Comprehensive Guide to Mortgage Pre-Approval and First-Time Homebuyer Loans in Utah

Buying a home in Utah is an exciting journey, but understanding Mortgage Pre-Approval Utah is essential for first-time buyers to navigate the mortgage process confidently. Understanding mortgage pre approval, prequalify for mortgage, and first time home buyer loans is essential to make informed decisions. In this guide, we’ll break down each step, explain key terms, and provide helpful tips to get you started.

Mortgage Pre-Approval in Utah

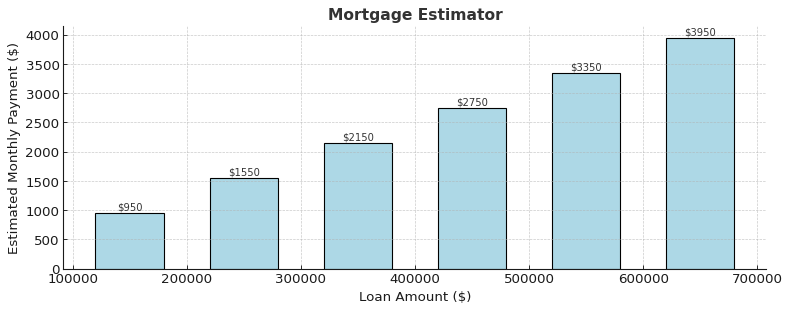

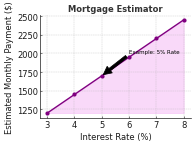

Mortgage pre approval is the process where a lender evaluates your financial background to determine how much you can borrow. Obtaining pre-approval gives you a clear budget and strengthens your offer when bidding on a home. Using a mortgage pre approval calculator can help estimate your potential loan amount based on income, debts, and credit score.

Most lenders require documentation such as pay stubs, bank statements, and tax returns during pre-approval. By being prepared, you can speed up the process and increase your chances of approval. Other related terms to keep in mind are mortgage loan pre approval and loan pre approval, which are commonly searched by Utah residents.

Mortgage Pre-Approval Utah: Tips for a Smooth Process

- Gather all necessary documents before applying.

- Use online calculators to estimate affordability and monthly payments.

- Apply with reputable lenders to avoid delays.

- Check your credit score ahead of time to address any issues.

Mortgage Pre-qualification Utah: How It Differs from Pre-Approval

Prequalify for mortgage is a preliminary step before pre-approval. While it doesn’t guarantee a loan, it provides insight into your eligibility. Keywords like get pre-qualified for a home loan and mortgage pre-qualification are relevant when learning about this stage.

During prequalification, lenders evaluate your income, debts, and credit history to estimate the loan amount you might qualify for. Tools such as an online mortgage pre approval or mortgage qualification calculator can make this step easier.

Get an Mortgage Qualification Calculator here: rocketmortgage.com: Utah Homebuyer’s Guide: Mortgage Pre-Approval and First-Time Loan OptionsUnderstanding Pre-qualification vs. Pre-Approval

Pre-qualification is generally faster and less formal than pre-approval, but it’s still a helpful first step. After pre-qualification, you can move on to full pre-approval, which solidifies your loan options. Using tools like a home affordability calculator can also help you understand what homes are within your budget.

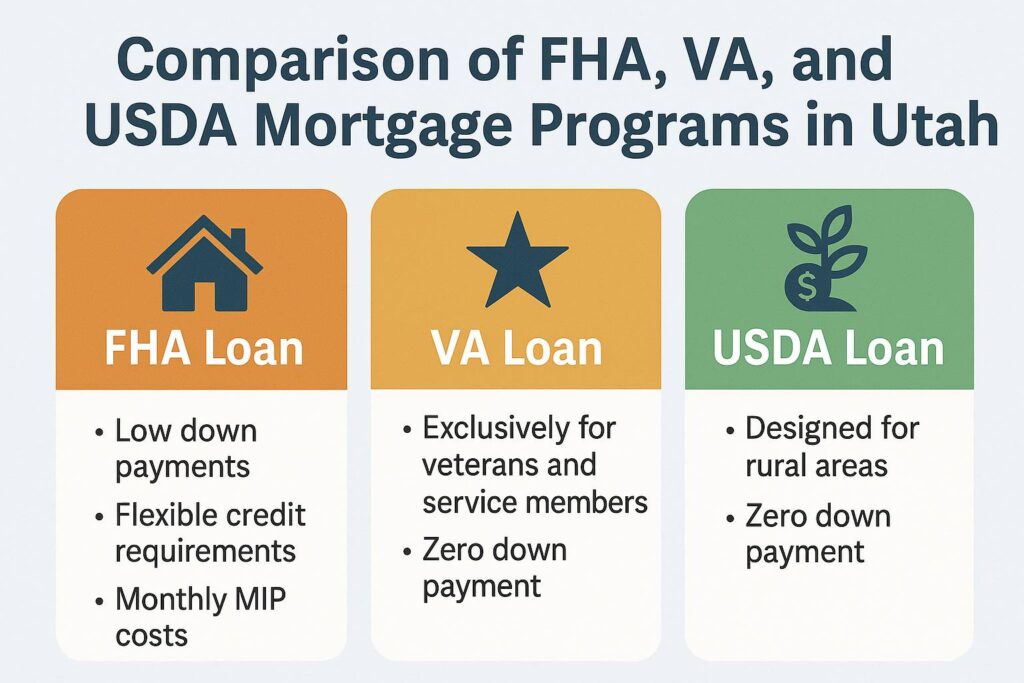

First-Time Homebuyer Loans in Utah

First time home buyer loans and first time home buyer programs provide opportunities specifically for first-time buyers in Utah. Many programs offer down payment assistance, lower interest rates, or special eligibility criteria. Keywords such as first time home owners loan and zero down home loans are often searched by people looking for these programs.

Exploring Utah-specific programs is important. For example, checking 1st time home buyer programs and comparing loan options can help you maximize your benefits. Calculators like the mortgage pre approval calculator and home buying calculator can help you determine how much you can afford.

Tips for First-Time Homebuyers

- Research state-specific programs for first-time buyers.

- Compare different loan types, including FHA and conventional loans.

- Use calculators to plan your budget and monthly payments.

- Consult with local mortgage professionals for personalized advice.

Tips for a Smooth Home Buying Process

- Check Your Credit Score: Lenders use your credit history to determine eligibility. Use a mortgage approval calculator to see where you stand.

- Organize Your Documents: Have tax returns, pay stubs, and bank statements ready for pre-approval.

- Use Online Calculators: Tools like home buying calculator and home affordability calculator help estimate your payments and affordability.

- Explore Utah Programs: Take advantage of first time home buyer programs and loan options for new buyers.

- Consult Experts: Local mortgage lenders and advisors can guide you through the get pre approved for a mortgage and mortgage pre-qualification process.

Conclusion

Navigating the mortgage process in Utah doesn’t have to be complicated. By understanding mortgage pre approval, prequalifying for mortgage, and first time home buyer loans, you can approach homebuying with confidence. Start by checking your eligibility, using online calculators, and exploring Utah-specific programs. With proper planning and the right resources, Utah homeownership is within reach!

{kind=link}

{kind=link}