Mortgage rates are one of the most important factors to understand before buying, refinancing, or using home equity. A small difference in your interest rate can change your monthly payment, your total loan cost, and the type of home loans you may be able to afford. That is why

borrowers should not only look at mortgage rates today, but also compare loan terms, lender fees, closing costs, and long-term financial goals. Before you apply for a mortgage, it helps to understand how lenders review your credit, income, debt, down payment, and property type. A smart mortgage plan starts with research. Many borrowers search for the best mortgage companies, but the best company for one buyer may not be the best choice for another. Your situation matters. A first-time buyer may need help with mortgage pre approval, while a homeowner may be more interested in mortgage refinancing, a home equity loan, or a cash out refinance. The goal is to compare options carefully so the loan fits your budget instead of forcing your budget to fit the loan.

Current Mortgage Rates

Current mortgage rates change frequently, and the rate you see advertised online may not be the exact rate you receive. Your personal rate can depend on your credit score, loan amount, down payment, property location, loan type, and whether you are buying a home or refinancing. When reviewing current mortgage rates, compare both the interest rate and the annual percentage rate because the APR can include certain loan costs. The Consumer Financial Protection Bureau offers a mortgage interest rate tool that helps borrowers compare how credit score, loan type, price, and down payment may affect rates.

Consumer Financial Protection Bureau mortgage rate tool

Mortgage rates today should be treated as a starting point, not a final answer. A mortgage quote from one lender may include different fees, points, or assumptions than a quote from another lender. For that reason, borrowers should request written estimates and compare the same loan type across multiple lenders. Freddie Mac also publishes mortgage rate data through its Primary Mortgage Market Survey, which is based on mortgage rate information collected from loan applications submitted through lenders across the country.

Mortgage Calculator

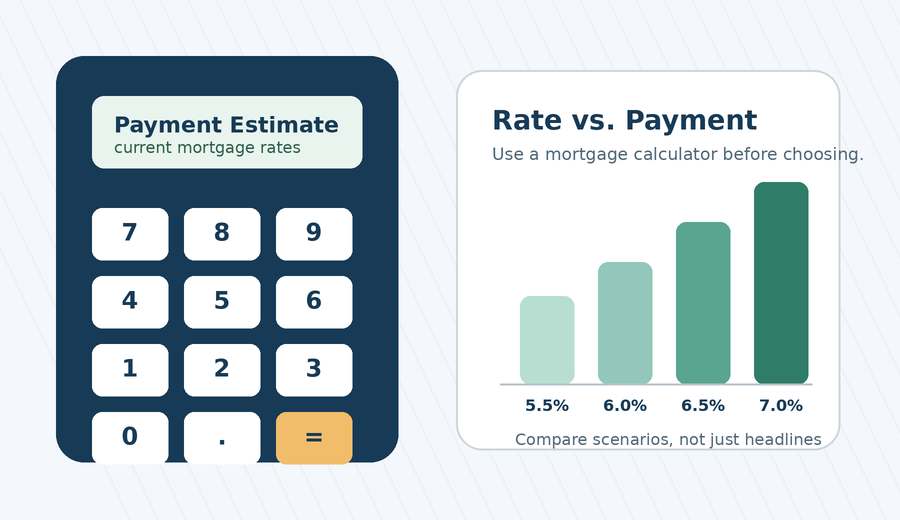

A mortgage calculator is one of the most useful tools for understanding affordability. A basic calculator estimates principal and interest, while a more detailed home loan calculator may include property taxes, homeowners insurance, mortgage insurance, and HOA fees. Using a mortgage calculator before contacting a mortgage lender can help you set a realistic payment range and avoid focusing only on the maximum loan amount.

A home loan calculator can also help you compare different scenarios. For example, you can test how your monthly payment changes with a larger down payment, a lower purchase price, or a different interest rate. A va loan calculator may be useful for eligible military borrowers who

are comparing VA financing, while a reverse mortgage calculator may help older homeowners explore whether a reverse mortgage is worth discussing with a qualified professional. These tools do not replace lender approval, but they can help you ask better questions before you

apply for a mortgage.

Mortgage Lender

Choosing a mortgage lender should involve more than picking the first result online. Some buyers search for a mortgage broker near me because they want local guidance, while others compare banks, credit unions, online lenders, and the best mortgage companies. A broker may

help compare different loan options, but you should still review the details of every mortgage quote, including the rate, APR, lender fees, discount points, and estimated closing costs. A strong mortgage lender should explain the difference between prequalification and mortgage

pre approval. Mortgage pre approval usually requires more documentation and may give sellers more confidence when you make an offer. During this stage, the lender may review income, employment, credit history, assets, and debts. Before you apply for a mortgage, avoid opening new credit accounts, making large unexplained deposits, or taking on major new debt because those changes may affect your approval.

Mortgage Refinancing

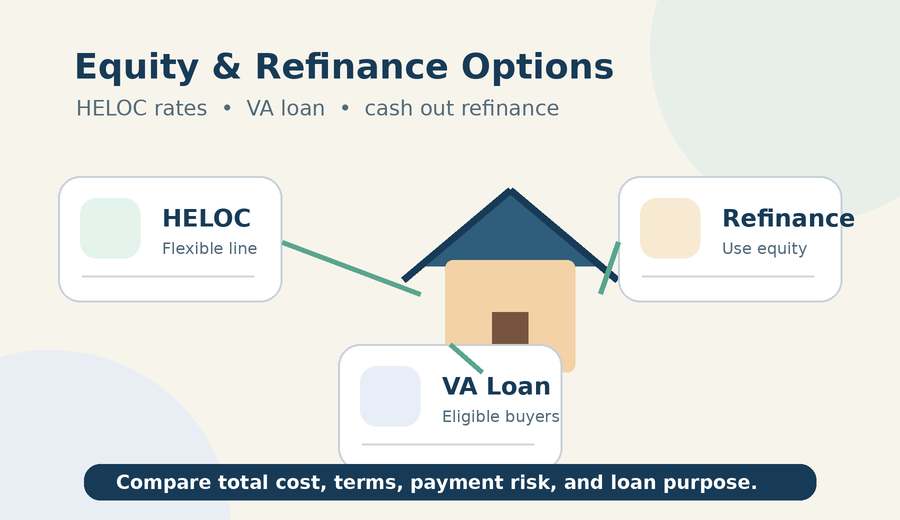

Mortgage refinancing may be helpful when a new loan improves your overall financial situation. A refinance home loan can sometimes lower your monthly payment, shorten your loan term, switch an adjustable-rate loan to a fixed-rate loan, or help remove a borrower from the mortgage. However, refinancing usually comes with closing costs, so borrowers should calculate the break-even point before moving forward. A cash out refinance works differently because it replaces your current mortgage with a larger loan and gives you part of your home equity as cash. This may be used for home improvements, debt consolidation, or major expenses, but it also increases the amount secured by your home. If current mortgage rates are higher than the rate on your existing loan, it may be worth comparing a cash out refinance with a home equity loan or home equity line of credit before making a decision.

Home Equity Loan and HELOC Rates

A home equity loan allows homeowners to borrow against their equity, usually with a lump sum and a fixed repayment schedule. Home equity loan rates may be easier to budget for because the payment is often predictable. This option can work well for borrowers who know exactly how much money they need for a project, repair, or other planned expense. A home equity line of credit, often called a heloc, is usually more flexible. A heloc loan may allow homeowners to borrow as needed during a draw period and repay over time. When comparing heloc rates, look beyond the starting rate. Review whether the rate is fixed or

variable, how long the introductory period lasts, what fees apply, and how repayment works after the draw period ends. A HELOC may be useful for ongoing expenses, while a home equity loan may be better for one-time costs

VA Home Loan Options

A va home loan can be a valuable option for eligible Veterans, service members, and qualifying surviving spouses. A va loan is provided through private lenders but backed by the Department of Veterans Affairs. Borrowers still need to meet credit, income, and occupancy requirements, and the VA explains that eligible borrowers may need a Certificate of Eligibility to show a lender they qualify.

A va loan calculator can help estimate monthly payments, but borrowers should also ask about the VA funding fee, closing costs, property requirements, and how the offer compares with conventional financing. For some borrowers, a VA loan may provide strong benefits, but it

should still be compared with other home loans to make sure the total cost and structure make sense. The best mortgage strategy is to move step by step. First, check mortgage rates and mortgage rates today to understand the market. Next, use a mortgage calculator or home loan calculator to estimate payments. Then, request a mortgage quote from more than one mortgage lender. After that, compare loan terms, fees, closing costs, and customer service. Whether you are buying, researching mortgage refinancing, comparing heloc rates, considering a home equity line of credit, or preparing to apply for a mortgage, the right loan should support your long-term financial goals.