Mortgage refinancing is one of the most powerful tools a homeowner has for cutting monthly costs and building long-term wealth. When you refinance, you replace your existing home loan with a new one — ideally at a lower rate or a better term. With mortgage rates today shifting week to week, keeping an eye on current mortgage rates and mortgage rates today helps you spot the right moment to act. Homeowners typically refinance to reduce their payment, shorten their loan, or tap equity through a refinance home loan.

When Refinancing Makes Sense in Today’s Market

Before you commit, compare your existing rate against refinance mortgage rates and refinance rates available now. A common guideline is that refinancing pays off when you can lower your rate meaningfully and stay in the home long enough to recover closing costs. A refinance calculator makes this easy — plug in your balance and new rate to find your break-even point. If you are shopping broadly, comparing best mortgage rates and home loan interest rates across several offers ensures you don’t leave money on the table.

Cash Out and Home Equity Options

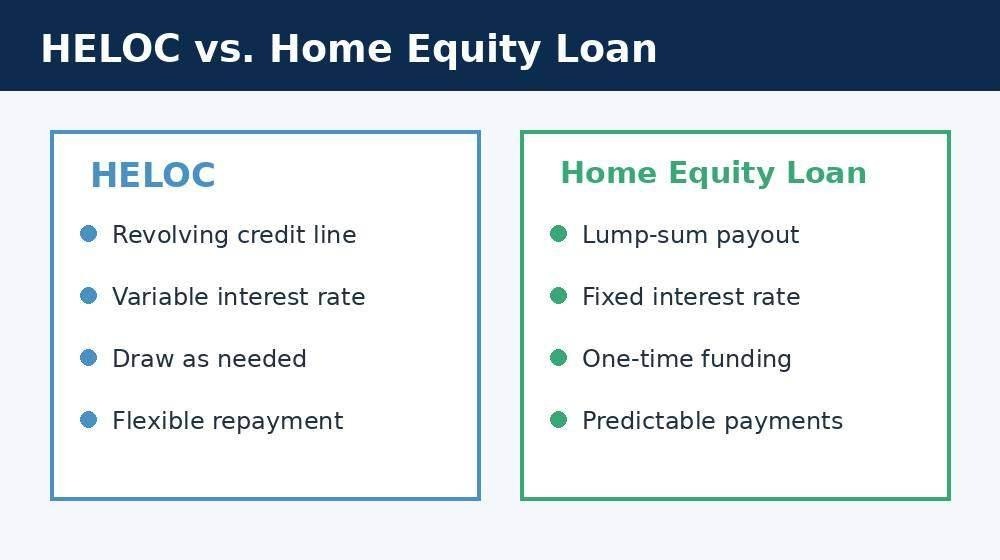

Not every homeowner refinances just for a lower rate. A cash out refinance lets you borrow more than you currently owe and take the difference as cash — useful for renovations or consolidating debt. Run the numbers with a cash out refinance calculator before deciding. If you’d rather keep your first mortgage untouched, a home equity loan or a home equity line of credit (heloc) borrows against your equity separately. Watch heloc rates and home equity loan rates closely, since these products price differently than a primary mortgage.

Calculating Your Payment Before You Apply

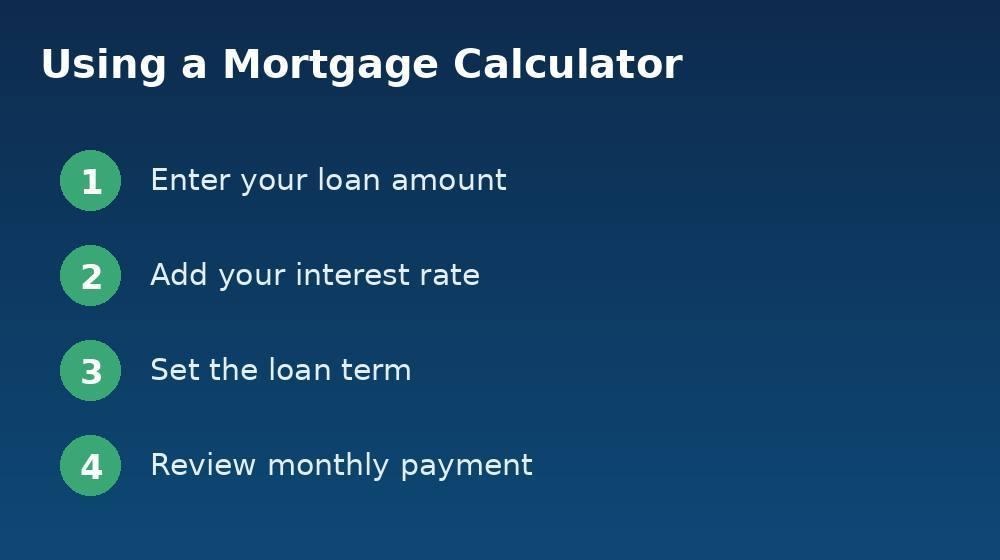

Knowing your numbers up front prevents surprises. A mortgage calculator or mortgage payment calculator shows your estimated monthly cost once you enter the loan amount, rate, and term. Running these figures first tells you whether refinancing actually improves your situation.

How to Apply and Get the Best Deal

Once the math works, it’s time to shop. Compare offers from more than one mortgage lender and at least one mortgage broker, since terms vary widely. Get your mortgage pre approval in hand before you apply for a mortgage, and gather your income and asset documents early. Special programs are worth a look too: a va loan offers strong terms for eligible veterans, and first time home buyer programs can lower upfront costs for newer buyers who later refinance. Preparing your paperwork and credit ahead of time is the surest way to lock in the best terms.

Ready to run your own numbers? Try our free refinance tools and compare today’s offers before you make a move.