A Home equity line of credit can be one of the most flexible financing options available for Utah homeowners. Instead of refinancing your mortgage, a HELOC allows you to borrow against the equity you’ve already built in your home. Whether you’re planning renovations, consolidating debt, or funding a large expense, understanding your options is essential before applying.

Home Equity Line of Credit Interest Rates and Utah HELOC Rates

One of the first questions homeowners ask is about Home equity line of credit interest rates. Rates vary depending on your credit profile, available equity, lender, and current market conditions. Many Utah borrowers compare HELOC interest rates today with HELOC rates Utah to determine whether local lenders offer more competitive financing.

A HELOC calculator can help estimate monthly payments before applying. Some homeowners also prefer a Fixed rated HELOC, which offers greater payment stability than a variable-rate line of credit.

HELOC Requirements and the Application Process

Before applying, borrowers should understand common HELOC requirements and HELOC credit score requirements. Most lenders review available equity, income, debt-to-income ratio, and credit history before making an approval decision.

The HELOC application process generally includes submitting financial documents, verifying home ownership, and completing a property valuation. Some borrowers specifically search for HELOC lenders with no appraisal to simplify the process.

Borrowers should also compare HELOC closing costs, since lender fees can vary significantly.

Comparing the best HELOC Lenders

Finding the Best HELOC lenders involves more than simply comparing interest rates. Homeowners frequently search for the Best HELOC lenders near me, Best online HELOC lenders, Best HELOC lenders Utah, and Best HELOC lenders no closing costs to identify the best combination of rates, fees, and customer service.

Reading HELOC lender reviews and considering Credit union HELOC lenders can help borrowers make informed decisions. It is always recommended to Compare HELOC lenders before selecting one.

HELOC vs Cash Out Refinance

Choosing between a HELOC vs cash out refinance depends on your financial goals. A HELOC keeps your existing mortgage while providing a revolving line of credit. A cash-out refinance replaces your mortgage with a larger loan.

For homeowners planning renovations, a HELOC for home improvements is often an attractive option because funds can be borrowed as needed.

Borrowers should also understand whether they qualify for a HELOC tax deduction, which may apply when funds are used for eligible home improvements.

Using a HELOC for Investment Property

Some lenders offer a Home equity line of credit on investment property, although qualification standards are typically stricter than those for a primary residence. Working with experienced Investment property HELOC lenders can help investors finance renovations, property improvements, or future purchases.

Buying a home in Utah is exciting, but it can also feel confusing if you are not sure where to begin. Before you spend weekends touring homes or comparing neighborhoods, it helps to understand how to get pre-approved for a home loan online. Mortgage pre-approval gives you a clearer idea of your price range. It can also help you understand your estimated monthly payment and loan options before you make an offer. For first-time buyers, it can also make the entire home search feel more realistic because you are no longer guessing what you can afford.

Many buyers start with basic questions like how to get pre-approved for a home loan, how to get pre-approved for a house loan, or how can I get pre-approved for a home loan. These questions all point to the same goal: getting a lender to review your financial picture before you buy. A pre-approval is not the same thing as a casual online mortgage calculator. It usually requires a lender to review your income, credit, debt, assets, and down payment funds so they can estimate what loan amount you may qualify for.

How to Get Pre-Approved for a Mortgage Loan

The first step is choosing a lender or mortgage professional who can review your situation and explain your options. If you are wondering how to get preapproval for a home loan, the process usually starts with a mortgage application. You will provide basic personal information, employment details, income history, debt information, and permission for the lender to check your credit.

From there, the lender may request documents such as pay stubs, W-2s, tax returns if you are self-employed, bank statements, and identification. These documents help verify that the information on your application is accurate. If you have savings for a down payment or closing costs, the lender may also ask for proof of those funds.

A common question is how can I get preapproved for a mortgage if I have never bought a home before? The answer is to start early and be honest about your finances. First-time buyers sometimes worry that they need to have everything perfect before talking to a lender. In reality, a good mortgage professional can help you understand what is strong, what needs work, and what loan programs might fit your situation.

If you are searching for how to get pre-approved for a mortgage loan, you are probably trying to understand whether you are financially ready to buy. Lenders look at several major factors, including credit score, income, debt-to-income ratio, employment stability, available cash, and the type of property you want to buy. If you are comparing Utah mortgage rates, it also helps to understand how pre-approval fits into your budget before you start shopping.

Another related search is how to get preapproval for a mortgage. The word “preapproval” may sound formal, but the idea is simple. A lender is trying to answer this question: based on the information available, how much mortgage financing might this buyer qualify for? That answer can help you avoid shopping too high or too low.

Some buyers also ask how to get pre-approved for a home mortgage because they want to know whether the process is different for a primary residence. In most cases, buying a home to live in is the standard mortgage scenario. The lender will still review your income, debts, assets, and credit, but they may also discuss loan types such as conventional, FHA, VA, or other programs that could apply to Utah buyers.

Getting Pre-Approved Online in Utah

One of the biggest advantages for today’s buyers is that much of the process can be handled digitally. If you want to get pre-approved for mortgage online, you can often complete an application, upload documents, and communicate with your loan officer without going into an office. This is helpful for busy Utah buyers who are working full time, managing family schedules, or trying to move quickly in a competitive market.

You can also get pre-approved for a home loan online through banks, credit unions, online lenders, mortgage brokers, or local mortgage professionals. The key is not just speed. The key is getting accurate information and clear guidance. A fast online letter is not very useful if you do not understand the payment, rate, estimated closing costs, or conditions that still need to be met.

If you are researching how to get pre-approved for a mortgage online, gather your documents before you apply. This can make the process smoother and reduce back-and-forth requests. You should also be ready to answer questions about your employment, income type, monthly debt, savings, and timeline for buying.

Where to Get Pre-Approved for a Mortgage in Utah

Buyers often ask where to get pre-approved for a mortgage because there are so many options. You can start with your current bank, a credit union, an online lender, a mortgage broker, or a local Utah mortgage specialist. Each option may offer different rates, fees, programs, and service levels.

If you are wondering where to get preapproved for a home loan, think beyond the company name. The right lender should explain the process clearly, respond quickly, and help you understand what your numbers mean. This matters because the lowest advertised rate is not always the full story. Closing costs, loan terms, lender fees, and communication can all affect your experience.

Many first-time buyers also search for where can I get pre-approved for a home loan because they are not sure whether they should apply with one lender or compare several options. It is usually reasonable to compare lenders, especially if you are trying to understand the difference between rates, fees, and loan programs. Just make sure you compare similar loan types and ask each lender the same questions.

Another version of the same question is where can I get preapproved for a mortgage. For Utah buyers, a local lender may be especially helpful because they understand the local housing market, common property types, and the pace of offers in different areas. National lenders can still be useful, but local experience can make the process feel more personal and practical.

Timing is one of the most important parts of the process. If you are asking when to get pre-approved for a home loan, the best answer is usually before you seriously start shopping. You do not necessarily need a pre-approval if you are casually browsing homes online, but once you are ready to tour properties or make an offer, pre-approval becomes much more important.

A lot of buyers ask when should I get pre-approved for a mortgage because they worry about applying too early. Pre-approval letters may expire after a period of time, but starting early can still be helpful. If there are issues with your credit, debt, income documentation, or savings, it is better to find out before you are under pressure to make an offer.

Similarly, if you are wondering when should I get pre-approved for a home loan, a good rule is to talk with a lender when you are within a few months of buying. This gives you time to understand your budget, compare loan options, and fix any problems that could slow you down later.

The question of when should you get pre-approved for a mortgage also depends on your local market. In a competitive Utah market, sellers may take your offer more seriously if you already have a pre-approval letter. Without one, you may look less prepared than another buyer who has already completed that step.

How Long to Get Pre-Approved for Mortgage?

Another practical question is how long to get pre-approved for mortgage. The timeline depends on the lender, your financial situation, and how quickly you provide documents. Some buyers with straightforward income and clean documentation may move quickly. Others may take longer if they are self-employed, have multiple income sources, recently changed jobs, or need to explain credit issues.

If you are asking how long to get pre-approved for home loan, the best way to speed up the process is to prepare before you apply. Gather pay stubs, tax forms, bank statements, debt information, and identification. Respond quickly if the lender asks for more details. The faster you provide complete and accurate information, the easier it is for the lender to review your application.

Should I Get Pre-Approved for a Mortgage Before Looking?

Many buyers ask should I get pre-approved for a mortgage before looking. In most cases, yes. Getting pre-approved before touring homes helps you understand your realistic price range and prevents you from falling in love with a home that may not fit your budget.

If you are asking, should I get pre-approved for a mortgage, think of it as preparation rather than pressure. A pre-approval does not force you to buy a home. It simply gives you better information. It can also help your real estate agent recommend homes that make sense for your financial situation.

The same is true if you are wondering whether I should get pre-approved for a home loan. Pre-approval can make you a stronger, more confident buyer. It helps you compare payments, understand closing costs, and know what to expect before you make one of the biggest financial decisions of your life.

Final Thoughts on Getting Pre-Approved Online in Utah

Learning how mortgage pre-approval works is one of the best first steps for Utah homebuyers. Whether you are buying your first home, moving to a new city, or trying to compare Utah mortgage rates, pre-approval helps turn a vague home search into a clear plan.

The best approach is simple: gather your documents, choose a lender you trust, apply online or with local guidance, review your numbers carefully, and ask questions before making an offer. With the right preparation, getting pre-approved online can be convenient, informative, and empowering for first-time buyers in Utah.

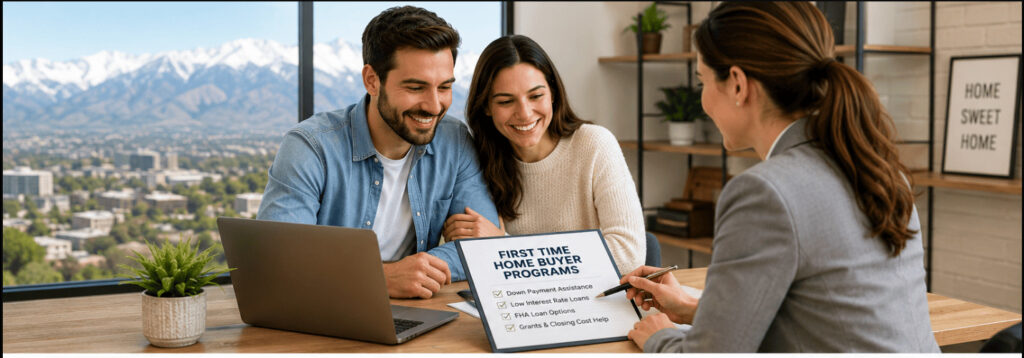

Buying your first home is an exciting milestone, but it can also feel overwhelming when you’re faced with choosing the right mortgage, understanding loan requirements, and saving for upfront costs. Fortunately, Utah offers several resources designed to help new buyers achieve homeownership. Whether you’re researching first time home buyers loans, comparing a first time home buyer mortgage, or exploring Utah first time home buyer programs, understanding your options can save you time, money, and unnecessary stress.

Many buyers assume they need a 20% down payment before purchasing a home, but that’s not always true. Depending on your financial situation, you may qualify for grants, assistance programs, or government-backed loans that make buying your first home much more affordable.

First Time Home Buyer Programs and Best First Time Home Buyer Loans

There are many first time home buyer programs available to help qualified buyers purchase a home with lower upfront costs. Some are offered through private lenders, while others are backed by federal or state agencies.

If you’re looking for first time home buyers loans, it’s important to compare several financing options before making a decision. Conventional loans work well for buyers with strong credit and larger down payments, while FHA, VA, and USDA loans provide more flexible qualification requirements.

Many buyers searching for a first time home owner’s loan are surprised to discover that Utah also offers local assistance programs. Several Utah first time home buyer programs provide financial assistance for qualified applicants through grants or affordable financing options.

Researching the best first time home buyer loans and the best first time home buyer programs can help you reduce your monthly payment and lower your overall borrowing costs.

First Time Home Buyer Assistance Utah, Grants, and Down Payment Assistance

One of the biggest challenges for new homeowners is saving enough money for a down payment and closing costs. Fortunately, several organizations offer first time home buyer grants Utah and first time home buyer assistance programs to help eligible buyers purchase a home sooner.

Some programs include first time home buyer down payment assistance, which can reduce or even eliminate the amount of cash required at closing. Buyers who qualify for these programs often find that homeownership becomes much more attainable than they originally expected.

Depending on your income, military status, or loan type, you may even qualify for no down payment first time home buyer financing. While these opportunities aren’t available to everyone, working with an experienced mortgage professional can help determine which programs fit your financial situation.

It’s important to remember that assistance programs frequently change, so staying informed about current eligibility requirements is essential. Many lenders can also help buyers combine grants and assistance programs with affordable mortgage products for even greater savings.

First Time Home Buyer Requirements and How to Qualify for a First Home Buyer Loan

Every mortgage program has its own qualification guidelines, but there are several common first time home buyer requirements that most lenders evaluate.

Your income, employment history, debt-to-income ratio, available savings, and overall financial health all play a role in determining your eligibility. Lenders will also review the first time home buyer credit score requirements before approving your application.

If you’re wondering how to qualify for a first home buyer loan, start by improving your credit score, paying down existing debt, avoiding large purchases before applying, and building a stable employment history. Even small improvements in your financial profile can increase your chances of approval while helping you secure better loan terms.

Working with a knowledgeable mortgage lender early in the process can also help you understand which loan programs best match your financial goals and long-term plans.

First Time Home Buyer Pre Approval and How to Get Pre Approved for a Mortgage

One of the smartest things you can do before shopping for homes is obtain first time home buyer pre approval.

If you’re wondering how to get pre-approved for a mortgage, the process usually begins with completing a mortgage application and providing documentation such as recent pay stubs, tax returns, W-2 forms, bank statements, and proof of employment.

Many lenders also allow buyers to prequalify for home loan first time buyers online before completing the full pre-approval process. Although pre qualification provides only an estimate, pre-approval demonstrates to sellers that you’re a serious buyer who has already completed much of the financing process.

Getting pre-approved also helps you establish a realistic home-buying budget and gives you greater confidence when making an offer on a property.

First Time Buyer Mortgage Rates, FHA Loans, and Closing Costs

One of the most important factors when purchasing a home is understanding today’s first time buyer interest rate and comparing first time buyer mortgage rates from several lenders. Even a small difference in interest rates can significantly affect your monthly mortgage payment and the total amount you pay over the life of your loan.

Many first-time buyers choose an FHA loan first time home buyer program because FHA loans typically require lower down payments and have more flexible credit score requirements than conventional loans. A first time home buyer loan can be an excellent choice for borrowers who have limited savings or are still building their credit history.

When comparing loan options, don’t focus only on the interest rate. Review the loan term, monthly payment, mortgage insurance, and closing costs to understand the full cost of borrowing. Speaking with a trusted mortgage professional can help you compare offers and determine which financing option best fits your needs.

First Time Home Buyer Closing Costs and Mortgage Calculator

Many buyers save for a down payment but forget to budget for first time home buyer closing costs. These costs typically include lender fees, title insurance, appraisal fees, escrow charges, recording fees, prepaid property taxes, and homeowners insurance.

Some Utah assistance programs may help cover part of these expenses, making homeownership even more affordable for qualified buyers.

Before purchasing a home, it’s also helpful to estimate your monthly payment using a first time home buyer’s mortgage calculator. Although you’ll sometimes see the search phrase first time home buyers mortgage online, using a mortgage calculator allows you to compare different purchase prices, interest rates, loan terms, and down payment amounts before speaking with a lender.

Planning ahead helps eliminate surprises and allows you to choose a home that comfortably fits your monthly budget.

Why First-Time Home Buyers in Utah Should Plan Ahead

Buying your first home is about much more than finding the perfect house. It’s also about understanding your financing options, preparing your finances, and taking advantage of programs designed to help new homeowners succeed.

By researching first time home buyers loans, exploring Utah first time home buyer programs, understanding first time home buyer requirements, and comparing available mortgage products, you’ll be in a much stronger position when it’s time to submit an offer.

Many buyers who spend time preparing before they begin house hunting experience a smoother mortgage process and often save money through grants, assistance programs, or better financing terms.

Final Thoughts

Purchasing your first home is a major milestone, and having the right information makes all the difference. Whether you’re looking for the best first time home buyer programs, comparing the best first time home buyer loans, researching mortgage rates, or learning how to qualify for assistance, taking the time to prepare now can save you money and reduce stress later.

Utah offers a variety of resources that can help first-time buyers achieve homeownership. By understanding available loan options, improving your financial profile, obtaining pre-approval, and exploring down payment assistance opportunities, you’ll be ready to move forward with confidence.

If you’re ready to begin your home-buying journey, the team at MortgageRateUtah.com can help you compare loan options, answer your questions, and guide you through every step of the mortgage process. Contact us today to learn which first-time home buyer program is the best fit for your goals.

Utah Mortgage Rates: The Ultimate 2026 Home Financing Guide

Navigating the local real estate market requires a clear, data-driven understanding of how home financing impacts your long-term wealth. Whether you are a first-time homebuyer looking at a townhome along the Wasatch Front or a current homeowner exploring a refinancing opportunity, tracking current Utah Mortgage rates is the definitive first step toward making an informed financial decision. Because buying real estate is likely the largest investment you will ever make, you should never guess your financial data or rely on national averages. Utilizing a professional mortgage estimator tool allows you to move past generalized estimates and analyze concrete numbers tailored specifically to our local economic climate.

Current mortgage rates in Utah

Current mortgage rates in Utah fluctuate daily based on broader macroeconomic indicators, employment reports, and Federal Reserve monetary policies. If you are actively shopping for a home anywhere in the state, keeping a close eye on Utah mortgage rates can save you tens of thousands of dollars over the life of your home loan. When analyzing your local financing options, you will generally choose between two primary debt structures: a stable fixed-rate option or a flexible adjustable-rate mortgage.

A traditional fixed rate mortgage offers total long-term predictability, ensuring that your core monthly principal and interest payment never changes regardless of how the broader market shifts. Conversely, ARM mortgage rates typically start noticeably lower than fixed options during their initial introductory period. However, these adjustable-rate structures are subject to periodic market changes over time, meaning your future payments could adjust upward later if inflation prints hot.

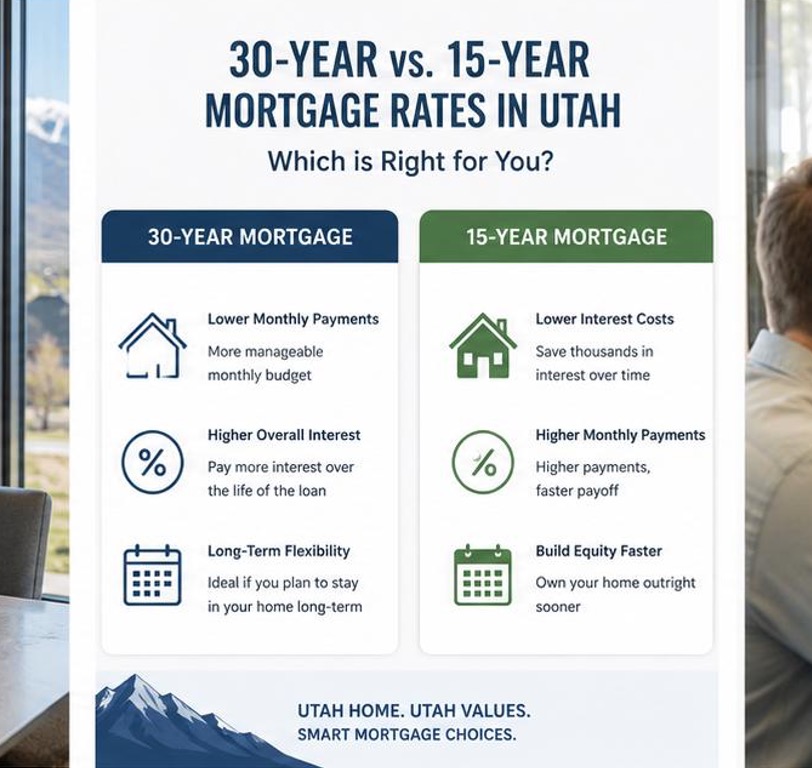

The mortgage rates average varies significantly depending on whether you commit to a shorter, aggressive repayment schedule or a longer, more affordable timeline. Choosing the right term determines how much house you can afford today and how much total interest you will transfer to your bank over the coming decades.

30 year fixed mortgage rates: This remains the most popular financing path for Utah buyers because it balances affordability with total safety.

30 year mortgage rates: Spreading your principal payments over three full decades lowers your immediate monthly obligation, giving you essential breathing room in your household budget.

15 year mortgage rates: If your household income can comfortably handle a larger monthly payment, a 15-year term secures a much lower interest rate and allows you to build home equity twice as fast.

Before you start touring open houses or contacting real estate agents, you must run the actual math using an interactive mortgage calculator. Relying on a comprehensive mortgage estimator helps you translate a gross real estate purchase price into an accurate, realistic monthly payment. To get a complete, transparent picture of your future housing liabilities, a premium calculator should measure more than just basic principal and interest; it must factor in local property taxes, homeowners insurance premiums, and potential private mortgage insurance (PMI).

A standard, generic simple mortgage calculator is excellent for fast, high-level math while you are casually browsing regional MLS listings online. However, utilizing a specialized Utah home loan calculator gives you a distinct competitive advantage in this market. This localized tool applies specific regional tax averages and geographic insurance cost structures, serving as a highly precise interest rates estimator and baseline payment breakdown. By feeding your unique target metrics into a comprehensive home loan calculator, you can safely test various down payment percentages to find your exact financial comfort zone.

framework. Depending on your professional background, military service, or current income brackets, specialized government-backed loan programs might offer significantly more favorable financing terms. You can review national eligibility baselines on the HUD Exchange to see how federal guidelines align with local state programs.

For those who have served our country, a VA loan offers an unparalleled path to homeownership, frequently requiring zero down payment and bypassing costly private mortgage insurance. Utilizing a dedicated, specialized VA loan calculator ensures you accurately account for the unique VA funding fees associated with these specific military housing benefits.

If your credit history is still growing or you have a smaller down payment saved up, Federal Housing Administration (FHA) programs provide an outstanding alternative. Because these programs feature distinct mortgage insurance premium structures, checking the latest Utah FHA loan rates and running your target purchase prices through a customized FHA loan calculator will help prevent any unexpected budget surprises at the closing table.

Buying your property is only the opening chapter of your personal wealth-building journey. To truly comprehend how your equity grows through real estate, you must regularly review your personalized mortgage amortization schedule. This technical schedule breaks down exactly how much of every single dollar paid goes toward reducing your principal balance versus how much goes directly to your lender as interest profit.

In the initial years of homeownership, your monthly mortgage calculator results will show that the vast majority of your payment goes toward serving the interest layer. Over time, that mathematical relationship flips, and your payments begin heavily chunking down the principal.

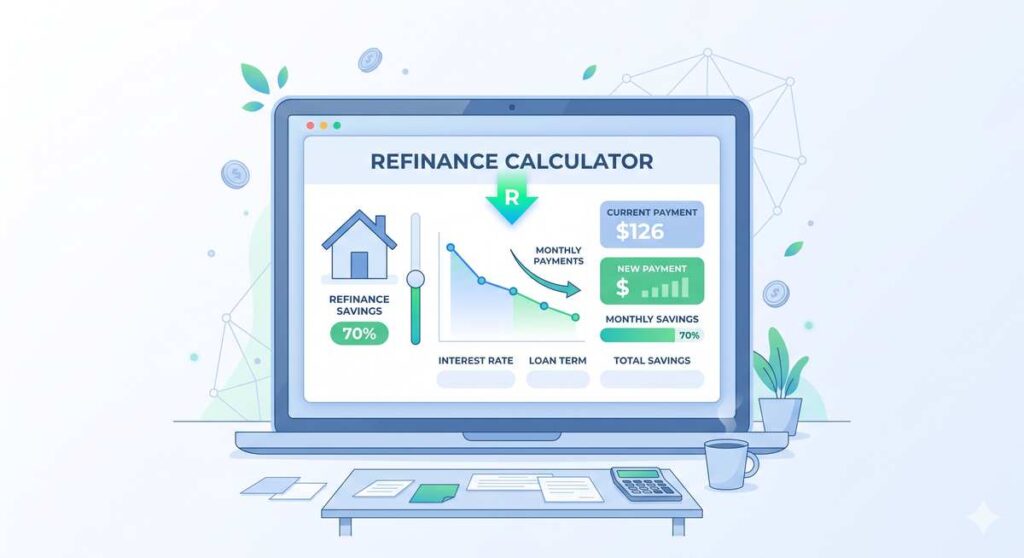

If market conditions improve or your credit score increases significantly after a few years of consistent payments, you should immediately check our Internal Refinance Portal to view current step-down programs. Running your metrics through a refinance calculator allows you to compare your existing interest note against today’s current environment to see if altering your term makes financial sense. By plugging your remaining loan balance into a specialized refinance calculator, you can visually map your financial break-even point and determine if updating your loan will result in immediate monthly savings.

Knowing your numbers provides incredible leverage, but executing the correct steps in the right order is what actually secures the keys to your new home.

Establish Your Baseline Budget: Use a standard monthly mortgage calculator to discover a safe, conservative housing budget based on your verifiable income.

Study Your Equity Growth: Review a simulated mortgage amortization schedule to understand how your principal paydown behaves over time.

Get Certified by a Lender: Before making a formal legal offer on any property, obtain a formal mortgage pre-approval from a licensed local lender to prove to sellers that your financial backing is fully verified.

Labeled diagram showing a Utah mortgage amortization schedule principal vs interest breakdown over 30 years.

If you have been watching interest rates and asking yourself should i refinance my home, you are not the only one. Refinancing can lower your payment, shorten your loan, or free up some cash, but it only makes sense when the numbers add up. This article walks through what it costs, when the timing is right, and how to know if you will qualify so you can feel confident about the decision.

Before you get into it, it helps to understand how does refinancing a mortgage work. Basically you replace your current loan with a new one, hopefully at a better rate or term. A lot of homeowners do this to refinance to lower monthly payment amounts, and others do it to refinance to lower rate costs over the life of the loan. Using a refinance mortgage calculator is the quickest way to see what a new loan would actually look like for you.

What Are the Refinance Closing Costs?

Since refinancing is not free, the first thing to look at is the refinance closing costs. These usually come out to two to five percent of your loan amount, and they cover things like the appraisal, the title, and the lender fees. It is good to know the typical refinance closing costs before you apply, and a refinance closing cost estimator can give you a quick idea of the range. A lot of people are surprised by the full cost to refinance house loans, so it is smart to plan for it.

If paying the fees up front is hard, you can ask your lender about a no closing cost refinance, where the costs get rolled into the loan or the rate instead. To compare your options the right way, look at the average cost to refinance next to how much you would save each month. Comparing the average cost to refinance mortgage against your break even point tells you if the deal is actually worth it.

When Is the Best Time to Refinance a Mortgage?

Timing can matter just as much as cost. The best time to refinance mortgage loans is usually when rates have dropped below your current rate, your credit has improved, or you have built up some equity. Most people agree it is a good time to refinance when you can cut your rate by about half a percent or more. In other words, it is a good time to refinance mortgage debt when the savings clearly beat the fees.

A refinance savings calculator helps you test out the timing, and a free mortgage refinance calculator lets you compare a few different situations without paying anything. The whole goal is to refinance lower interest rate terms that save you more than the refinance ends up costing you.

Should You Refinance to a 15 Year Mortgage?

Shortening your loan term is another common reason people refinance. If you refinance to 15 year mortgage loans, you usually pay a lot less interest overall, but your monthly payment goes up. Right now the 15 year refinance rates are often lower than the 30 year rates, which makes the switch more appealing for people who can handle a bigger payment in exchange for saving more in the long run.

How to Qualify for a Mortgage Refinance

Before you apply, it is worth finding out how to qualify for mortgage refinance approval. Lenders look at your credit score, your income, your debt, and your home equity. A common first question is how much refinance can i qualify for, and getting a rough answer early saves you time. If you are not sure whether will i qualify for a mortgage refinance approval applies to you, a quick pre qualification check with a lender gives you a clear yes or no without locking you into anything.

Is It Worth Refinancing My Home?

After you weigh the cost, the timing, and qualifying, the real question is is it worth refinancing my home right now. It usually is when your monthly savings make back the closing costs in a reasonable amount of time and you plan to stay in the home past that point. It also helps to know how long does it take to refinance a house, which is normally about 30 to 45 days, so you can plan around it. If the savings are clear and you are going to stay long enough to enjoy them, then refinancing is probably worth it.

The bottom line is that you can answer should i refinance my home by running your own numbers, comparing the costs to the savings, and making sure the timing fits your goals.

A homebuyer can enter the correct figures into a calculator and still walk away with a misleading answer. The problem is often not the formula; it is the assumptions behind the numbers. A reliable dti ratio for mortgage estimate should reflect documented income, required monthly debts, and a realistic future housing payment. When one of those inputs is incomplete, the percentage may look better or worse than the figure a lender eventually uses. The following seven mistakes explain why online estimates can disagree and how to build a more useful home-loan stress test.

Mistake 1: Using Take-Home Pay Instead of Gross Monthly Income

The basic debt to income ratio compares required monthly debt payments with gross monthly income, meaning income before taxes and payroll deductions. Using take-home pay produces a different percentage and makes it difficult to compare your estimate with a lender calculation. Someone who says, “I want to calculate my debt to income ratio,” should begin with monthly gross income shown on pay records or other acceptable documentation, not the amount deposited into a checking account.

Variable income requires extra care. Overtime, commissions, bonuses, seasonal income, and self-employment earnings may not be counted exactly as they appear in a strong month. A personal worksheet can include those earnings for budgeting, but a lender may average or document them differently. This is one reason a self-calculated debt to income ratio for home loan estimate should be treated as preparation rather than an approval decision.

Mistake 2: Entering Loan Balances Instead of Required Monthly Payments.

DTI generally uses recurring monthly obligations, not the full amount owed. A $20,000 auto balance does not go into the formula as $20,000; the required monthly payment does. The same principle usually applies to credit cards, student loans, personal loans, leases, and other installment debt. Confusing balances with payments can make a mortgage debt to income ratio look impossibly high.

The reverse mistake is leaving out a payment because the balance feels small or because the debt will be paid off “soon.” Until the obligation is actually resolved and documented, it may still matter. Build a list from current statements and credit reports rather than memory. That produces a cleaner debt ratio for mortgage analysis and makes it easier to explain any difference between your estimate and the lender’s figure.

Mistake 3: Estimating Only Principal and Interest for the New Home

A proposed housing payment is usually more than principal and interest. Property taxes, homeowners insurance, mortgage insurance, and homeowners association dues can materially change the total. Buyers who use only the advertised loan payment may underestimate their debt to income ratio for mortgage and their debt to income ratio for buying a house.

Before you calculate debt to income ratio for mortgage planning, estimate the full monthly housing obligation. Test more than one property-tax level and insurance estimate because two similarly priced homes can produce different monthly costs. The goal is not to predict the exact final payment down to the dollar. It is to avoid building a home search around an unrealistically low housing number.

Mistake 4: Treating Every Online Calculator as the Same Tool

Search results use many labels for similar tools: dti calculator, debt to income calculator, mortgage debt to income ratio calculator, dti mortgage calculator, debt to income ratio mortgage calculator, and debt to income mortgage calculator. The names overlap, but the input fields do not always work the same way. One tool may ask for a total housing payment, another may build the payment from separate fields, and another may exclude obligations you assumed were included.

A debt to income ratio to buy a house calculator is most useful when the user can see every input and change one assumption at a time. A dti ratio calculator should help compare scenarios, not merely display one percentage. Run the same verified figures through two tools. If the results differ, inspect the housing, income, and debt fields before assuming one calculator is wrong.

The front end debt to income ratio compares the proposed housing expense with gross monthly income. Total or back-end DTI adds other required monthly debts. A buyer can have a reasonable housing-only percentage and still have a high total ratio because of auto loans, student loans, credit cards, or support obligations. Another buyer may have little non-housing debt but choose a house payment that consumes too much of the monthly budget.

When an article refers to debt to income for mortgage, confirm which ratio it means. A general statement about a good dti ratio is incomplete without context because loan programs, underwriting methods, and the rest of the application can matter. Use both housing-only and total figures to understand where the pressure comes from instead of chasing a single universal target.

Mistake 6: Assuming FHA Automatically Solves a High DTI

Consumers often search for an fha debt to income ratio because they have heard that FHA-insured loans can offer flexibility. That does not mean every higher ratio is automatically acceptable. A debt to income ratio for fha loan estimate still depends on how income and debts are documented, the complete application, and the lender’s process.

The same caution applies to a debt to income ratio calculator fha result. The tool can perform arithmetic, but it cannot decide whether a particular income source is usable or how a specific obligation will be treated. Use the percentage to organize questions for a mortgage professional rather than interpreting it as a guarantee.

Mistake 7: Optimizing for Approval Instead of Monthly Resilience

A lender calculation measures required debt obligations, but it does not include every expense that affects real life. Childcare, groceries, utilities, health care, transportation, home maintenance, travel, and savings goals may not appear in DTI. A buyer can satisfy a debt to income ratio for mortgage approval and still feel financially trapped after closing.

Use the dti ratio as one boundary, then build a second household budget using take-home pay and all recurring expenses. This second budget is not the lender’s formula; it is the affordability test that protects the rest of your life. The best home price is not necessarily the highest amount supported by an automated approval.

A Ten-Minute DTI Stress Test Before Preapproval

Start with a baseline using documented gross income, current required payments, and a complete estimated housing payment. Next, run three small shocks: increase the housing estimate by 10%, reduce usable income by 10%, and add one realistic monthly cost such as an association fee or higher insurance quote. The exercise shows whether the plan has breathing room or depends on every assumption going perfectly.

Then test one improvement. Remove a debt payment that could realistically be eliminated, lower the target purchase price, or increase the down payment without draining emergency savings. Recalculate the percentage after each change. This approach turns a calculator into a decision model and provides a more practical view of the debt to income ratio for mortgage than a single best-case result.

Finally, save the worksheet and bring it to the preapproval conversation. Ask which income was counted, which debts were included, and whether the lender’s housing estimate differs from yours. That comparison makes the debt to income ratio for home loan process easier to understand and helps identify the exact assumption that changed the number.

Use DTI to Find Errors Before They Become Loan Problems

DTI is simple arithmetic built on inputs that are not always simple. Using gross income, verified monthly payments, a complete housing estimate, and clearly labeled calculator fields will prevent most errors. Comparing front-end and total ratios, treating FHA results as estimates, and stress-testing the payment creates a more useful picture than searching for one perfect cutoff.

A careful estimate will not replace underwriting, but it can improve the questions you ask and the homes you consider. The strongest plan is one that remains workable when taxes, insurance, debt payments, or income are slightly different from the first estimate. That is how DTI becomes a homebuying tool rather than a last-minute surprise.

Buying a home in Utah is exciting, but before you start touring houses or making offers, one of the smartest first steps is mortgage pre approval. Getting pre-approved helps you understand your budget, compare loan options, and show sellers that you are a serious buyer.

If you are preparing to apply for a mortgage, this guide explains how the process works, what documents you may need, how credit affects your options, and how Utah-specific programs may help first-time buyers.

How to Get Pre Approved for a Home Loan

Many buyers begin by searching how to get pre approved for a home loan because they are not sure where to start. The process usually begins with choosing a lender and completing an initial application. The lender reviews income, employment history, credit score, debt, savings, and your overall financial picture.

When you get preapproved for a mortgage, the lender gives you an estimate of how much you may be able to borrow. This helps you shop in a realistic price range and avoid falling in love with a home that is outside your budget.

For buyers wondering how to get pre approved for a home loan first time buyer, the answer is to start early, organize your financial information, and speak with a lender before making assumptions about what you can afford.

Mortgage Pre Approval Process

The mortgage pre approval process is more detailed than a basic estimate. A lender usually reviews your financial documents and may check your credit. This allows the lender to provide a more accurate estimate of the loan amount you may qualify for. A typical pre-approval process includes completing an application, submitting income documents, reviewing your credit, estimating your monthly payment, and receiving a mortgage pre approval letter. Your mortgage pre approval letter is important because it shows sellers and real estate agents that you have already spoken with a lender. In a competitive Utah housing market, this can help strengthen your offer.

Mortgage Pre Approval vs Pre Qualification

Many buyers ask about mortgage pre approval vs pre qualification. A pre-qualification is usually a basic estimate based on information you provide. A pre-approval is more detailed because the lender may review documents and credit information. Some buyers also ask about mortgage pre approval without hard inquiry. This depends on the lender. Some may offer a soft credit review first, while a full pre-approval may require a hard credit inquiry.

What Documents Do I Need for Mortgage Pre Approval

One of the most common questions is what documents do I need for mortgage pre approval. Common documents include recent pay stubs, W-2 forms, tax returns, bank statements, identification, debt information, and proof of additional income if applicable.

If you are self-employed, you may need business tax returns, profit and loss statements, or 1099 forms. Having these documents ready can help the process move faster.

What Credit Score Do I Need for a Mortgage

Another common question is what credit score do I need for a mortgage. The answer depends on the loan type, lender requirements, down payment, income, and debt level.

If your credit is not perfect, you may still have options. Buyers often search how to get pre approved for a home loan with bad credit or can I buy a house with bad credit in Utah. The answer depends on your full financial situation.

Some buyers may also explore first time home buyer programs for bad credit. These programs vary, so it is important to speak with a lender who understands first-time buyer options.

First Time Home Buyer Programs and Utah Down Payment Assistance

Utah buyers often search for first time home buyer programs because they want help with down payments, closing costs, or loan qualification. These programs may vary based on location, income, credit, and property type.

For many buyers, Utah down payment assistance can be especially helpful. A down payment is one of the largest upfront costs in the process, and assistance programs may help qualified buyers reduce the amount of cash needed at closing.

Buyers may also compare first time home buyer loans, including FHA loans, conventional loans with low down payment options, VA loans for eligible borrowers, USDA loans in qualifying areas, or Utah-specific programs.

Understanding how to get approved for a home loan means understanding what lenders look for. They usually review credit score, income, employment history, monthly debts, down payment funds, savings, and loan program requirements.

If you are asking how to get a mortgage, the best place to start is by reviewing your finances before shopping. Check your credit, avoid new debt, save for upfront costs, and ask a lender what you can do to improve your approval chances.

How Much House Can I Afford in Utah

Before making an offer, ask how much house can I afford in Utah. Affordability is not just about the home price. Your monthly payment may include principal, interest, taxes, homeowners insurance, mortgage insurance, and HOA fees.

A lender can help estimate your monthly payment and compare different loan scenarios. It is important to choose a payment that fits your real life, not just the maximum amount you can technically borrow.

Steps to Buying a House in Utah

The steps to buying a house in Utah usually include reviewing your credit, saving for upfront costs, researching loans, completing home loan pre approval, choosing a real estate agent, searching for homes, making an offer, completing inspections, finalizing loan approval, and closing.

Many first-time buyers also need to plan for closing costs Utah first time buyer expenses. These may include lender fees, title fees, appraisal costs, recording fees, prepaid taxes, homeowners insurance, and other charges.

Best Mortgage Lenders for First Time Home Buyers

Searching for the best mortgage lenders for first time home buyers does not always mean choosing the lender with the lowest advertised rate. First-time buyers often need guidance, clear communication, and a lender who explains the process clearly.

A strong lender can help you compare options, understand your monthly payment, review assistance programs, and avoid common mistakes.

Mortgage Pre Approval How Long Does It Take

A common question is mortgage pre approval how long does it take. The timeline depends on how quickly you complete the application and provide documents. If your information is organized, pre-approval may happen quickly. If the lender needs more details, it may take longer.

To speed up the process, gather documents early, respond quickly to lender requests, and avoid major financial changes while your application is being reviewed.

Final Thoughts

Getting mortgage pre approval is one of the most important first steps in the Utah home-buying process. It helps you understand your budget, compare loan options, and shop for homes with confidence.

Whether you are ready to apply for a mortgage, explore first time home buyer programs, review Utah down payment assistance, or estimate how much house can I afford in Utah, starting with pre-approval gives you a clearer path forward.

Learn how mortgage pre approval works for first-time buyers, what documents you need, how loan programs help, and how to get ready before shopping for a home.

Mortgage Pre Approval for First Time Home Buyers

First-time home buyer reviewing mortgage pre approval documents before shopping for a home.

Mortgage Pre Approval First Time Home Buyer Guide

Buying your first home is exciting, but the mortgage process can feel overwhelming. Terms like mortgage pre approval, home loan pre approval, credit checks, down payments, and closing costs can be confusing at first. Before touring homes or making offers, getting preapproved is one of the smartest steps you can take. It helps you understand your budget, shows sellers you are serious, and gives you a clearer idea of which loan options fit your situation.

A mortgage pre approval first time home buyer process happens when a lender reviews your income, credit, debts, assets, and employment history to estimate how much you may be able to borrow. After reviewing your information, the lender may give you a preapproval letter showing the loan amount you could qualify for.

This matters because sellers want to know that a buyer can get financing. A first time home buyer pre approval letter can make your offer stronger and help you avoid shopping outside your real budget. Instead of falling in love with a home first and figuring out the money later, preapproval gives you clear expectations from the start.

Documents Needed for Mortgage Pre Approval

The documents needed for mortgage pre approval usually include proof of income, bank statements, tax forms, identification, employment details, and a list of debts such as credit cards, auto loans, or student loans. If you are self-employed, you may need extra tax returns or business records. Having these ready can make the process faster and easier.

A first time home buyer pre approval checklist can help you stay organized. Include recent pay stubs, W-2s or tax returns, bank statements, photo ID, rental history, monthly debts, estimated down payment, closing cost savings, and questions for your lender.

Checklist of documents needed for mortgage pre approval including pay stubs, tax forms, and bank statements.

It is also important to understand mortgage pre approval vs pre qualification. Prequalification is usually a basic estimate based on information you provide, while preapproval is stronger because the lender reviews more documents and may check your credit.

Prequalification can be helpful early on, but preapproval is better when you are ready to shop seriously. A preapproval letter gives your real estate agent and sellers more confidence that you are financially prepared.

There are several first time home buyer loans that can make buying a home more affordable. Common options include conventional loans, FHA loans, VA loans, USDA loans, and state assistance programs. The right first time buyer mortgage depends on your credit, income, debt, location, military status, and down payment.

An FHA loan first time home buyer option may help buyers who need a lower down payment or more flexible credit requirements. Some buyers also look for first time home buyer loans with zero down or no down payment first time home buyer options, which may be available through VA or USDA loans. Since not every buyer or property qualifies, it is important to compare your options with a lender.

The best first time home buyer loans are not always the ones with the lowest advertised rate. A good loan should fit your budget, savings, credit, and long-term plans. When comparing the best mortgages for first time buyers, look at the interest rate, APR, mortgage insurance, down payment, closing costs, and any special assistance programs.

Your first time home buyer interest rate depends on your credit score, loan type, down payment, debt-to-income ratio, and market conditions. This is why it helps to compare multiple first time home buyer lenders before choosing one. Even a small difference in rate or fees can affect your monthly payment.

If you are wondering how to qualify for a home loan first time buyer, start by reviewing your credit, income, debt, and savings. Paying bills on time, lowering credit card balances, avoiding new debt, and saving for upfront costs can help strengthen your application.

Qualifying Without Stretching Your Budget

A first time home loan is not just about getting approved for the highest amount. It is about choosing a payment that still leaves room for utilities, repairs, insurance, taxes, and daily expenses. A first time home buyer mortgage should support your goals without stretching your budget too far.

If you are looking for a first home buyers loan, start by speaking with a lender, reviewing your budget, and asking about programs that may lower your down payment or closing costs.

Many buyers ask, how long does mortgage pre approval take? The answer depends on the lender and how prepared you are. If your documents are ready and your finances are simple, it may be completed quickly. If income, credit, employment, or bank records need extra review, it may take longer.

To speed up the process, gather your documents before applying, respond quickly to lender questions, and avoid making major financial changes while you are shopping for a home. Do not open new credit cards, buy a car, or make large unexplained bank transfers without speaking to your lender first.

First time home buyer programs can help with down payments, closing costs, education, or special loan terms. They may come from federal, state, local, nonprofit, or lender-based sources. Some programs have income limits, location rules, education requirements, or rules about how long you must live in the home.

Before choosing a program, ask if the help is a grant, forgivable loan, deferred loan, or repayable second mortgage. This helps you understand the true cost and responsibility before moving forward.

First-time home buyer comparing FHA loans, low down payment programs, and zero down payment mortgage options.

Before applying for home loan pre approval, use this quick checklist:

Review your credit report and fix errors.

Save recent pay stubs, W-2s, tax returns, and bank statements.

Calculate your monthly debts.

Estimate your down payment and closing cost savings.

Compare several first time home buyer lenders.

Ask about FHA, VA, USDA, conventional, and assistance programs.

Buying a home is one of the most significant financial decisions you will ever make, so it’s natural to ask, “how much mortgage can I afford?” Before you begin touring homes or submitting offers, it’s important to understand the financial factors that determine your purchasing power. While many buyers immediately turn to a mortgage affordability calculator, the calculator is only one part of the process. Your income, existing debt, credit profile, interest rate, and down payment all influence the amount you can comfortably borrow.

Whether you’re researching home affordability, comparing the price of house i can afford, or preparing to meet with a lender, understanding how affordability is calculated will help you make confident, informed decisions. The more prepared you are before applying for a mortgage, the easier it becomes to establish a realistic budget and find a home that fits both your needs and your finances.

Mortgage Affordability and Mortgage Affordability by Income

When lenders evaluate your application, one of the first factors they consider is mortgage affordability by income. Your annual salary provides the foundation for determining how much you may qualify to borrow, but it is only one piece of the equation. Many buyers begin their research with a home affordability calculator, a house affordability calculator, or a home loan affordability calculator to estimate an affordable price range before speaking with a mortgage professional.

You may also search phrases such as home affordability by salary, house affordability based on income, how much house can I afford based on income, or what mortgage can I afford with my salary. Although each search is worded differently, they all seek the same answer: how your income translates into purchasing power. Even buyers asking how much house can I buy with my income or trying to determine the maximum mortgage based on income should remember that lenders evaluate the complete financial picture rather than salary alone.

Debt to Income Ratio for Home Loan Qualification

Income is important, but lenders also place significant emphasis on your debt to income ratio for home loan approval. This ratio compares your monthly debt obligations to your gross monthly income and helps determine whether you can comfortably manage a mortgage payment alongside your other financial responsibilities.

Improving your debt-to-income ratio before purchasing a home may increase both your borrowing capacity and your financing options. This is why many buyers research how much home loan can I qualify for before beginning the application process. Others may wonder about the income needed to buy a house or calculate the income to afford 500k house. In every case, reducing debt and strengthening your overall financial profile can improve your mortgage eligibility.

Mortgage Calculator What Can I Afford and House Affordability

Online calculators have become valuable planning tools because they allow buyers to estimate payments in just a few minutes. A mortgage calculator what can i afford uses information such as income, monthly debt, estimated interest rate, property taxes, insurance, and down payment to generate an estimated price range.

Many buyers also search for house affordability, mortgage affordability, or a mortgage affordability calculator before contacting a lender. These resources provide an excellent starting point, but they should be viewed as estimates rather than guaranteed loan approvals. If you’ve ever searched home much home can i afford, you’re asking the same fundamental question: what home price fits comfortably within your long-term financial goals?

Understanding Home Affordability Before You Buy

Knowing your budget is about more than qualifying for the largest possible loan. True home affordability means purchasing a home that allows you to comfortably manage monthly payments while continuing to save for emergencies, retirement, vacations, and other life goals.

Instead of stretching your finances to the maximum approval amount, consider what payment best supports your lifestyle. Buyers researching house affordability, comparing a home affordability calculator, or estimating the price of house i can afford often discover that purchasing below their maximum qualification creates greater financial flexibility and long-term stability.

VA Loan Affordability Calculator Options

Eligible veterans and active-duty military members have access to specialized financing programs that may improve affordability. Many begin their research with a va loan affordability calculator or a va mortgage affordability calculator to estimate purchasing power under VA loan guidelines.

Although VA loans offer unique benefits such as competitive interest rates and, in many cases, no down payment requirement, affordability is still based on income, debt obligations, and monthly expenses. Understanding these factors before beginning your home search can help you choose a mortgage that supports your financial future.

Take the Next Step Toward Homeownership

Purchasing a home should never be based solely on what a lender is willing to approve. Instead, use tools such as a mortgage affordability calculator, review your mortgage affordability by income, and evaluate your debt to income ratio for home loan before making one of the largest financial commitments of your life.

Whether you’re researching how much mortgage can I afford, exploring a house affordability calculator, comparing home affordability, or determining the price of house i can afford, the best next step is speaking with an experienced mortgage professional. Combining online affordability tools with expert guidance will give you a clearer understanding of your budget and help you purchase a home with confidence.

Buying a home is one of the biggest financial decisions most people will ever make. That’s why keeping up with Utah mortgage rates today is so important. Whether you’re purchasing your first home, moving to a new neighborhood, or refinancing your current loan, even a small change in interest rates can have a noticeable impact on your monthly payment and long-term costs.

Understanding Utah mortgage rates today can help you make smarter decisions and potentially save thousands of dollars over the life of your loan.

Utah mortgage rates today consultation with homebuyers

Understanding Utah Mortgage Rates Today

Most homebuyers start their search by checking current mortgage rates and mortgage rates today. It’s a good place to begin because your interest rate plays a major role in determining what you can afford.

Several factors influence mortgage rates in utah, including inflation, economic conditions, your credit score, and the type of loan you’re applying for. Lenders also look at your debt-to-income ratio, down payment amount, and overall financial profile when determining your rate.

If you’re researching current mortgage rates utah, it’s worth getting quotes from multiple lenders. Many buyers are surprised to learn that rates and fees can vary significantly from one lender to another. Taking the time to compare offers can help you find some of the best mortgage rates available.

Comparing 30-Year and 15-Year Mortgage Rates

When comparing loan options, most buyers focus on 30 year mortgage rates and 15 year mortgage rates.

A 30-year mortgage is popular because it spreads payments over a longer period, resulting in lower monthly payments. That’s why many borrowers regularly monitor 30 year mortgage rates today, current 30 year mortgage rates, and current 30 year fixed mortgage rates when shopping for a home.

On the other hand, borrowers who want to build equity faster and pay less interest over time often choose a 15-year mortgage. While the monthly payments are higher, the long-term savings can be substantial.

Before choosing a loan, compare:

30 year fixed mortgage rates

30 year mortgage rates utah

15 year mortgage rates utah

current home loan interest rates

The right option depends on your budget, financial goals, and how long you plan to stay in the home.

Comparing Utah mortgage rates today for 30-year and 15-year home loans

FHA and VA Mortgage Rates Utah Buyers Should Consider

Not every borrower fits the traditional mortgage profile, which is why government-backed loan programs remain popular.

Many buyers with smaller down payments explore fha mortgage rates utah because FHA loans typically have more flexible qualification requirements. These loans can be especially helpful for first-time buyers who may not have perfect credit or a large amount saved for a down payment.

Eligible military members and veterans should also look into va mortgage rates utah. VA loans often offer competitive rates and may allow qualified borrowers to purchase a home with little or no down payment.

Taking the time to compare FHA, VA, and conventional loan options can help you find the financing solution that works best for your situation.

First-Time Home Buyer Mortgage Rates Utah Residents Can Access

Buying your first home can feel overwhelming, but there are resources available to make the process easier.

Many people searching for first time home buyer mortgage rates utah may qualify for programs that provide down payment assistance, help with closing costs, or additional educational resources. These programs are designed to help buyers overcome some of the common barriers to homeownership.

If you’re entering the market for the first time, it’s worth exploring all available options before choosing a loan. The right program could make a significant difference in both your upfront costs and your monthly payment.

First-time homebuyers discussing Utah home loan rates with a mortgage lender

Are Mortgage Rates Going Down in Utah?

One question many buyers are asking right now is: are mortgage rates going down in utah?

The truth is that nobody can predict future mortgage rates with complete certainty. Rates are influenced by inflation, economic growth, Federal Reserve policies, and broader market conditions. Because of this, they can change frequently.

Many borrowers keep an eye on:

home mortgage rates today

utah home loan rates

average mortgage rate in utah

salt lake city mortgage rates

best mortgage rates utah

Staying informed can help you recognize opportunities and make more confident decisions about when to lock in a rate.

Final Thoughts on Utah Mortgage Rates

Choosing a mortgage isn’t just about finding the lowest number advertised online. It’s about understanding your options, comparing lenders, and selecting a loan that fits your long-term financial goals.

Whether you’re researching mortgage rates today, comparing current mortgage rates utah, evaluating 30 year mortgage rates today, or looking for the best loan program available, taking the time to do your homework can pay off in the long run.

The more informed you are, the better prepared you’ll be to secure a mortgage that works for your budget and your future. You can also explore additional Utah Mortgage Rate Resources for more home-buying information.