By: Charlie Mcleod

Utah Mortgage Rates: The Ultimate 2026 Home Financing Guide

Navigating the local real estate market requires a clear, data-driven understanding of how home financing impacts your long-term wealth. Whether you are a first-time homebuyer looking at a townhome along the Wasatch Front or a current homeowner exploring a refinancing opportunity, tracking current Utah Mortgage rates is the definitive first step toward making an informed financial decision. Because buying real estate is likely the largest investment you will ever make, you should never guess your financial data or rely on national averages. Utilizing a professional mortgage estimator tool allows you to move past generalized estimates and analyze concrete numbers tailored specifically to our local economic climate.

Current mortgage rates in Utah

Current mortgage rates in Utah fluctuate daily based on broader macroeconomic indicators, employment reports, and Federal Reserve monetary policies. If you are actively shopping for a home anywhere in the state, keeping a close eye on Utah mortgage rates can save you tens of thousands of dollars over the life of your home loan. When analyzing your local financing options, you will generally choose between two primary debt structures: a stable fixed-rate option or a flexible adjustable-rate mortgage.

A traditional fixed rate mortgage offers total long-term predictability, ensuring that your core monthly principal and interest payment never changes regardless of how the broader market shifts. Conversely, ARM mortgage rates typically start noticeably lower than fixed options during their initial introductory period. However, these adjustable-rate structures are subject to periodic market changes over time, meaning your future payments could adjust upward later if inflation prints hot.

The mortgage rates average varies significantly depending on whether you commit to a shorter, aggressive repayment schedule or a longer, more affordable timeline. Choosing the right term determines how much house you can afford today and how much total interest you will transfer to your bank over the coming decades.

- 30 year fixed mortgage rates: This remains the most popular financing path for Utah buyers because it balances affordability with total safety.

- 30 year mortgage rates: Spreading your principal payments over three full decades lowers your immediate monthly obligation, giving you essential breathing room in your household budget.

- 15 year mortgage rates: If your household income can comfortably handle a larger monthly payment, a 15-year term secures a much lower interest rate and allows you to build home equity twice as fast.

Before you start touring open houses or contacting real estate agents, you must run the actual math using an interactive mortgage calculator. Relying on a comprehensive mortgage estimator helps you translate a gross real estate purchase price into an accurate, realistic monthly payment. To get a complete, transparent picture of your future housing liabilities, a premium calculator should measure more than just basic principal and interest; it must factor in local property taxes, homeowners insurance premiums, and potential private mortgage insurance (PMI).

A standard, generic simple mortgage calculator is excellent for fast, high-level math while you are casually browsing regional MLS listings online. However, utilizing a specialized Utah home loan calculator gives you a distinct competitive advantage in this market. This localized tool applies specific regional tax averages and geographic insurance cost structures, serving as a highly precise interest rates estimator and baseline payment breakdown. By feeding your unique target metrics into a comprehensive home loan calculator, you can safely test various down payment percentages to find your exact financial comfort zone.

framework. Depending on your professional background, military service, or current income brackets, specialized government-backed loan programs might offer significantly more favorable financing terms. You can review national eligibility baselines on the HUD Exchange to see how federal guidelines align with local state programs.

For those who have served our country, a VA loan offers an unparalleled path to homeownership, frequently requiring zero down payment and bypassing costly private mortgage insurance. Utilizing a dedicated, specialized VA loan calculator ensures you accurately account for the unique VA funding fees associated with these specific military housing benefits.

If your credit history is still growing or you have a smaller down payment saved up, Federal Housing Administration (FHA) programs provide an outstanding alternative. Because these programs feature distinct mortgage insurance premium structures, checking the latest Utah FHA loan rates and running your target purchase prices through a customized FHA loan calculator will help prevent any unexpected budget surprises at the closing table.

Buying your property is only the opening chapter of your personal wealth-building journey. To truly comprehend how your equity grows through real estate, you must regularly review your personalized mortgage amortization schedule. This technical schedule breaks down exactly how much of every single dollar paid goes toward reducing your principal balance versus how much goes directly to your lender as interest profit.

In the initial years of homeownership, your monthly mortgage calculator results will show that the vast majority of your payment goes toward serving the interest layer. Over time, that mathematical relationship flips, and your payments begin heavily chunking down the principal.

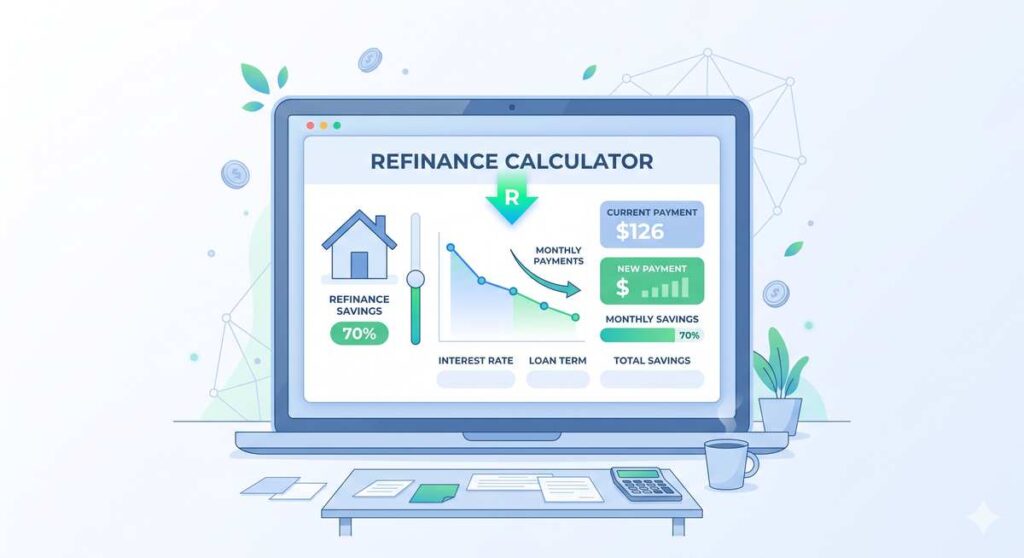

If market conditions improve or your credit score increases significantly after a few years of consistent payments, you should immediately check our Internal Refinance Portal to view current step-down programs. Running your metrics through a refinance calculator allows you to compare your existing interest note against today’s current environment to see if altering your term makes financial sense. By plugging your remaining loan balance into a specialized refinance calculator, you can visually map your financial break-even point and determine if updating your loan will result in immediate monthly savings.

Knowing your numbers provides incredible leverage, but executing the correct steps in the right order is what actually secures the keys to your new home.

- Establish Your Baseline Budget: Use a standard monthly mortgage calculator to discover a safe, conservative housing budget based on your verifiable income.

- Study Your Equity Growth: Review a simulated mortgage amortization schedule to understand how your principal paydown behaves over time.

- Get Certified by a Lender: Before making a formal legal offer on any property, obtain a formal mortgage pre-approval from a licensed local lender to prove to sellers that your financial backing is fully verified.