Buying a home in Utah is exciting, but many buyers are surprised by how much money they may need before closing day. Most people focus on the down payment, but closing costs are another major part of the home-buying budget. A closing cost calculator Utah buyers can use is helpful because it gives a clearer estimate of the fees, prepaid expenses, taxes, insurance, and lender charges that may be due at closing.

If you are comparing mortgage rates Utah buyers are seeing today, researching Utah mortgage lenders, or trying to decide which loan program is right for you, understanding closing costs should be one of your first steps. The amount you need to close can vary depending on your loan type, purchase price, credit profile, property taxes, insurance, and whether the seller agrees to help pay some of your costs.

What Is a Mortgage Closing Costs Calculator?

A mortgage closing costs calculator helps buyers estimate the extra expenses involved in purchasing a home. These costs are separate from the down payment and may include lender fees, appraisal fees, title insurance, escrow deposits, prepaid homeowners insurance, prepaid property taxes, and recording fees. While the exact amount can change from one transaction to another, using a calculator early can help you avoid surprises later.

A mortgage closing costs calculator is especially useful before you make an offer on a home. It can help you understand the total amount of cash needed, not just the monthly mortgage payment. This is important because a buyer may qualify for the payment but still need to plan for the money required at closing.

Learn more about Utah mortgage options.

Learn more about closing cost disclosures from the Consumer Financial Protection Bureau.

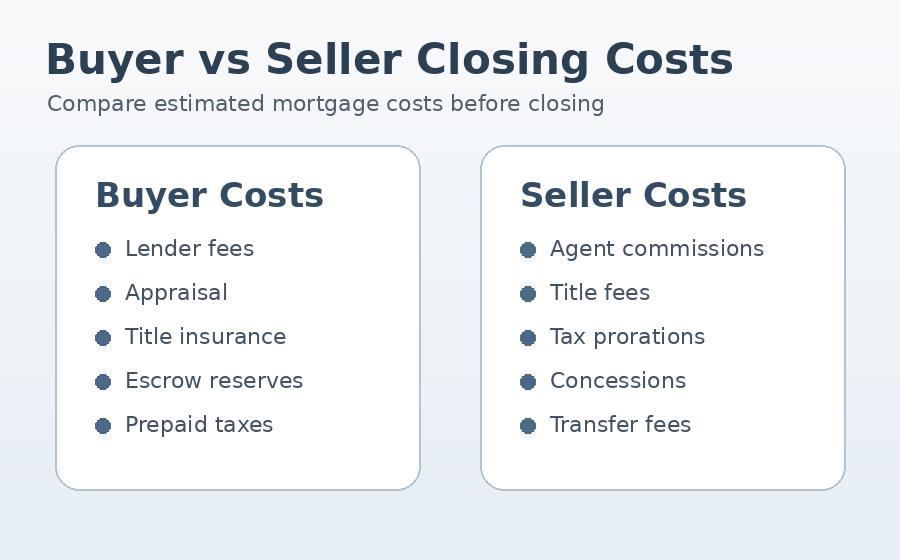

Closing Cost Calculator for Buyer Expenses

A closing cost calculator for buyer expenses focuses on what the homebuyer may need to pay. Buyer closing costs can include the loan origination fee, appraisal, credit report, title fees, lender’s title insurance, prepaid interest, escrow setup, homeowners insurance, and property tax reserves. These costs are usually listed on the Loan Estimate after a buyer applies for a mortgage.

For a first time home buyer mortgage, these numbers can feel overwhelming at first. However, breaking them down makes the process much easier to understand. A first time home buyer loan may have a lower down payment requirement, but the buyer still needs to prepare for closing costs unless those costs are covered by seller concessions, lender credits, gift funds, or assistance programs.

A home affordability calculator can also help buyers estimate a realistic price range. However, affordability is not only about the monthly payment. Buyers should also consider the down payment, closing costs, insurance, taxes, mortgage insurance, and any upfront expenses that may come with the loan.

Closing Cost Calculator for Seller Expenses

A closing cost calculator for seller expenses estimates the costs a seller may pay when selling a home. Seller costs may include real estate agent commissions, title fees, prorated property taxes, transfer fees, and any seller concessions negotiated in the purchase contract.

Seller concessions can be helpful for buyers who have enough income to qualify for the loan but need help reducing the cash needed at closing. For example, a seller may agree to pay part of the buyer’s closing costs. This can make a home purchase more realistic for buyers using a low down payment mortgage or first time home buyer down payment assistance.

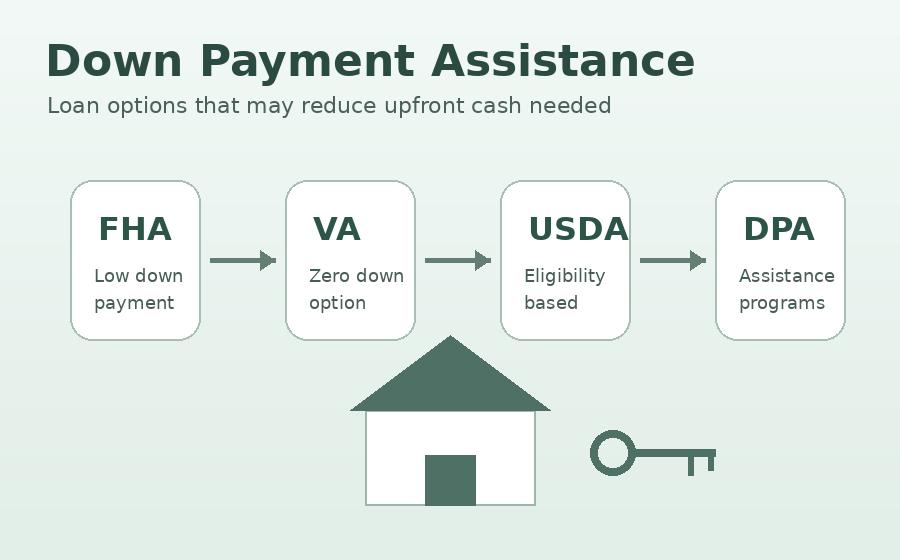

VA Loan Closing Costs

A closing cost calculator VA loan estimate can help eligible veterans, active-duty service members, and certain surviving spouses understand what costs may still apply with a VA loan. VA loans are popular because qualified borrowers may be able to purchase a home with no down payment. However, a no down payment mortgage does not always mean no money is needed at closing.

VA loan requirements include eligibility based on military service, lender approval, and property standards. Buyers may still need to pay closing costs, prepaid expenses, and a VA funding fee unless they are exempt. For borrowers who qualify, a VA loan can be one of the strongest zero down mortgage options available.

Learn more about VA home loans.

FHA Loan Requirements

FHA loan requirements are often more flexible than some conventional loan guidelines, which is why FHA loans are popular with first-time buyers. FHA loans may allow lower down payments and may be available to buyers with less-than-perfect credit. This can make them a good option for buyers who have steady income but limited savings.

However, FHA loans usually include mortgage insurance, and the property must meet certain standards. Buyers should compare FHA loans with other options to understand the full cost of the loan, including closing costs, mortgage insurance, and monthly payment.

Learn more about FHA loans from HUD.

USDA Loan Requirements

USDA loan requirements are important for buyers considering homes in eligible rural or suburban areas. Many buyers are surprised to learn that some properties outside major city centers may qualify for USDA financing. USDA loans may offer no down payment options for eligible borrowers and properties.

USDA loan eligibility usually depends on the property location, household income limits, and borrower qualifications. Buyers interested in this option should verify both the home’s location and their income eligibility before assuming they qualify.

Check USDA property and income eligibility.

Conventional Loan Requirements

Conventional loan requirements can vary by lender and loan program, but buyers usually need to meet guidelines for credit score, income, debt-to-income ratio, assets, and down payment. Conventional loans may be a good fit for borrowers with stronger credit and stable income.

Some conventional programs allow low down payments, which can make them attractive for first-time buyers. However, if the down payment is below 20%, private mortgage insurance may be required. Buyers should compare conventional loans with FHA, VA, and USDA options to decide which program offers the best overall fit.

First Time Home Buyer Down Payment Assistance

First time home buyer down payment assistance can help qualified buyers reduce the amount of money needed upfront. Some down payment assistance programs may help with the down payment, closing costs, or both. These programs may come in the form of grants, forgivable loans, deferred-payment loans, or second mortgages.

For buyers who are close to qualifying but do not have enough saved, down payment assistance programs can make a major difference. A Salt Lake City mortgage lender who understands Utah programs may be able to explain what options are available and how they can be combined with FHA, VA, USDA, or conventional loans.

Finding a Mortgage Lender Near Me

Searching for a mortgage lender near me is a common step when buyers want personal guidance. Online tools are helpful, but mortgages are not one-size-fits-all. A local mortgage lender can help explain estimated closing costs, loan options, current Utah mortgage rates, and which programs may fit your financial situation.

A mortgage broker Salt Lake City buyers can work with may also help compare multiple loan options. This can be useful when looking at rates, fees, lender credits, and different mortgage programs. The lowest advertised rate is not always the lowest overall cost, so buyers should compare the full loan estimate.

Mortgage Pre Approval Online

Getting a mortgage pre approval online can help buyers understand what they may qualify for before they start shopping for homes. During pre-approval, the lender typically reviews income, credit, debts, assets, and employment. This process can also help determine whether FHA, VA, USDA, or conventional financing is the best fit.

Once buyers know their estimated price range, monthly payment, and cash needed to close, they can shop with more confidence. Pre-approval can also make an offer stronger because it shows sellers that the buyer has already started the mortgage process.

Final Thoughts on Utah Closing Costs

A closing cost calculator Utah buyers can use is a great starting point, but it should not replace a detailed estimate from a mortgage professional. Closing costs can vary based on the loan type, property, purchase price, lender, taxes, insurance, and negotiated seller concessions.

If you are comparing Utah mortgage lenders, looking for a Salt Lake City mortgage lender, or trying to understand how much cash you need to buy a home, the best step is to review your options early. Whether you are considering a low down payment mortgage, no down payment mortgage, zero down mortgage, FHA loan, VA loan, USDA loan, conventional loan, or down payment assistance, knowing the numbers upfront can make the home-buying process much less stressful.