Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

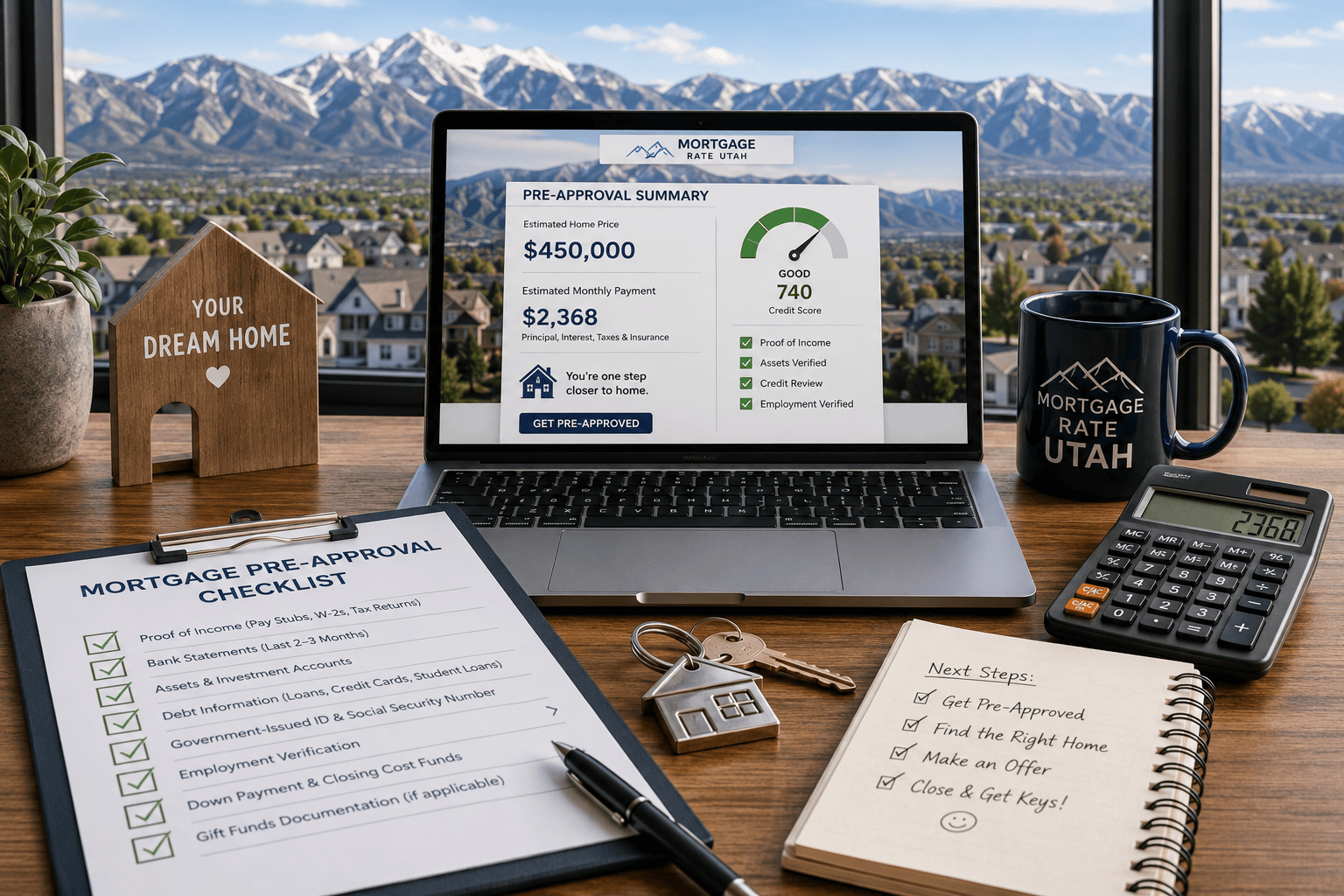

Getting ready to buy a home is exciting, but it can also feel overwhelming if you are unsure what lenders need. This guide gives Utah buyers a clear mortgage pre approval checklist to help you get organized and avoid delays. It also explains what comes next in the process. If you’ve been searching how to get pre approved for a mortgage, this guide covers the documents you’ll need, how credit and income affect approval, available loan options, and what to expect before receiving a pre-approval letter. A strong pre-approval helps you shop with confidence. It also shows sellers that you’re a qualified buyer. Before you start touring homes, review how much house can I afford, estimate your monthly payment, and make sure your credit, income, and finances are ready for the mortgage approval process.

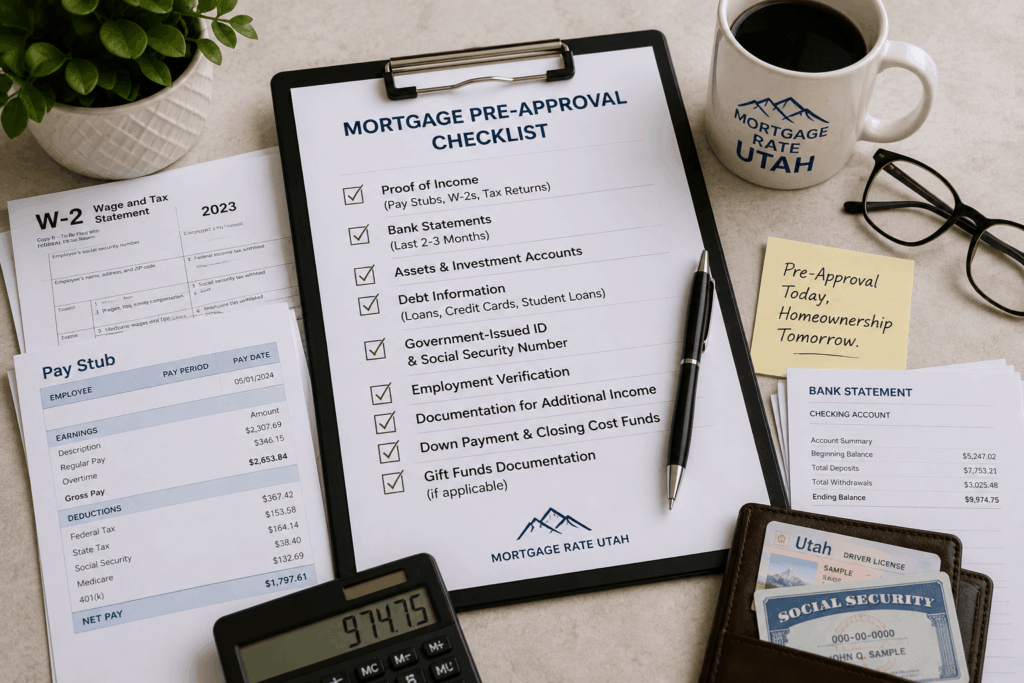

The first step in pre-approval is proving that you can repay the loan. Lenders usually ask for a government-issued ID, Social Security number, recent pay stubs, W-2s, tax returns, bank statements, and documentation for any additional income. Self-employed buyers may need profit and loss statements or extra tax documents. Having these items ready before applying can make the process faster and cleaner.

Your lender will also review savings, checking accounts, retirement funds, and any money you plan to use for your down payment or closing costs. A complete mortgage pre approval checklist should include proof of income, proof of assets, employment history, debt information, and identification.

One of the most common questions buyers ask is what credit score do I need to buy a house. The answer depends on the loan program, down payment, debt-to-income ratio, and lender guidelines. A higher score may help you qualify for better pricing. However, a lower score does not always mean you cannot buy. Some buyers can buy a home with bad credit if they have stable income, enough savings, and the right loan structure.

Before applying, check your credit report for errors, late payments, high credit card balances, and outdated accounts. Correcting mistakes early may improve your approval chances. Avoid opening new credit lines, financing furniture, or making large purchases while preparing for a mortgage. Even small increases in monthly debt can affect your approval amount.

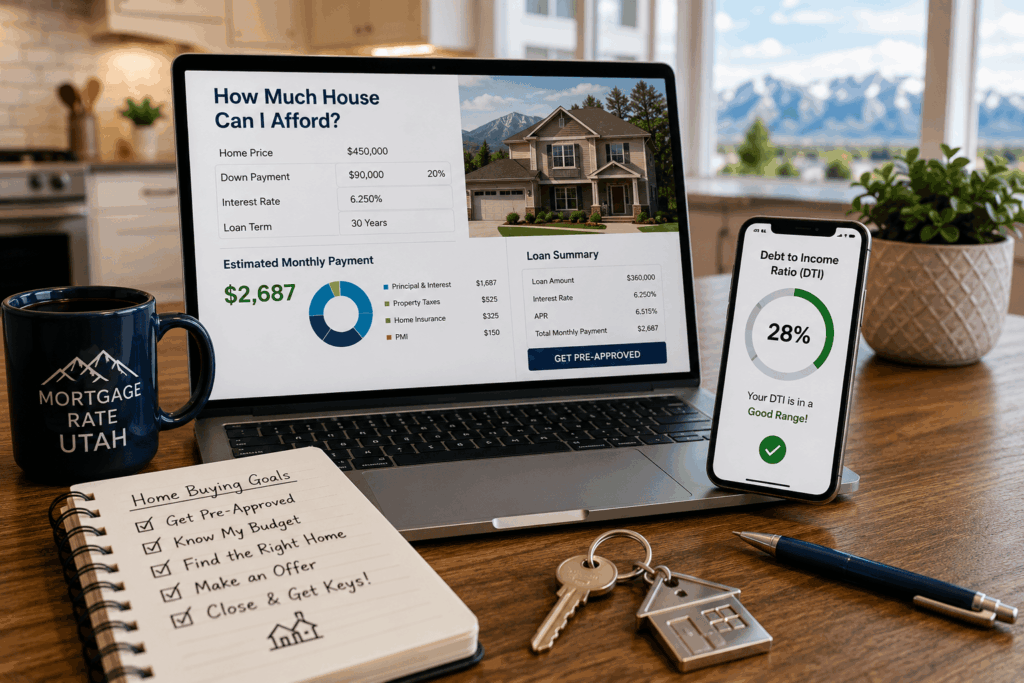

Before you fall in love with a home, you need to understand the payment. A mortgage calculator Utah page can help estimate principal, interest, taxes, insurance, and potential mortgage insurance. This is important because the sales price alone does not tell the full story. Property taxes, homeowners insurance, HOA dues, and loan terms all change the final monthly payment.

A debt to income ratio calculator is also useful because lenders compare your monthly debt payments to your gross monthly income. Your car payments, credit cards, student loans, and other debts all matter. If your debt-to-income ratio is too high, your lender may suggest paying down balances, increasing the down payment, or choosing a different loan program.

Utah buyers should ask about first time home buyer programs, grants, and down payment assistance Utah options before choosing a loan. These programs may help cover upfront costs, especially for buyers with steady income but limited savings. Because program rules can change, confirm your eligibility with a mortgage professional before making plans around assistance funds.

Many buyers compare fha loan requirements with conventional financing. FHA loans may be a good option for buyers with lower credit scores or smaller down payments. Conventional loans often work well for borrowers with stronger credit or larger savings. A conventional loan vs fha comparison should consider the down payment, mortgage insurance, interest rate, monthly payment, and long-term cost.

Veterans, active-duty service members, and some surviving spouses should review va loan eligibility because VA loans may allow qualified borrowers to buy with no down payment. Buyers searching outside major metro areas should also review the usda home loan map to see if a property qualifies. USDA loans can be an excellent option for eligible buyers who meet the income and location requirements.

Another question that comes up early is how much are closing costs. Closing costs usually include lender fees, appraisal fees, title charges, recording fees, prepaid taxes, prepaid insurance, and escrow setup. Your exact number depends on the purchase price, loan type, location, and whether the seller agrees to contribute toward buyer costs.

Ask your lender for a Loan Estimate so you can see the projected cash needed to close. This is different from your down payment. Buyers sometimes have enough saved for the down payment but forget that closing costs are separate. Knowing the full cash-to-close number early can prevent last-minute stress.

Once you are pre-approved, the mortgage process step by step moves from home shopping to writing an offer and getting under contract. Next, you’ll schedule inspections, complete the appraisal, submit final conditions, receive final approval, and close on your home. Your lender, real estate agent, title company, and insurance provider work together to keep your transaction moving.

Understanding the mortgage closing timeline helps you know what to expect. Some loans close faster than others. Delays can happen if documents are missing, an appraisal takes longer than planned, or underwriting requests additional information. Responding quickly to your lender helps keep your closing on schedule.

Buyers should also understand home appraisal vs home inspection. The appraisal estimates the home’s value for the lender. The inspection evaluates the home’s condition for the buyer. Both play an important role, but they serve very different purposes.

Many first-time buyers need escrow account explained in plain language. An escrow account is used by the lender to collect money for property taxes and homeowners insurance as part of your monthly mortgage payment. When those bills are due, the lender pays them from the escrow account. This can make budgeting easier because you are spreading large annual expenses across monthly payments.

Your payment may include principal, interest, taxes, insurance, mortgage insurance, and HOA dues if applicable. When comparing homes, do not only compare list prices. Compare the total estimated monthly payment so you understand the real cost of ownership.

When reviewing loan options, ask your lender to explain fixed vs adjustable mortgage choices. A fixed-rate mortgage keeps the same interest rate for the life of the loan, which gives payment stability. An adjustable rate mortgage explained simply means the loan may start with a lower introductory rate, but the rate can change later based on the loan terms and market conditions.

Some buyers watch the mortgage rate forecast before locking a rate, but rates can move quickly and are never guaranteed. Your best option is to talk through your budget, timeline, and risk tolerance with a lender who can explain the pros and cons of each structure.

Pre-approval is focused on buying, but it is also smart to understand your future options. If rates drop or your financial goals change, refinance mortgage rates may become important. A refinance can potentially lower your payment, shorten your loan term, or change your loan type.

Some homeowners later consider a cash out refinance to access equity for home improvements, debt consolidation, or other expenses. Another option is a home equity line of credit. A home equity line of credit, also called a heloc, lets homeowners borrow against available equity as needed. Before choosing one, compare heloc rates, fees, repayment terms, and whether a refinance would be better.

Choosing the best mortgage lender Utah is not only about the lowest advertised rate. You also want communication, local knowledge, clear explanations, and someone who can help match your situation with the right program. A good lender will help you understand documents, payments, timelines, closing costs, and the loan options that fit your goals.

Mortgage Rate Utah is built around helping Utah buyers compare options and move through the process with confidence. Whether you are buying your first home, relocating, using assistance programs, or trying to strengthen your approval, the right guidance can make the experience much easier.

Getting pre-approved before shopping for homes gives you a clearer budget, a stronger offer, and fewer surprises. Start by organizing your documents, checking your credit, estimating your payment, and asking questions early. The more prepared you are, the easier it is for your lender to review your file and help you move toward closing.

If you are ready to start, use this mortgage pre approval checklist as your guide and connect with Mortgage Rate Utah to review your options. A strong pre-approval can help you shop smarter, make better decisions, and move one step closer to homeownership.