Buying a home is one of the biggest financial decisions most people will ever make. Before you begin looking at houses, it is important to get mortgage pre approval. A pre-approval helps you understand how much home you can realistically afford and shows sellers that you are a serious buyer. In Utah’s competitive housing market, having a pre-approval letter can make your offer much stronger than someone who has not started the financing process.

What Is Mortgage Pre-Approval?

A mortgage pre approval is a lender’s estimate of how much money you qualify to borrow after reviewing your financial information. Unlike a simple pre-qualification, a pre-approval requires documentation that verifies your income, employment, debts, and credit history.

Many buyers confuse pre approval vs pre qualification mortgage, but there is an important difference. A pre-qualification is based on information you provide yourself, while a pre-approval requires supporting documents and a more complete review by the lender. Because of this, sellers usually view a pre-approval as much stronger when evaluating purchase offers.

Mortgage Pre-Approval Requirements

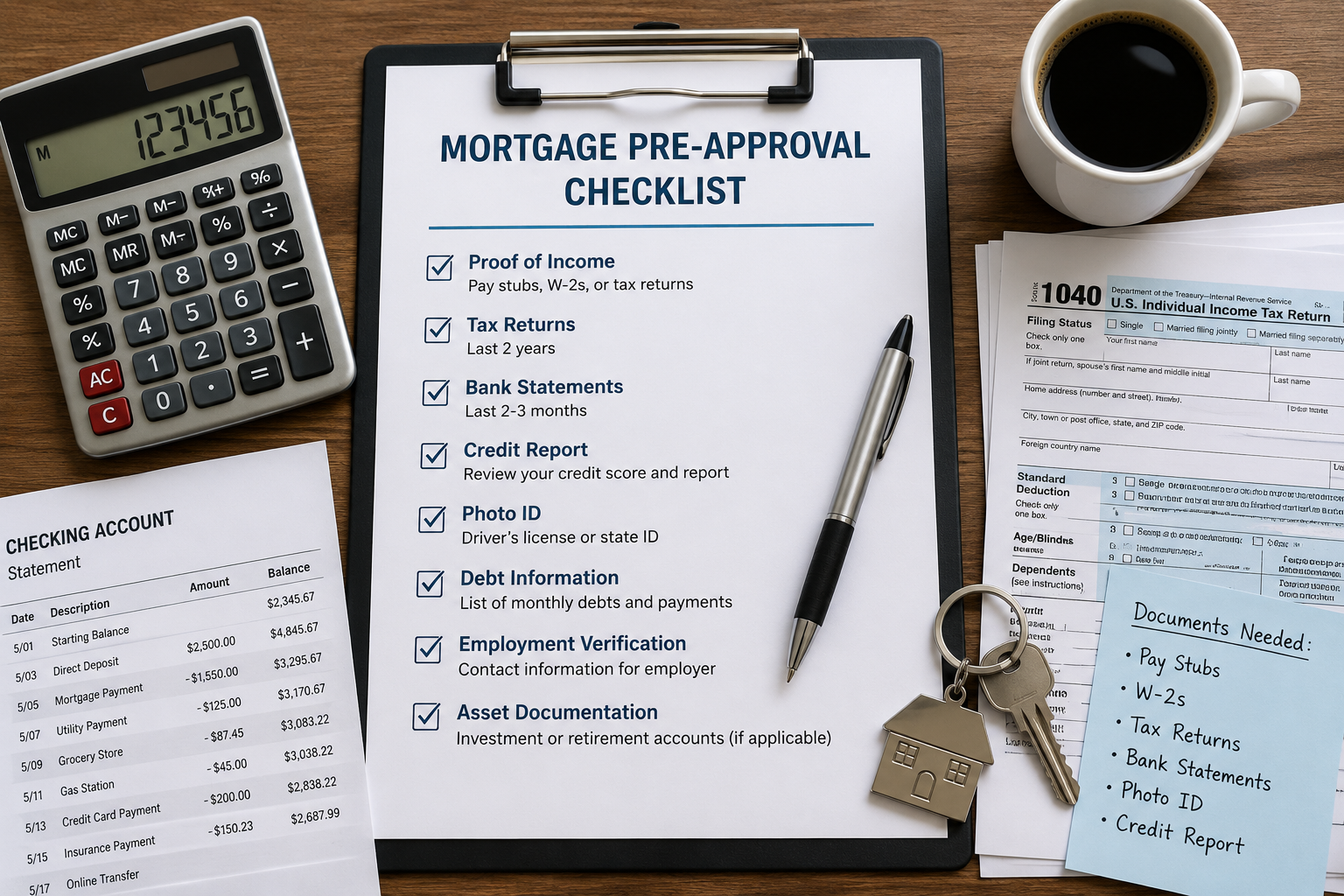

Every lender has slightly different mortgage pre approval requirements, but most ask for similar documentation.

Common documents needed for mortgage pre approval include:

· Recent pay stubs

· W-2s or tax returns

· Bank statements

· Government-issued identification

· Employment information

· Credit history

Preparing these documents ahead of time can make the approval process much faster and reduce delays.

Many buyers also create a simple mortgage pre approval checklist before applying. This helps ensure they have everything organized before speaking with a lender.

How to Get Mortgage Pre-Approval

If you’re wondering how to get mortgage pre approval, the process is usually straightforward.

First, compare several lenders to find competitive rates and good customer service. Next, complete an application and submit your financial documents. Many lenders now offer online mortgage pre approval, making the process convenient for busy homebuyers.

For a first time home buyer mortgage pre approval, lenders may also explain loan programs that require smaller down payments or provide additional assistance.

A common question is does mortgage pre approval affect credit score. Most lenders perform a hard credit inquiry, but multiple mortgage applications completed within a short shopping period are generally treated as one inquiry by credit reporting agencies.

How Long Does Mortgage Pre-Approval Last?

Many buyers ask how long does mortgage pre approval take.

Some lenders can issue a decision within one business day, while others may require several days depending on how quickly documents are submitted.

Buyers also ask how long is mortgage pre approval good for. Most pre-approvals remain valid for about 60 to 90 days. If your home search takes longer, the lender may request updated financial information before renewing your approval.

Some companies even advertise same day mortgage pre approval for qualified applicants who provide complete documentation.

Choosing the Right Mortgage Lender

Choosing the right lender is almost as important as getting pre-approved.

While interest rates are important, buyers should also compare:

· Customer service

· Closing costs

· Loan options

· Communication

· Online tools

For buyers looking for mortgage pre approval Utah, working with a lender who understands the local housing market can make the process smoother.

Additional information about home buying can be found through the Consumer Financial Protection Bureau:

https://www.consumerfinance.gov

You can also explore more Utah mortgage resources on:

Conclusion

Getting mortgage pre approval before shopping for a home is one of the smartest steps a buyer can take. It provides a realistic budget, strengthens purchase offers, and gives buyers confidence throughout the home-buying process.

By understanding the mortgage pre approval process, preparing the required documentation, and comparing lenders carefully, buyers can make better financial decisions and improve their chances of purchasing the right home.