Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Buying a first home is exciting, but it can also feel overwhelming when there are loan options, interest rates, down payment requirements, and closing costs to understand. For many new buyers, researching first time home buyer programs is one of the best places to start. These programs can help buyers understand what mortgage options may be available, especially if they are worried about saving a large down payment or qualifying for a loan for the first time.

For Utah buyers, the process can feel even more specific because housing prices, local lenders, and assistance options may vary by location. Someone researching first time home buyer loans Utah may not only be looking for general mortgage information, but also trying to understand what applies in Utah specifically. A strong first step is learning the basic mortgage terms, comparing programs, and understanding how interest rates, closing costs, and pre-approval affect the total cost of buying a home.

The phrase first time home buyer loans does not refer to only one type of mortgage. Instead, it usually describes loan options that may be useful for people purchasing their first home. These can include conventional loans, FHA loans, and other programs that may offer lower down payment requirements or more flexible qualification standards. A first time buyer mortgage should be evaluated based on the buyer’s credit, income, debt, savings, and long-term financial goals.

Many buyers want to find the best first time home buyer loans, but the “best” loan is not always the one with the lowest advertised interest rate. A better loan is one that fits the buyer’s full financial situation. That means looking at the interest rate, monthly payment, mortgage insurance, closing costs, down payment requirement, and lender fees. A first time home buyer mortgage should be compared carefully before a buyer decides which option is the best fit.

An FHA loan first time home buyer option is often popular because FHA loans may allow lower down payments and more flexible credit requirements than some conventional mortgage products. This can make FHA loans appealing to buyers who have steady income but limited savings or a shorter credit history. For many new buyers, FHA financing can make the idea of purchasing a home feel more realistic.

A buyer researching FHA first time home buyer information may also want Utah-specific guidance. For example, someone searching for FHA loan Utah first time buyer options may be trying to understand whether FHA financing works well in their local market. FHA loans can be helpful, but they can also include mortgage insurance and specific property requirements. Buyers should compare FHA loans with other mortgage options before assuming it is automatically the right choice.

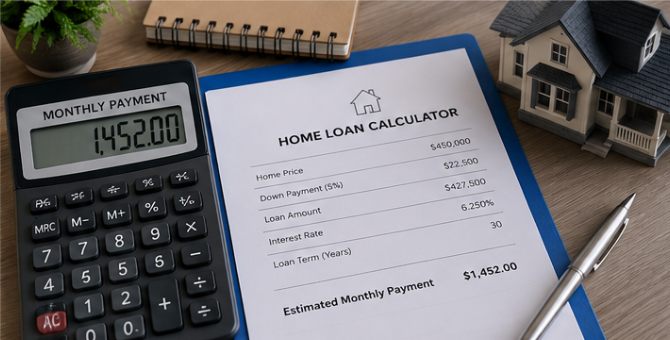

Before applying for a loan, buyers should estimate what they can afford. A first time home buyer mortgage calculator can help estimate a monthly payment based on home price, down payment, loan amount, interest rate, taxes, and insurance. This is useful because the purchase price alone does not show the full cost of homeownership. A buyer also needs to consider utilities, repairs, maintenance, moving costs, and emergency savings.

Other tools can also be helpful. A first time home buyer calculator or first time home buyer loan calculator can give buyers a clearer starting point before they talk to a lender. These calculators do not replace a formal loan estimate, but they can help buyers avoid shopping outside their realistic price range. They can also help buyers test different scenarios, such as making a larger down payment or comparing a lower interest rate.

Interest rates are one of the biggest factors in a mortgage payment. A first time home buyer interest rate affects both the monthly payment and the total amount of interest paid over the life of the loan. Even a small rate difference can matter over time, especially on a long-term mortgage. This is why buyers often compare first time buyer mortgage rates before deciding when and where to apply.

Utah buyers may also search for first time home buyer rates or first time home buyer mortgage rates Utah when they want local rate information. Rates can change based on the overall market, credit score, loan type, down payment, and lender. A buyer with a strong application may qualify for better terms than someone with higher debt or weaker credit. This is one reason it can be useful to compare lenders and request more than one quote.

Getting first time home buyer pre approval can make the home search more focused. Pre-approval gives a buyer an estimate of how much they may be able to borrow based on financial information like income, assets, debts, and credit. It can also help the buyer understand which loan types may be realistic. While pre-approval is not the same as final approval, it is an important step before making an offer on a home.

Pre-approval can also make a buyer more competitive. Sellers may take an offer more seriously when the buyer has already spoken with a lender and has documentation showing they may qualify for financing. For first-time buyers, this step can reduce uncertainty. It also gives them time to fix possible issues, gather documents, and better understand the mortgage process before they are under contract.

Choosing among first time home buyer lenders is an important part of the buying process. Different lenders may offer different rates, fees, loan programs, and levels of support. Some buyers may prefer a local lender who understands Utah housing conditions, while others may compare banks, credit unions, online lenders, and mortgage brokers. The right lender should be able to explain loan options clearly and help the buyer understand the true cost of the mortgage.

A search for best mortgage lenders for first time buyers Utah can be a helpful starting point, but buyers should still compare actual loan estimates. A lender with strong advertising may not always offer the best fit for every borrower. Buyers should ask about interest rates, annual percentage rate, lender fees, estimated closing costs, down payment requirements, and whether any first-time buyer programs or assistance options may apply.

One of the biggest barriers for first-time buyers is the upfront cost of buying a home. A low down payment mortgage Utah option may help buyers purchase sooner, especially if they have stable income but limited savings. However, a lower down payment may also lead to mortgage insurance or a higher monthly payment, so buyers should compare the short-term and long-term costs carefully.

Many buyers also research Utah closing cost assistance because closing costs can add thousands of dollars to the amount needed at closing. Utah first time buyer closing costs may include lender fees, appraisal fees, title fees, prepaid taxes, homeowners insurance, and other charges. Buyers should also understand how much down payment for house in Utah may be required based on the loan type they choose. Planning early for both the down payment and closing costs can help prevent last-minute financial stress.

A Utah mortgage rate buydown may be another option for some buyers. A rate buydown involves paying upfront to reduce the interest rate, either temporarily or permanently depending on the structure. This can lower the monthly payment, which may be helpful for buyers who expect their income to increase or who want a lower payment during the first years of ownership.

However, a rate buydown is not always the best choice. Buyers should compare the upfront cost of the buydown with the monthly savings. They should also consider how long they plan to stay in the home. If the buyer sells or refinances quickly, the buydown may not provide enough savings to justify the cost. This is why it is important to review the numbers with a lender before choosing this strategy.

Learning how to buy a house in Utah first time buyer style means breaking the process into clear steps. A buyer should start by reviewing their budget, checking credit, saving for upfront costs, researching loan options, and getting pre-approved. After that, they can compare homes, work with a real estate agent, make an offer, complete inspections, finalize the mortgage, and close on the property.

The process can feel complicated, but it becomes easier when buyers understand each step. First-time buyers should avoid rushing into a loan without comparing options. They should also avoid focusing only on the monthly payment without understanding closing costs, interest rates, mortgage insurance, and long-term affordability. The more informed the buyer is before applying, the better prepared they will be to make a confident decision.

For more local mortgage information, readers can compare Utah mortgage rate information. Buyers who want to understand FHA loans can also learn about FHA loan basics from HUD.

Overall, first time home buyer programs can help Utah buyers better understand their mortgage options, especially when they are unsure where to start. By researching loan types, using calculators, comparing lenders, reviewing down payment needs, and learning about closing cost assistance, first-time buyers can make more informed decisions. The goal is not just to buy a home, but to choose a mortgage that fits the buyer’s budget and long-term financial stability.