Finding the best mortgage rates in Utah has never been more important. With median home prices exceeding $500,000 across much of the Wasatch Front, the difference between the average mortgage rate and the rate a well-prepared buyer can actually secure can mean $30,000 or more in savings over the life of the loan. This guide covers current mortgage rates in Utah, compares 30 year mortgage rates against 15 year mortgage rates, walks through every first time home buyer loan option available in the state, and shows you exactly how to qualify for the lowest rate your financial profile can achieve.

Mortgage rates today in Utah sit in the low-to-mid 6% range for a 30-year fixed product. The average mortgage interest rate nationally hovers around 6.54%, but Utah buyers who do a real mortgage rate comparison across at least three lenders routinely land offers below that figure. On a $420,000 loan, every 0.25% drop in your mortgage interest rates today saves you more than $18,000 over 30 years. Shopping lenders is not optional — it is the single highest-return action available to any Utah home buyer.

30 Year Mortgage Rates vs. 15 Year Mortgage Rates

30 year mortgage rates and 15 year mortgage rates are the two most important fixed-rate choices Utah buyers face, and picking the right term shapes your finances for decades. The current 30 year mortgage rates in Utah range from approximately 6.1% to 6.4% for a qualified borrower. These current 30 year fixed mortgage rates spread repayment across three decades, producing the lowest possible monthly payment and making homeownership more accessible — especially for the first time home buyer working within a tight monthly budget. On a $420,000 loan at 6.25%, principal and interest runs roughly $2,587 per month.

15 year fixed mortgage rates currently sit between 5.75% and 5.95% — lower in rate but significantly higher in monthly payment because the debt is retired twice as fast. That same $420,000 loan at 5.85% produces a payment of approximately $3,515 per month. The payoff is substantial: far less total interest paid and equity that builds at twice the speed. Buyers who can comfortably handle the higher payment often find that 15 year mortgage rates represent one of the best long-term wealth-building tools available. Ask your lender to run both scenarios side by side so the total home mortgage rates cost — rate, APR, and interest paid over time — makes the right choice clear.

Which Loan Term Is Right for You?

If keeping monthly payments low is your priority — particularly as a first time home buyer — the 30-year product is almost always the right starting point. If your budget has room and building equity faster matters more, the 15-year is worth a serious look. Either way, always get quotes for both on the same day from the same lender so the mortgage rate comparison is a true apples-to-apples comparison.

First Time Home Buyer Loans and Programs in Utah

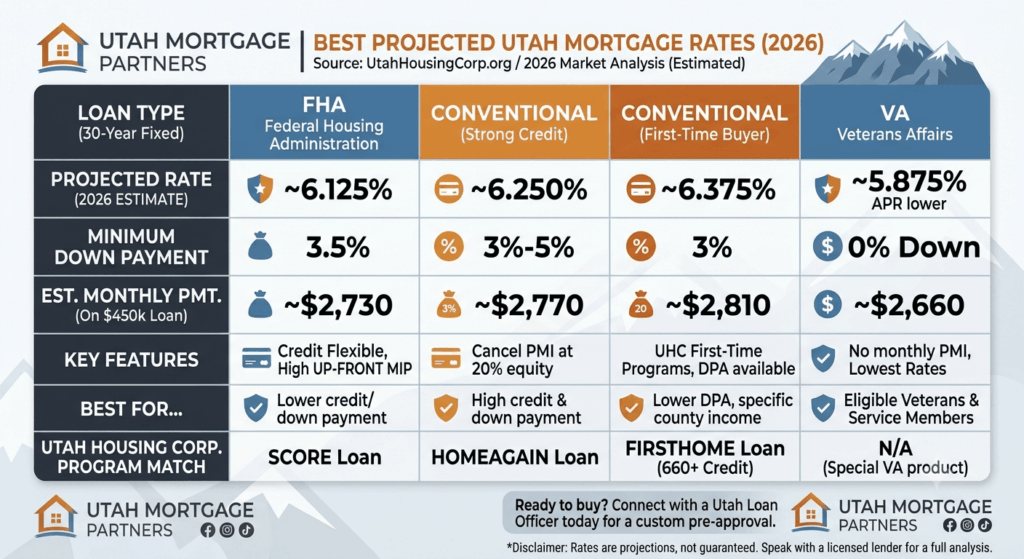

First time home buyer loans in Utah come with advantages that national lenders simply cannot match. The Utah Housing Corporation (UHC) runs several first time home buyer programs that pair below-market mortgage interest rates with down payment assistance of up to 6% of the loan amount. A qualifying first time home buyer can purchase a home with little to nothing out of pocket — a state-funded tool built specifically to help Utah residents achieve homeownership. The flagship UHC product is the FirstHome Loan, available to buyers who have not owned a primary residence in the past three years, meet county income limits, and carry at least a 660 credit score. It consistently offers the lowest rates in the UHC lineup. The HomeAgain Loan extends similar benefits to repeat buyers, while the Score Loan serves buyers with lower credit profiles. All three first time home buyer programs are 30-year fixed products. If you are asking how much house can I afford through one of these programs, a UHC-approved lender can walk you through the numbers at no cost during a pre-approval meeting. A strong first time home buyer loan from UHC, combined with down payment

Fixed Rate Mortgage Options: FHA, Conventional, and VA Loans Compared

Fixed rate mortgage products in Utah fall into three main categories, and choosing the right one directly determines which best mortgage rates are available to you. A conventional fixed rate mortgage suits buyers with a 620+ credit score and at least 3% to 5% down. It typically offers the most competitive home mortgage rates for strong borrowers and allows private mortgage insurance to be cancelled once you reach 20% equity. FHA loans open the door for buyers with scores as low as 580 and down payments of just 3.5%, making them a popular choice for buyers earlier in their credit journey. VA loans — available to eligible veterans and service members — consistently deliver the lowest current mortgage rates of any product type, with no down payment required and no mortgage insurance premium. If you are VA-eligible, always evaluate this product first.

A thorough mortgage rate comparison across all three loan types is essential before you apply. The headline interest rate alone does not tell the full story — mortgage insurance costs, origination fees, and APR all affect the true cost of each option. Ask every lender you speak with to show you a side-by-side comparison of every product you qualify for, not just the one they default to recommending. Two loans with identical mortgage interest rates today can have very different APRs if one lender is charging higher fees.

How to Qualify for the Best Mortgage Rates in Utah

Best mortgage rates go to the best-prepared borrowers. The average mortgage rate you see advertised is priced for an ideal borrower profile — 740+ credit score, 20% down, low debt load. If your profile differs, your rate will too. Here is how to close that gap.

Know your credit score. Pull your report from all three bureaus at least 60 days before applying. Dispute any errors and pay down revolving balances below 30% utilization. Every 20-point improvement in your score can lower your mortgage interest rates today by 0.125% to 0.25%.

Calculate what you can afford. Answer how much house can I afford honestly using your gross income and current monthly debts before any lender conversation. Most programs want total monthly debt — including the new mortgage — under 43% of gross income.

Compare at least three lenders. Home mortgage rates can vary by 0.25% to 0.50% for the same borrower on the same day. A real mortgage rate comparison looks at rate, APR, points, and closing costs together — not just the headline number.

Lock your rate when the time is right. Mortgage rates today move daily. Once you find an offer that works within your budget, lock it. Waiting for a small drop can backfire if the market shifts against you. Your lender can advise on the right lock window based on your closing timeline.

The Bottom Line on Mortgage Rates in Utah

Current mortgage rates in Utah are historically normal, and buyers who wait for a return to the 3% era of 2021 may wait a very long time. In Utah, when rates have fallen in the past, home prices have risen to compensate because demand here does not let up. The buyers who consistently win are the ones who control what they can: their credit score, their debt load, their down payment, and how aggressively they shop lenders.

Whether you are weighing 30 year mortgage rates against 15 year mortgage rates, exploring first time home buyer programs through the Utah Housing Corporation, comparing a fixed rate mortgage against an FHA or VA product, or doing a full mortgage rate comparison across multiple lenders — the path to the best mortgage rates is always the same: prepare your finances, compare real offers, and act when you find the right one. The average mortgage interest rate is what unprepared buyers settle for. With the right approach, Utah buyers can do significantly better.