If you have a VA home loan and interest rates have dropped since you closed, you have probably run into the term and wondered, what is a VA IRRRL? Short for Interest Rate Reduction Refinance Loan, it is the Department of Veterans Affairs’ fast-track refinance, much better known as the va streamline refinance. The honest “what is va irrrl program” answer is refreshingly simple: it lets veterans and service members swap an existing VA loan for a new one at a lower rate, with fard less paperwork and cost than a normal refinance. This guide walks through how the loan works, who qualifies, what it costs, and how to decide whether a va home loan refinance is the right move for you.

How Does a VA IRRRL Work?

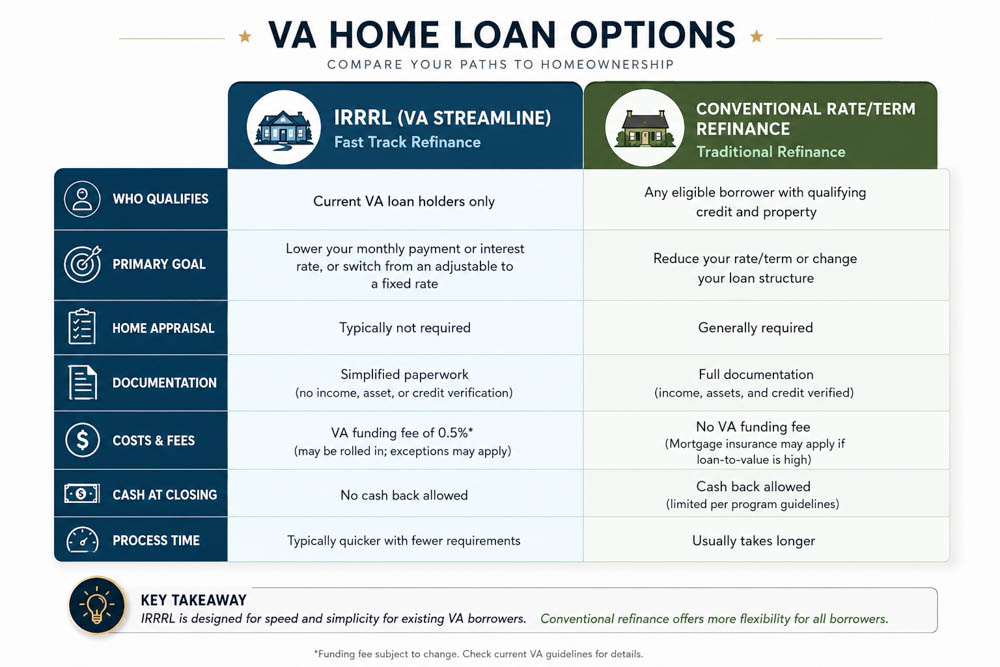

Here is how does va irrrl work in everyday terms. A va irrrl refinance simply replaces your current VA mortgage with a brand-new VA loan on better terms. Because the VA already guarantees your original loan, a va loan refi through this program skips most of the friction of a traditional va mortgage refinance. In the majority of cases there is no new appraisal, no income verification, and no fresh credit pull. On top of that, the closing costs can be folded straight into the new balance, so plenty of veterans refinance with little or nothing out of pocket. From application to funding, the whole process often wraps up in just two to three weeks.

VA IRRRL Eligibility Requirements

One of the best parts of this program is that the va irrrl eligibility requirements are some of the simplest in the entire mortgage world. To start, you must already hold a VA-backed loan, since the IRRRL exists only to refinance an existing one. Beyond that, the irrrl refinance requirements are short and clear: at least six consecutive on-time monthly payments, a minimum of 210 days since your first payment came due, and a genuine benefit from the new loan, such as a lower interest rate or a switch from an adjustable rate to a fixed one. Most lenders can confirm your eligibility in a single phone call.

Key Benefits of the VA Streamline Refinance

A handful of features make the va streamline refinance especially appealing. Because most IRRRLs skip the appraisal, you can often refinance even if your home value has slipped or you owe close to what it is worth. There is no monthly mortgage insurance on a VA loan, the funding fee is small, and you are never tied to your current servicer, so you are free to shop for the best terms. For many households, it is simply the quickest and most affordable way to trim a monthly payment.

VA IRRRL Rates Today

For most veterans, the decision really comes down to the numbers, which is why va irrrl rates get all the attention. Just like any mortgage, irrrl rates today move with the bond market, so the current irrrl rates a lender quotes you in the morning may not survive until closing. As a rough benchmark, va streamline refinance rates today in early 2026 have hovered in the high-5 percent range on a 30-year term, though your own va refi rates today will always depend on your lender, your loan balance, and the term you choose. The smartest habit is to gather several va irrrl refinance rates on the very same day, because irrrl refinance rates can differ noticeably from one lender to the next.

When you do compare, weigh the entire quote rather than fixating on one headline number. Putting va refinance rates, va streamline refinance rates, and va loan refinance rates side by side gives you a much truer picture of the real cost. A shorter term usually brings lower va refi rates but a higher monthly payment, while a 30-year term keeps va loan refi rates and va home loan refi rates more affordable by spreading the savings across more years. It also helps to review our regularly updated Utah VA refinance rates (internal link) before you apply, so you walk in knowing roughly where the market sits.

Costs and the VA Funding Fee

A VA IRRRL is inexpensive, but it is not quite free. The VA charges a streamline funding fee of just 0.5 percent of the loan amount, far below the fee attached to a purchase or cash-out loan. Better still, many veterans pay nothing at all thanks to the va irrrl funding fee exemption, which covers borrowers receiving VA disability compensation as well as certain surviving spouses. The usual closing costs, such as title and recording fees, still apply, but in most cases they can be rolled neatly into the loan.

Run the Numbers with an IRRRL Calculator

Before you commit, spend a few minutes with an irrrl refinance calculator. A good one compares your current payment against the projected new payment, factors in the closing costs, and then shows your break-even point, the month when your accumulated savings finally outweigh everything the refinance cost you. If you plan to stay in the home beyond that point, the math almost always works in your favor.

Choosing the Best VA IRRRL Lenders

Rates and service can vary widely, so it genuinely pays to shop for the best va irrrl lenders rather than simply defaulting to your current one. Collect quotes on the same day, ask each lender about available credits, and make sure no junk fees are quietly padding the estimate. For program details straight from the source, the VA’s official Interest Rate Reduction Refinance Loan page (external link) is well worth a read. Utah veterans in particular tend to find that a knowledgeable local team makes the entire process faster and smoother.

Is a VA IRRRL Right for You?

If today’s rates sit below the rate on your current VA loan, a streamline refinance is one of the easiest ways to free up money every single month. It is fast, low-cost, and designed specifically for those who have served. Reach out to our Utah team for a no-obligation quote and find out exactly what you could save.