Buying your first home is exciting, but it can also feel confusing when you are trying to understand loan options, down payments, mortgage rates, and pre-approval requirements. A first time home buyer mortgage calculator can help you estimate what you may be able to afford before you begin seriously shopping for homes. For many Utah buyers, this is one of the best first steps because it allows you to compare possible monthly payments, loan amounts, interest rates, and down payment options before speaking with a lender.

A mortgage calculator is especially useful because your monthly housing payment is usually more than just the cost of the home loan. It may also include property taxes, homeowners insurance, mortgage insurance, and possibly HOA fees. By estimating these costs early, first-time buyers can get a clearer picture of what fits comfortably within their budget.

First Time Home Buyer Loans

Many buyers begin their research by looking for first time home buyer loans. These loans are designed to help people purchase their first home, often with lower down payment options or more flexible qualification standards. A first time home loan can come in several forms, including FHA, USDA, VA, and conventional mortgage options.

Some buyers may search for a first home buyers loan or a first time home owners loan, which usually means they are looking for mortgage options specifically designed for people buying their first property. While these phrases are slightly different, they all point to the same main goal: finding a loan that makes homeownership more affordable and easier to understand.

The best first time home buyer loans are not always the same for every borrower. One buyer may need a loan with a low down payment, while another may be focused on getting the lowest possible interest rate. Another buyer may need flexible credit guidelines. Because every financial situation is different, it is important to compare options carefully before choosing a mortgage.

Learn More About Utah Mortgage Options

First Time Home Buyer Lenders

Choosing the right lender is just as important as choosing the right loan. Experienced first time home buyer lenders can help explain loan programs, estimate monthly payments, review credit requirements, and guide buyers through pre-approval. A good lender should help you understand more than just the interest rate. They should also explain closing costs, mortgage insurance, down payment options, and how much home you can realistically afford.

Many buyers also search for the best home loan lenders for first time buyers because they want a lender who understands the challenges of buying a first home. First-time buyers often have questions about credit scores, employment history, debt-to-income ratio, and how much money they need to bring to closing. Working with a lender who explains these steps clearly can make the process much less stressful.

First Time Home Buyer Programs

In addition to mortgage loans, many buyers search for first time home buyer programs. These programs may help with down payments, closing costs, or other parts of the home buying process. Some programs are national, while others are offered by state or local organizations. Utah buyers should review both general home buying assistance and Utah-specific programs to see what may be available.

Government Home Buying Assistance Programs

Utah First-Time Homebuyers Assistance Program

These programs can be helpful, but buyers should remember that eligibility rules vary. Some programs have income limits, location requirements, purchase price limits, or rules about whether you have owned a home before. A mortgage lender can help you understand whether you may qualify.

FHA First Time Home Buyer

A popular option for many new buyers is an fha loan first time home buyer program. FHA loans are often attractive because they may allow lower down payments and more flexible credit requirements than some conventional loans. Many people search for fha first time home buyer information because FHA financing is commonly associated with first-time homeownership.

However, FHA loans are not automatically the best choice for everyone. Buyers should compare the monthly payment, mortgage insurance, interest rate, and total loan cost. A first-time home buyer mortgage calculator can help compare FHA loan estimates with other loan types so buyers can see which option may work best.

USDA First Time Home Buyer

Another option some buyers consider is a usda first time home buyer loan. USDA loans may be available for eligible buyers purchasing homes in qualifying rural or suburban areas. One reason buyers like USDA loans is that some qualified borrowers may be able to purchase a home without a down payment.

This makes USDA financing appealing for buyers searching for first time home buyer loans with zero down. It may also be helpful for buyers looking for no down payment first time home buyer options. However, USDA loans have specific income and property location requirements, so buyers should confirm eligibility with a lender before assuming this loan will work for them.

First Time Home Buyer Down Payment Calculator

One of the most helpful tools for new buyers is a first time home buyer down payment calculator. This type of calculator can help estimate how much money you may need upfront based on the purchase price and loan program. For example, a buyer using an FHA loan may have a different down payment requirement than a buyer using a conventional loan.

A down payment calculator can also show how changing your down payment affects your monthly payment. A larger down payment may reduce your loan amount and monthly cost, while a smaller down payment may help you buy sooner. However, buyers should also remember to budget for closing costs, inspections, moving expenses, insurance, and other costs connected to purchasing a home.

First Time Home Buyer Loan Calculator

A first time home buyer loan calculator can help estimate the full cost of a mortgage. This may include the loan amount, interest rate, term length, down payment, taxes, insurance, and mortgage insurance. While a calculator cannot replace a lender’s official estimate, it is a useful starting point for understanding what different loan scenarios may look like.

Using a calculator can also help buyers compare different home prices. For example, a buyer may discover that a slightly lower home price creates a much more comfortable monthly payment. This can help prevent buyers from stretching their budget too far.

First Time Home Buyer Mortgage

Choosing a first time home buyer mortgage is one of the biggest decisions in the home buying process. Your mortgage affects your monthly payment, long-term interest costs, and overall affordability. Buyers should compare loan programs, down payment requirements, mortgage insurance, and lender fees before making a decision.

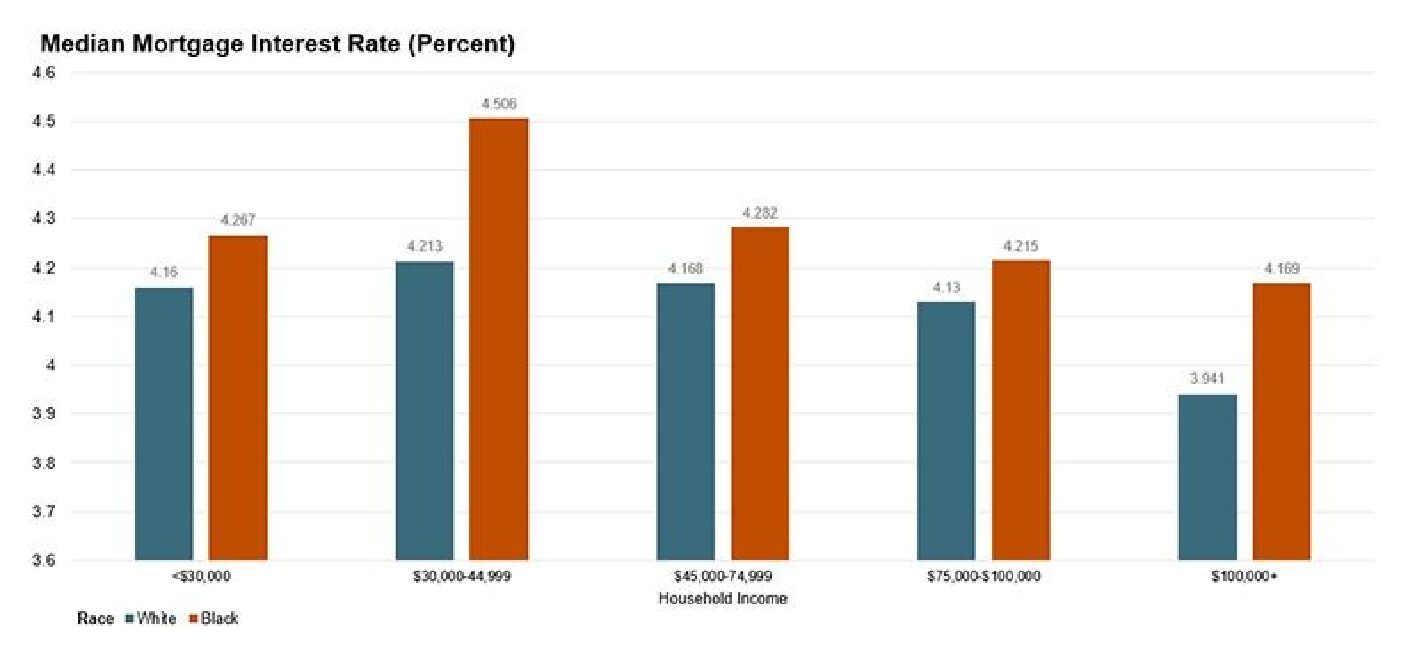

It is also important to compare first time home buyer mortgage rates. Mortgage rates can change over time and may vary based on credit score, loan type, down payment, and market conditions. Even a small difference in your first time home buyer interest rate can make a noticeable difference in your monthly payment and total cost over the life of the loan.

First Time Home Buyer Pre Approval

After estimating your budget, the next step is often first time home buyer pre approval. Pre-approval is when a lender reviews your financial information and estimates how much you may be able to borrow. The mortgage pre approval first time home buyer process usually includes reviewing income, credit, debts, employment, and savings.

Many buyers search for pre approval for home loan first time buyer because they want to know what documents they need. Lenders may ask for pay stubs, W-2s, tax returns, bank statements, identification, and permission to check credit. Getting these documents ready early can make the process easier.

A pre approved home loan first time buyer is often more prepared to make an offer because sellers may view pre-approved buyers as more serious. Pre-approval is not the same as final loan approval, but it gives buyers a stronger starting point.

Some buyers may choose to prequalify for home loan first time buyer options before getting fully pre-approved. Prequalification is usually a basic estimate, while pre-approval is more detailed. Both can be useful, but pre-approval is usually stronger when you are ready to shop for homes.

How to Qualify for a Home Loan First Time BuyeR

Many new buyers want to know how to qualify for a home loan first time buyer. While each loan program has different rules, lenders usually review credit score, income, employment history, debt-to-income ratio, savings, and the type of property being purchased. Buyers can improve their chances by paying down debt, saving for closing costs, avoiding major new purchases, and checking their credit before applying.

A first-time buyer should also avoid focusing only on the maximum loan amount. Just because you qualify for a certain amount does not mean that payment is the best fit for your budget. A mortgage calculator can help you compare different payment levels and choose a price range that feels realistic.

Buying your first home does not have to feel overwhelming. By using a first-time home buyer mortgage calculator, comparing loan programs, reviewing assistance options, and getting pre-approved with a trusted Utah lender, you can move through the process with more confidence. Whether you are considering FHA, USDA, conventional, zero-down, low down payment, or pre-approval options, understanding your numbers early can help you make a smarter home buying decision.