasing a home is one of the biggest financial decisions you’ll ever make, andunderstanding …

Choosing the right mortgage lender Salt Lake City homebuyers can trust is one of the most important decisions you’ll make when purchasing your first home. …

After more than two decades working in Utah’s mortgage industry, I’ve learned that the buyers who do well here aren’t the ones who time the …

When buyers search for interest rates today, they are usually looking for more than just a number. They want to know whether buying a home …

Introduction Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step …

The dream of owning a home in the Beehive State is more achievable than many realize, especially with the current Utah housing market forecast 2026 …

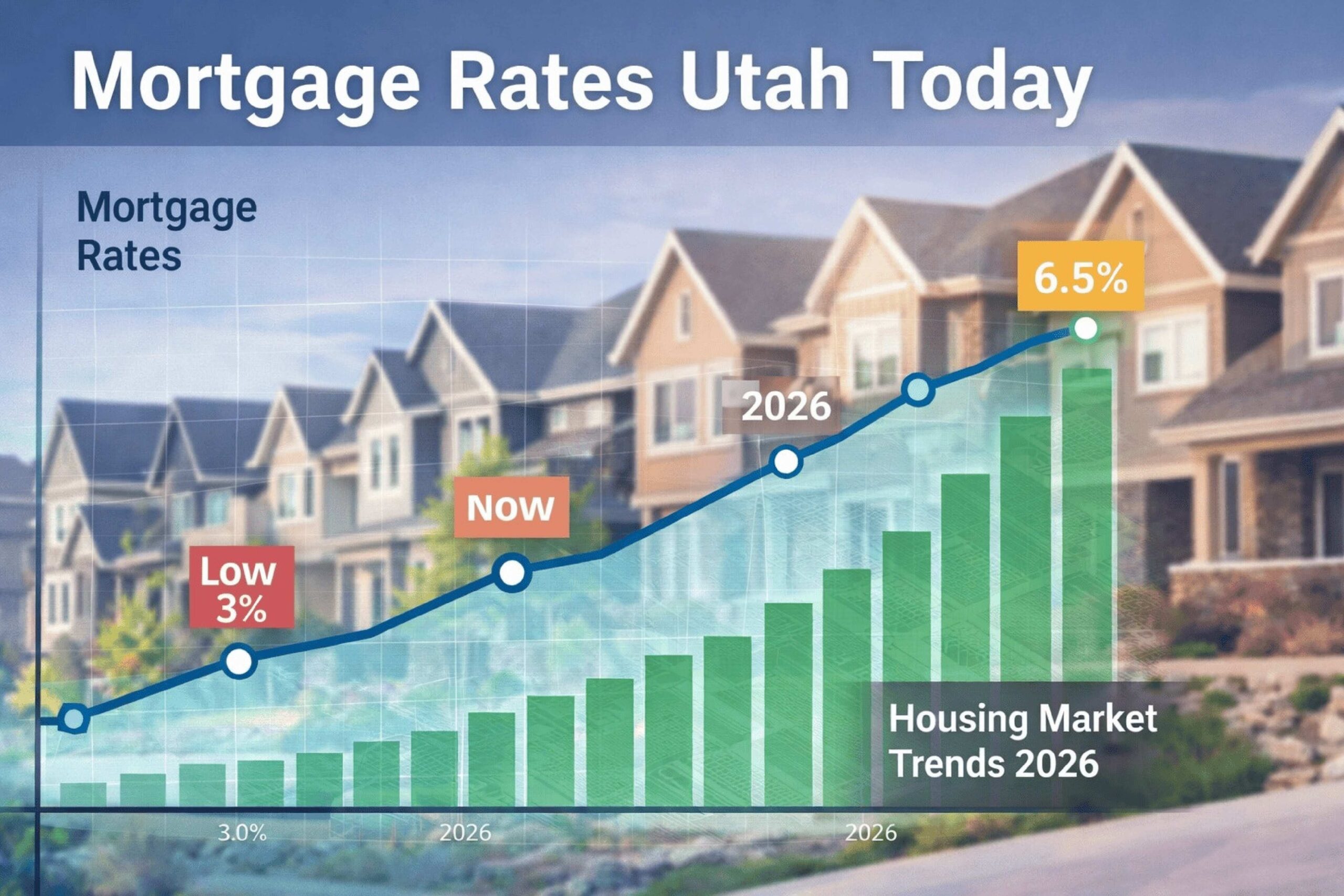

If you’re monitoring mortgage rates today in Utah, you’re likely trying to understand how current mortgage rates impact what you can afford. In Utah’s fast-moving …

Navigating the 2026 real estate market requires more than just a passing interest in home listings; it requires a fortified financial strategy. As home prices …

What Is a First Time Home Buyer Utah Loan? Buying your first home can feel overwhelming, especially when it comes to understanding loan options. A …