Choosing the right mortgage lender Salt Lake City homebuyers can trust is one of the most important decisions you’ll make when purchasing your first home. While it’s exciting to browse listings and imagine life in a new home, many first-time buyers make costly mistakes before they ever submit an offer. From selecting the wrong loan program to focusing only on interest rates, these missteps can lead to higher costs and unnecessary stress throughout the home-buying process.

The best mortgage lender does more than provide financing—they serve as a trusted advisor who helps you compare loan options, understand current home mortgage rates, explore FHA financing, and determine which mortgage best fits your financial goals. Whether you’re searching for a mortgage lender Utah buyers recommend or comparing the best mortgage lenders Utah has to offer, working with an experienced local lender can make your path to homeownership much smoother.

In this guide, you’ll learn how to avoid the most common first-time home buyer mistakes, compare mortgage options with confidence, and choose a lender who can help you navigate Utah’s competitive housing market.

Common First-Time Home Buyer Mistakes

Many first-time buyers assume they should start by looking at homes online. In reality, your first step should be speaking with a qualified mortgage professional. Some of the most common mistakes include:

- Shopping before getting pre-approved.

- Choosing the first lender you find online.

- Focusing only on the interest rate instead of total loan costs.

- Not comparing multiple loan programs.

- Overlooking available first time home buyer programs Utah offers.

Taking the time to compare lenders and financing options can help you avoid these costly mistakes while making your home purchase much smoother.

The Consumer Financial Protection Bureau (CFPB) provides an excellent guide to the home-buying process and explains why comparing lenders is important: https://www.consumerfinance.gov/owning-a-home/

How to Choose the Best Mortgage Lender in Salt Lake City

Finding the best mortgage lenders Utah has to offer isn’t just about getting the lowest rate. Great lenders provide education, communication, and personalized guidance throughout the loan process.

When comparing a mortgage lender Salt Lake City homebuyers trust, ask questions like:

- How long have you helped Utah homebuyers?

- What loan programs do you recommend for first-time buyers?

- Do you offer pre-approvals before I begin shopping?

- Can you explain all estimated closing costs?

- How often will you communicate during the loan process?

If you’re searching online for the best mortgage lender near me, look for local experience, positive reviews, responsive communication, and knowledge of Utah’s housing market.

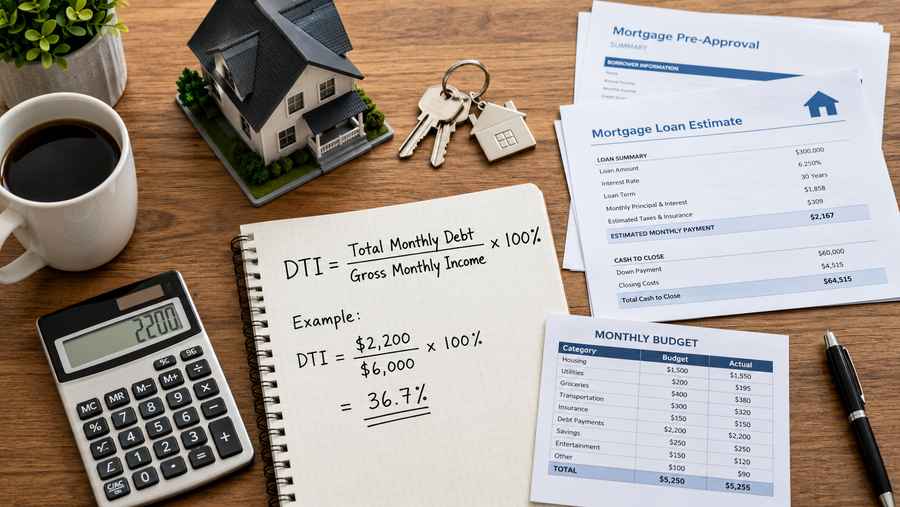

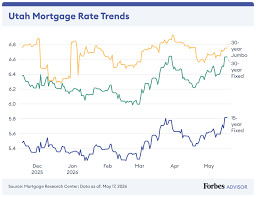

Mortgage Lender Utah: Compare More Than Interest Rates

Many buyers immediately compare current home mortgage rates and current housing interest rates. While rates certainly matter, they are only one piece of the financing puzzle. A mortgage quote also includes:

- Loan origination fees

- Closing costs

- Mortgage insurance

- Loan term

- Annual Percentage Rate (APR)

- Estimated monthly payment

When comparing home loan interest rates, ask each lender for a complete loan estimate instead of simply requesting today’s rate. Sometimes a slightly higher interest rate comes with lower closing costs, making it the better financial decision. A trusted mortgage lender Utah buyers recommend will explain every cost so you can make an informed decision.

The Consumer Financial Protection Bureau explains how to read a Loan Estimate and compare mortgage offers from multiple lenders. Read up on it on their website here: https://www.consumerfinance.gov/owning-a-home/loan-estimate/

First-Time Utah Home Buyer Programs Can Make Homeownership More Affordable

Many buyers are surprised to learn they may qualify for programs designed specifically for first-time homeowners. Several first time home buyer programs Utah lenders offer can help reduce upfront costs through down payment assistance or affordable financing.

Depending on your qualifications, you may be eligible for:

- Down payment assistance

- Reduced closing costs

- Low down payment conventional loans

- Government-backed financing

If you’re searching for a first time home buyer loan, ask your lender to explain every available option before choosing a mortgage. Many first time borrowers discover that these programs make purchasing a home much more affordable than they expected.

FHA Loan Utah: Is FHA Financing Right for You?

An FHA loan is one of the most popular mortgage options for first-time homeowners. Because FHA loans are insured by the Federal Housing Administration, they often allow Utah resident to take advantage of:

- Lower down payments

- Flexible credit requirements

- Competitive financing options

- Easier qualifications

However, FHA financing isn’t the right solution for everyone.

A knowledgeable lender can compare FHA financing with conventional loans and determine which option best fits your financial goals. Before applying, it’s also helpful to use an FHA loan calculator to estimate your monthly payment, including mortgage insurance and taxes.

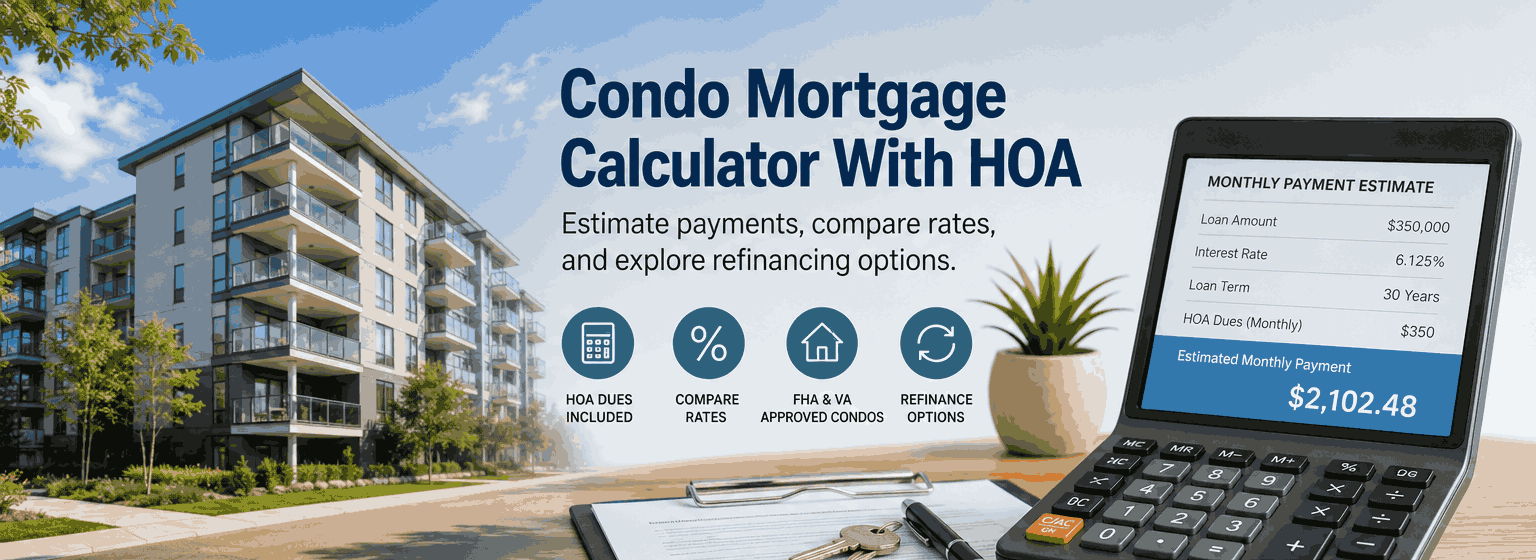

Using a Mortgage Payment Calculator Before Shopping for Homes

Knowing your monthly payment before making an offer helps you shop with confidence. A mortgage payment calculator gives buyers a better understanding of what they can comfortably afford based on today’s market. Many buyers also use a mortgage price calculator to compare different purchase prices and see how changes in the down payment or interest rate affect their monthly payment.

While calculators provide excellent estimates, your lender can provide a personalized payment estimate using your actual income, credit score, and loan program.

First Time Home Buyer Loans: Understanding Your Options

There are several first time home buyer loans available today.

The right loan depends on your financial goals, available down payment, and long-term plans. Some buyers searching for a first time home owners loan may benefit from FHA financing, while others qualify for conventional financing with competitive rates. Similarly, a first home buyers loan may refer to several different mortgage programs rather than one specific loan product.

Working with an experienced lender helps ensure you’re matched with the financing option that best supports your budget.

Why Local Experience Matters

The Salt Lake City housing market continues to evolve, and local knowledge matters. A lender who understands neighborhood values, Utah property taxes, local appraisal requirements, and regional housing trends can help buyers navigate the process more efficiently than a lender unfamiliar with the market.

Choosing a local mortgage professional often results in faster communication, better coordination with your real estate agent, and a smoother closing experience.

In Summary

Buying your first home doesn’t have to be overwhelming. By avoiding common first-time buyer mistakes, comparing lenders carefully, and understanding your financing options, you’ll be in a much stronger position to purchase your home with confidence.

Whether you’re comparing current housing interest rates, researching first time home buyer programs, exploring FHA loans, or searching for the best mortgage lender in Salt Lake City, investing time in choosing the right lender is one of the smartest decisions you’ll make.

The best mortgage isn’t simply the one with the lowest advertised rate—it’s the one that fits your financial goals, monthly budget, and long-term plans. A knowledgeable local lender can help you find that solution while making the home-buying process easier from pre-approval to closing.