If you’ve been watching interest rates today and wondering whether now is a smart time to refinance your Utah home, you’re not alone. Thousands of homeowners across the state are comparing refinance rates, weighing cash out refinance options, and trying to decide if a new mortgage loan makes financial sense. This guide walks you through everything you need to know about refinance mortgage rates in Utah — from how current mortgage rates are shaped, to the differences between a HELOC, a home equity loan, and a full refinance, to how VA loan rates, FHA loans, and USDA loans factor in.

Current Mortgage Rates in Utah: What to Expect in 2026

Understanding refinance mortgage rates starts with the broader rate environment. As of mid-2026, mortgage rates are hovering in the low-to-mid 6% range for most conventional loan products. If you locked in a rate above 7% in 2022 or 2023, you may already have a strong case for refinancing.

When shopping for mortgage rates today, remember that advertised rates are written for the strongest possible applicant. Your actual mortgage interest rates will depend on your credit score, loan-to-value ratio, debt-to-income ratio, and the specific mortgage lender you work with. Two borrowers can receive quotes half a percentage point apart on the same day from different mortgage lenders — that difference can mean thousands of dollars over the loan term.

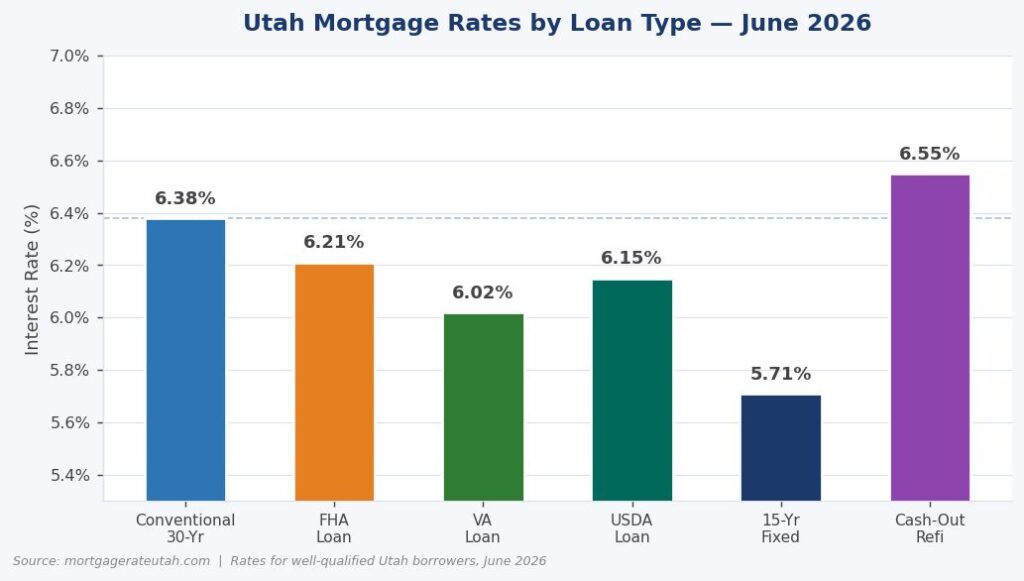

The most commonly watched benchmark is 30 year mortgage rates, which currently run between 6.2% and 6.5% for well-qualified Utah borrowers. Before calling a single mortgage lender, use a mortgage payment calculator or home loan calculator to run the numbers on your current balance. Plug in different rate scenarios and use an amortization calculator to see how much total interest you’d save over the remaining life of your loan.

Cash Out Refinance: Access Your Home Equity While Lowering Your Rate

One of the most powerful tools available to Utah homeowners is the cash out refinance. Rather than simply replacing your existing mortgage loan with a new one at a lower rate, a cash out refinance lets you borrow against the equity you’ve built — receiving the difference as cash at closing.

This works well when you need to consolidate high-interest debt, fund a renovation, or cover a major expense. Utah home values have risen significantly over the past five years, meaning many homeowners are sitting on substantial equity. To qualify, most mortgage lenders require at least 20% equity remaining in the property after the cash is withdrawn. Your mortgage lender will review your income, credit profile, and current debt load before approving the transaction.

The interest you pay on a cash out refinance is typically much lower than personal loan or credit card rates, making it a cost-effective borrowing strategy — provided you’re disciplined about what you use the funds for.

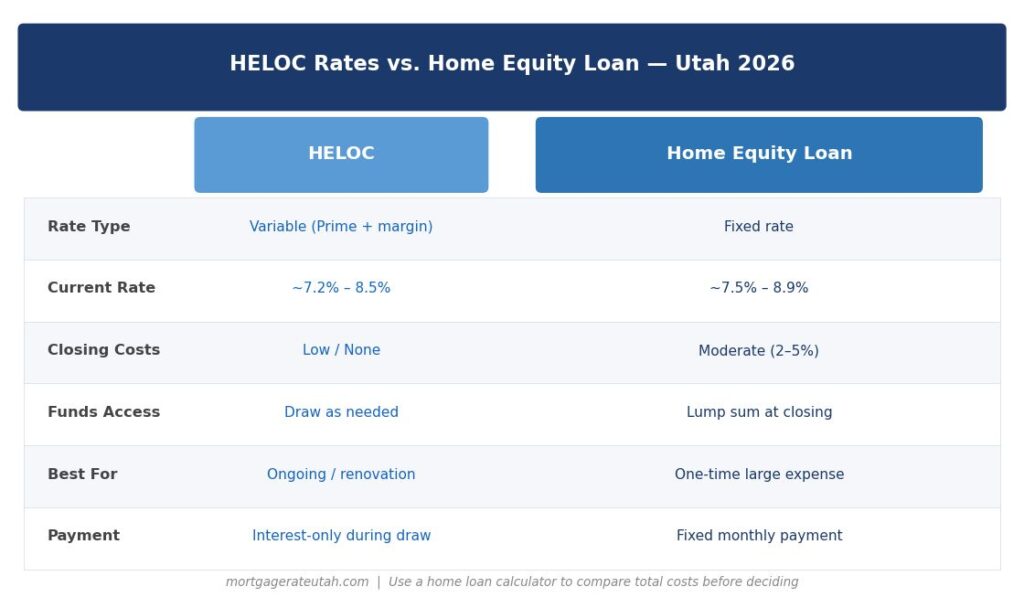

HELOC Rates vs. Home Equity Loan: Which Option Makes More Sense?

If you don’t want to restart your mortgage clock or pay full refinance closing costs, a home equity loan or a HELOC (Home Equity Line of Credit) may be a better fit. Both products let you borrow against your home’s equity without replacing your existing first mortgage.

A home equity loan delivers a lump sum at a fixed rate — similar to a second mortgage. HELOC rates, by contrast, are typically variable, tracking the prime rate and fluctuating month to month. Current HELOC rates generally run slightly above first-mortgage rates, but you avoid the closing cost of a full refinance, which can range from 2%–5% of the loan amount.

The right choice depends on how much you need to borrow, how long you plan to stay in the home, and whether you prefer a fixed or variable payment. Use a home loan calculator to compare monthly costs for both options side by side — and factor in the break-even timeline before committing.

Best Mortgage Rates by Loan Type: VA, FHA, USDA, and Conventional

Your loan type has a major impact on the refinance mortgage rates you’ll qualify for. Here’s how each option stacks up:

VA loan / VA home loan: Eligible veterans and active-duty service members can refinance through the VA Interest Rate Reduction Refinance Loan (IRRRL) program. VA loan rates are consistently among the lowest available — often 0.25%–0.5% below conventional pricing — because the federal government backs the loan and reduces risk for the lender. If your current mortgage is a VA home loan, the IRRRL is the fastest, lowest-cost refinance path available.

FHA loans: Homeowners with existing FHA loans can use the FHA Streamline Refinance, requiring minimal documentation and no new appraisal. FHA loans refinance rates are competitive and accessible to borrowers with credit scores as low as 580. The main trade-off is that FHA loans require ongoing mortgage insurance regardless of your equity level.

USDA loans: Common in rural Utah communities, USDA loans come with a Streamlined Assist Refinance option that requires no new credit check or appraisal — just proof that you’ve made on-time payments for the past 12 months. If you originally financed in a USDA-eligible county, check this program before exploring other options.

Conventional: For borrowers with strong credit and at least 20% equity, conventional refinances typically offer the best mortgage rates available. If your credit score has improved since you first bought, or if your home has appreciated significantly, a conventional refi can also eliminate PMI that’s been adding to your monthly payment.

First Time Home Buyer Programs and Refinancing Later

If you originally purchased using first time home buyer programs — such as those offered by the Utah Housing Corporation — check the terms before refinancing. Some down payment assistance loans require you to remain in the home for a set period or repay a portion of the grant if you refinance within the first few years.

Once those restrictions expire, refinancing is usually straightforward. Homeowners who originally used first time home buyer programs and have since reached 20% equity can often refinance into a conventional mortgage, drop PMI, and lower their payment simultaneously. It’s worth running the numbers with a mortgage payment calculator to see if the timing makes sense for your situation.

How to Use a Mortgage Payment Calculator to Evaluate Your Refinance

Before reaching out to a single mortgage lender, do your homework with the right tools. A mortgage payment calculator lets you estimate your new monthly payment at different interest rates — enter your current loan balance, the new rate, and the remaining term and it will show you the monthly savings instantly.

An amortization calculator goes a step further, showing you the full interest cost over the life of the loan at both the old and new rates. The difference can be surprisingly large: even shaving 0.5% off a $400,000 loan saves over $45,000 in total interest on a 30-year term. A home loan calculator that factors in closing costs will also tell you your break-even point — the month when your accumulated savings exceed what you paid to refinance.

Once you’ve modeled your scenarios, request written loan estimates from at least three mortgage lenders. Comparing best mortgage rates across multiple lenders — including a local credit union, a regional bank, and an online lender — gives you real leverage. Utah has one of the strongest credit union markets in the country, and credit unions here regularly beat national banks on mortgage interest rates for qualified borrowers. Don’t accept the first quote you receive.

The Bottom Line on Utah Refinance Mortgage Rates

Whether you’re chasing a lower payment on your existing mortgage loan, tapping equity through a cash out refinance, weighing HELOC rates against a home equity loan, or using the IRRRL to lower your VA loan rates — the math matters more than the market headlines. Run your numbers with a mortgage payment calculator, compare at least three mortgage lenders, and keep an eye on current mortgage rates in the weeks before you lock. Utah homeowners who take a disciplined, comparison-focused approach to refinancing consistently come out ahead.