Mortgage Rates Today

Mortgage rates today can have a major impact on how much homebuyers pay each month and over the life of a loan. Even a small change in a mortgage rate can affect your monthly payment, your buying power, and the total cost of your home. For first-time buyers especially, understanding how rates work can make the homebuying process feel less overwhelming and help you make smarter financial decisions.

When people search for current mortgage rates, they are usually trying to answer one main question: “Is now a good time to buy?” The answer depends on more than just the number you see online. Rates are influenced by the economy, inflation, lender requirements, credit scores, loan types, and the overall housing market. That is why it is important to look beyond one advertised rate and understand what actually affects your personal loan offer.

Average Mortgage Rates

Average mortgage rates give homebuyers a general idea of where the market stands, but they are not the exact rate every borrower will receive. An average rate is usually based on national lending data and can change daily. However, your individual rate may be higher or lower depending on your financial profile, including your credit score, income, debt, loan amount, and down payment.

Many buyers compare average mortgage rate information to see if rates are rising or falling. This can be helpful, but it should only be a starting point. For example, two people buying similar homes may receive different rates because one has a higher credit score or a larger down payment. Instead of relying only on national averages, buyers should use averages to understand the market and then compare personalized loan estimates from multiple lenders.

Current Mortgage Rates

Current mortgage rates are the rates lenders are offering right now. These rates can change quickly based on economic news, inflation reports, Federal Reserve decisions, bond market activity, and lender competition. Because rates move often, buyers should check mortgage interest rates today when they are actively shopping for a home or preparing to lock in a loan.

Looking at home loan rates today can help buyers decide whether they want to move forward, wait, or explore different loan options. However, buyers should remember that the rate shown online is often a sample rate. The actual rate offered may depend on the borrower’s finances and the details of the loan.

Mortgage Rates 30 Years Fixed

One of the most common loan options is the 30-year fixed mortgage. When buyers search for mortgage rates 30 years fixed or 30 year mortgage rates today, they are usually looking for a predictable monthly payment. A fixed-rate mortgage keeps the same interest rate for the entire loan term, which makes budgeting easier.

The main advantage of a 30-year fixed mortgage is that the payments are usually lower than shorter-term loans because the cost is spread over a longer period. The downside is that borrowers may pay more interest over time. Still, many buyers choose this option because it provides stability and flexibility.

Home Loan Interest Rates

Home loan interest rates are one of the biggest factors in determining the cost of buying a home. A lower interest rate can reduce monthly payments and save thousands of dollars over the life of the loan. A higher rate can make the same home much more expensive.

This is why buyers should compare mortgage rates from several lenders before choosing a loan. Different lenders may offer different rates, fees, and loan terms. Comparing options can help buyers find the best mortgage rates available for their situation.

How to Get the Best Mortgage Rate

Learning how to get the best mortgage rate starts with improving your financial profile. Lenders usually offer better rates to borrowers with strong credit, stable income, manageable debt, and larger down payments. Before applying for a mortgage, buyers should check their credit report, pay down high-interest debt, avoid opening new credit accounts, and save as much as possible for upfront costs.

Buyers looking for the lowest mortgage rates should also shop around. Getting quotes from multiple lenders can reveal meaningful differences in pricing. One lender may offer a lower rate, while another may have lower fees. The best deal is not always the lowest rate alone. Buyers should compare the full cost of the loan, including interest, fees, closing costs, and monthly payment.

Mortgage Rate Calculator

A mortgage rate calculator can help buyers estimate how different interest rates affect monthly payments. This tool is useful because it lets buyers test different scenarios before committing to a loan. For example, a buyer can compare how their payment changes with a lower interest rate, larger down payment, or different loan term.

A mortgage payment calculator is also helpful for understanding the full monthly cost of homeownership. In addition to principal and interest, a mortgage payment may include property taxes, homeowners insurance, and private mortgage insurance. Looking at the full payment gives buyers a more realistic picture of affordability.

Mortgage Points

Mortgage points are optional upfront fees that buyers can pay to lower their interest rate. One point typically costs a percentage of the loan amount. Paying points can make sense for buyers who plan to stay in their home for a long time because the monthly savings may eventually outweigh the upfront cost.

However, points are not always the best choice. Buyers should calculate the break-even point before paying for them. If someone plans to sell or refinance soon, paying points may not save enough money to be worth it.

Rate Lock

A rate lock allows a borrower to secure an interest rate for a specific period while the loan is being processed. This can protect buyers if rates increase before closing. Rate locks are especially useful when housing market rates are changing quickly.

However, buyers should understand the terms of the lock. Some rate locks expire after a certain number of days, and extending them may cost extra. Before locking a rate, buyers should ask their lender about the lock period, extension fees, and whether they can access a lower rate if rates fall.

Down Payment Assistance

Down payment assistance can help eligible buyers cover part of their upfront homebuying costs. These programs may be offered by state agencies, local governments, nonprofits, or lenders. Assistance may come in the form of grants, forgivable loans, or low-interest second loans.

For first-time buyers, mortgage assistance programs can make homeownership more realistic. Buyers should research programs in their area and ask lenders if they work with assistance programs. For example, buyers searching for mortgage rates Utah may also want to look for Utah-specific down payment support and first-time buyer programs.

Piggyback Loan

A piggyback loan is a second loan used alongside a primary mortgage. Some buyers use piggyback loans to avoid private mortgage insurance or reduce the size of their first mortgage. This strategy can be helpful in certain situations, but it also means managing two loans instead of one.

Before choosing a piggyback loan, buyers should compare the total monthly payment, interest rates, and long-term costs. Sometimes private mortgage insurance is less expensive than taking on a second loan.

Bridge Loan

A bridge loan is a short-term loan that helps homeowners buy a new home before selling their current one. This can be useful in competitive markets where buyers need to move quickly. However, bridge loans can come with higher costs and more risk because the borrower may temporarily carry multiple payments.

Buyers considering a bridge loan should talk with a lender about repayment timelines, fees, and whether they have enough financial flexibility.

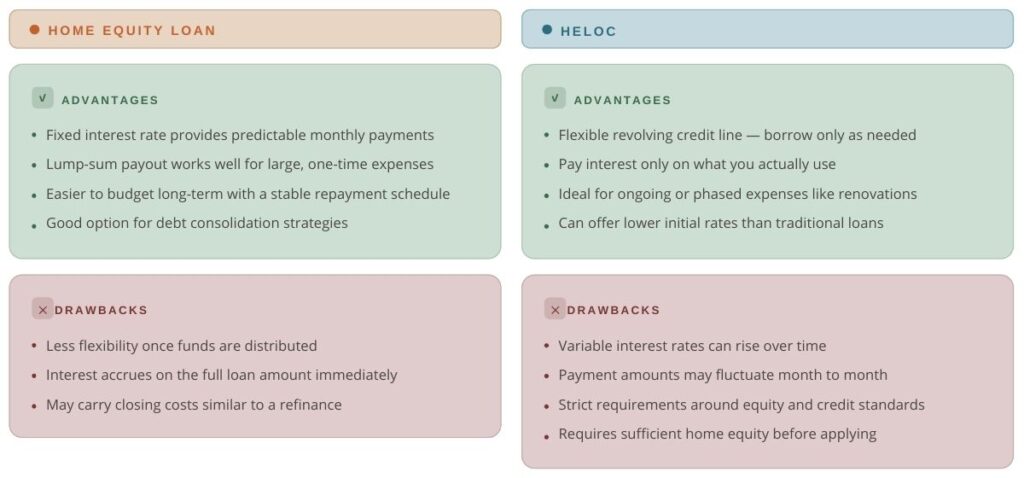

Home Equity Loan Rates

Home equity loan rates matter for homeowners who want to borrow against the value of their home. While this is different from a purchase mortgage, it is still connected to the broader interest rate environment. When mortgage rates rise, home equity loan rates may also increase.

Homeowners may use home equity loans for renovations, debt consolidation, or major expenses. However, since the home is used as collateral, borrowers should be careful and only borrow what they can afford to repay.

Final Thoughts

Understanding mortgage rates today is about more than checking one number online. Buyers should compare current mortgage rates, review average mortgage rates, use a mortgage rate calculator, and understand loan tools like mortgage points, rate locks, and private mortgage insurance. They should also explore options like down payment assistance, mortgage assistance, piggyback loans, and bridge loans when appropriate.

The best mortgage decision depends on your personal finances, your location, and your long-term goals. By comparing lenders, understanding your options, and using tools like a mortgage payment calculator, you can make a more confident choice and find a home loan that fits your budget.