Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Buying a home for the first time in Utah can feel exciting, stressful, and confusing at the same time. You may be watching rates, comparing loan types, wondering how much cash you need, and trying to decide whether now is the right time to apply. That is why understanding utah first time home buyer mortgage rates matters. Your rate affects your monthly payment, your buying power, and the type of loan that makes the most sense for your budget.

This guide is designed for buyers who want a clear starting point. Instead of only looking at advertised rates, first-time buyers should compare loan programs, down payment requirements, credit standards, and available assistance. The right strategy is not just finding the lowest number online. It is finding a realistic mortgage plan that fits your income, savings, location, and long-term goals.

First Time Home Buyer Programs Utah Buyers Should Compare

The best place to start is with first time home buyer programs utah residents may qualify for. These programs are built to reduce some of the biggest barriers to homeownership, especially the down payment and closing costs. Some buyers may qualify for state or local assistance, while others may qualify for federal loan options such as FHA, USDA, or VA financing.

When researching first time home buyer programs, remember that each program has its own rules. Some programs require homebuyer education. Others have income limits, purchase price limits, credit score requirements, or property location rules. A program that works for one buyer may not work for another, so the smart move is to compare several options before committing to one path.

Utah buyers should also think about timing. Assistance funds can change, program rules can update, and mortgage rates move daily. That means a buyer should not wait until making an offer to ask about utah down payment assistance programs. Asking early gives the lender time to confirm whether the buyer qualifies and whether the program can be paired with the selected loan type.

First Time Home Buyer Loans and Low Down Payment Options

There are several types of first time home buyer loans that can work in Utah. FHA loans are often popular with buyers who have limited savings or credit challenges. Conventional loans may work well for buyers with stronger credit and stable income. USDA loans may help buyers in eligible rural areas. VA loans may help eligible service members, veterans, and certain surviving spouses purchase with major benefits.

One common search is fha loan first time home buyer because FHA loans are widely known for lower down payment requirements. An fha first time home buyer option can be useful when the buyer has steady income but does not have a large amount saved. FHA loans still include mortgage insurance and property requirements, so buyers should compare the full monthly payment, not just the down payment.

Some buyers are also looking for first time home buyer loans with zero down. True zero-down options are usually limited to eligible VA or USDA borrowers. A no down payment first time home buyer path can be powerful, but it is not automatically the cheapest choice. Buyers should compare the monthly payment, funding fees, mortgage insurance, closing costs, and long-term interest before deciding.

How First Time Home Buyer Mortgage Rates Affect Affordability

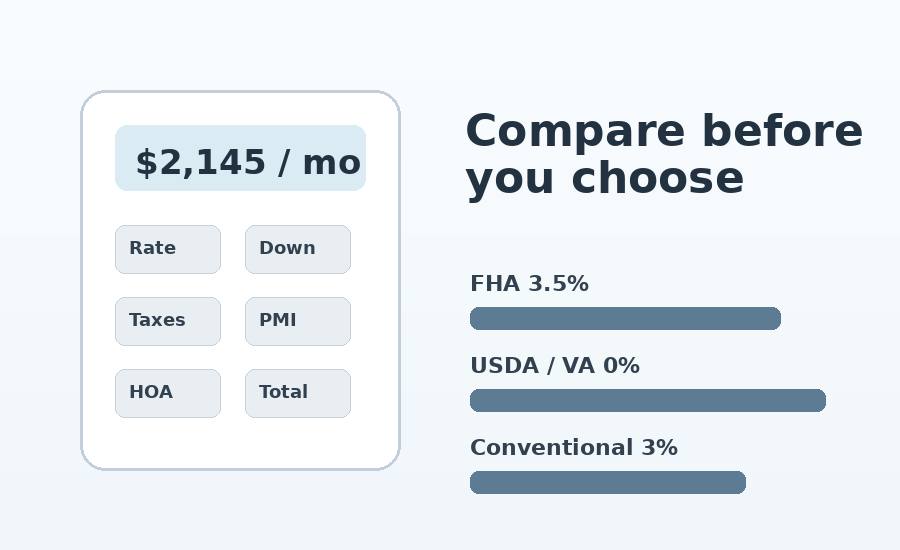

Your first time home buyer interest rate is one of the biggest factors in your payment. Even a small rate difference can change what you can afford. That is why it helps to compare first time buyer mortgage rates from more than one lender instead of relying on a single quote.

When people search for first time home buyer rates, they often see national averages. Those averages can be helpful, but your personal quote depends on your credit score, down payment, debt-to-income ratio, loan type, property type, and whether you pay points. In other words, first time home buyer mortgage rates are personal. Two Utah buyers can apply on the same day and receive different offers.

For Utah specifically, utah first time home buyer mortgage rates may track national trends, but local lenders can still vary in fees, service, and program access. This is why first-time buyers should compare the annual percentage rate, lender fees, closing costs, and loan estimate details before choosing a lender.

Use a Mortgage Calculator Before You Tour Homes

A first time home buyer mortgage calculator helps turn confusing numbers into a realistic monthly estimate. Before touring homes, buyers should test different prices, down payments, interest rates, property taxes, insurance, mortgage insurance, and HOA fees. This is especially important in Utah because monthly affordability can change quickly from one city or county to another.

A first time buyer mortgage calculator can also help compare loan types. For example, a buyer could compare FHA with 3.5% down, conventional with 3% down, and USDA or VA if eligible. A first time home buyer loan calculator can show whether a lower down payment creates a higher monthly payment because of mortgage insurance or fees.

A first time home buyer down payment calculator is useful for estimating how much cash you need before closing. Many buyers only think about the down payment, but the final amount can also include closing costs, prepaid taxes, insurance, appraisal fees, inspection costs, and reserves. Understanding the full number helps prevent surprises.

Pre-Approval Gives First-Time Buyers a Stronger Start

Getting first time home buyer pre approval should happen before serious house hunting. Pre-approval is stronger than a basic prequalification because the lender reviews income, credit, assets, and debt. It gives the buyer a clearer price range and helps sellers know the offer is backed by a lender review.

Searches like mortgage pre approval first time home buyer are common because many new buyers are not sure when to start. The answer is usually earlier than expected. A pre-approval can reveal credit issues, debt-to-income concerns, or missing documents before the buyer is under contract. That preparation can save time and stress.

Pre-approval is also the point where buyers can compare utah first time home buyer loans more seriously. Instead of guessing which program sounds best, the lender can help compare FHA, conventional, VA, USDA, and assistance options based on the buyer’s real numbers.

How Much Down Payment Should a First-Time Buyer Expect?

Many buyers research the average down payment on a house for first time buyer because they assume 20% down is required. In reality, many first-time buyers use lower down payment loans. FHA may allow a low down payment, conventional programs may allow low down payments for qualified buyers, and eligible VA or USDA borrowers may be able to buy with zero down.

The key is not only how much you can put down. The key is how your down payment affects your total payment and your financial safety after closing. A larger down payment may lower the monthly payment, but using all your savings can leave you unprepared for repairs, moving costs, or emergencies.

Finding the Best Mortgage Lenders for First-Time Home Buyers

The best mortgage lenders for first time home buyers are usually the lenders who explain the process clearly, compare multiple options, and understand assistance programs. The lowest advertised rate is not always the best deal if the fees are higher or the lender does not offer the right program.

When comparing first time home buyer lenders, ask about FHA, VA, USDA, conventional low down payment loans, Utah assistance programs, estimated closing costs, and rate lock options. A good lender should be able to show the differences in writing, not just tell you which option is popular.

A first time buyer mortgage should be chosen based on the full picture: payment, cash to close, interest rate, APR, mortgage insurance, loan flexibility, and long-term goals. For some buyers, the lowest cash-to-close option matters most. For others, the best choice is the loan with the lowest total long-term cost.

Final Takeaway for Utah First-Time Buyers

Buying your first home in Utah becomes less overwhelming when you slow the process down and compare the numbers. Start with pre-approval, review assistance options, use calculators, and compare more than one lender. The best mortgage strategy is the one that helps you buy responsibly without stretching your monthly budget too far.

If you are comparing utah first time home buyer mortgage rates, do not stop at the rate alone. Look at the loan program, down payment, assistance options, closing costs, and how the payment fits your life after move-in. With the right preparation, first-time buyers can move from uncertainty to a clear plan for homeownership.