Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Saving for a down payment is one of the biggest obstacles standing between many Utah families and homeownership. In fact, it’s often not the monthly mortgage payment that keeps people from buying a home—it’s coming up with enough cash upfront.

The good news is that many buyers don’t realize they may qualify for programs that can significantly reduce those initial costs. Whether you’re researching first-time home buyer programs, comparing first-time home buyer loans, or wondering if buying a home is even realistic this year, understanding your options can make the process much less intimidating.

Utah offers several loan and assistance programs designed specifically to help first-time buyers purchase a home sooner. Some provide lower down payment requirements, while others can help cover part of your down payment or closing costs. Combined with guidance from an experienced mortgage professional, these resources can help you move from renting to owning with more confidence.

This guide explains how Utah down payment assistance works, who may qualify, which loan programs are available, and what steps you should take before applying.

One of the most common myths about buying a home is that you need a 20% down payment. While putting more money down can reduce your monthly payment, many buyers purchase their first home with much less.

A first-time buyer mortgage is designed to make homeownership more accessible, especially for buyers who may not have years of savings. Depending on your financial situation, you may qualify for a first-time home owner’s loan that offers flexible credit requirements, lower down payment options, or access to assistance programs.

Many buyers begin by comparing the best mortgage lenders for first-time buyers. While interest rates certainly matter, an experienced lender can also help you identify loan programs and assistance opportunities you may not have discovered on your own.

Utah buyers have several potential resources available, including assistance offered through participating lenders and statewide housing programs. Depending on the program, assistance may be used toward:

Some assistance programs are structured as forgivable loans, while others are low-interest or deferred-payment second mortgages. The exact terms depend on the program you qualify for.

For many buyers, combining one of these programs with the right mortgage can significantly reduce the amount of cash needed at closing.

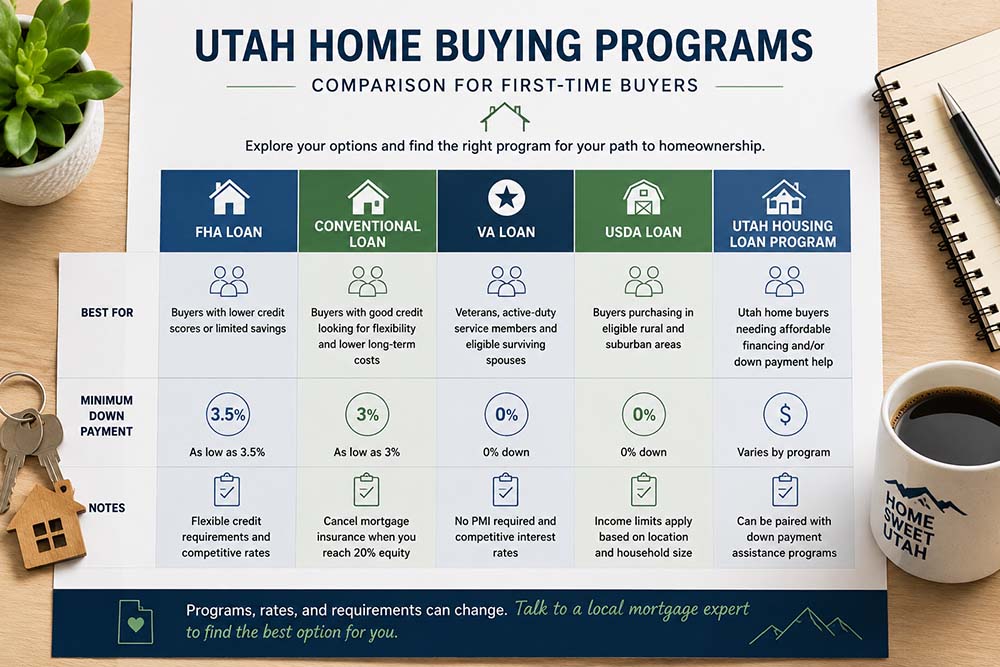

| Loan Program | Best For | Minimum Down Payment | Notes |

| FHA Loan | Buyers with moderate credit or limited savings | As low as 3.5% | Popular FHA loan first-time home buyer option with flexible qualification guidelines. |

| Conventional Loan | Buyers with stronger credit | As low as 3% | Often offers competitive long-term costs for qualified borrowers. |

| VA Loan | Eligible veterans and active-duty military | 0% | One of the most popular first-time home buyer loans with zero down available for eligible military borrowers. |

| USDA Loan | Qualified rural property buyers | 0% | Excellent option for eligible borrowers seeking a no-down-payment first-time home buyer loan in qualifying areas. |

| Utah Housing Loan Program | Qualified Utah buyers needing assistance | Varies by program | Can often be paired with down payment assistance through participating lenders. |

Every buyer’s situation is different. Credit score, income, military eligibility, property location, and long-term financial goals all influence which loan offers the greatest value. Rather than searching for the single best first-time home buyer loans, it’s usually better to compare several options with a licensed mortgage professional who understands Utah’s lending market.

One of the biggest surprises for many buyers is discovering they qualify sooner than they expected.

Most home-buying programs evaluate similar financial factors, including:

If you’re researching first-time home buyer Utah requirements, remember that every assistance program has its own guidelines. Meeting the qualifications for one program does not automatically mean you’ll qualify for every available option.

Income is another important consideration. Many buyers search for first-time home buyer Utah income limits, but these limits vary depending on the assistance program and sometimes even by county. Some programs are intended to help moderate-income households, while others have broader eligibility requirements.

If you’re unsure whether you qualify, the best first step is obtaining a mortgage pre-approval. A lender can review your financial information and determine which programs may be available before you begin shopping for homes.

Many buyers are also surprised to learn that assistance isn’t limited to one type of loan. Depending on eligibility, several first-time buyer programs can work alongside conventional, FHA, VA, or USDA financing.

Before You Apply Checklist

Before submitting an application, take a few simple steps to strengthen your position:

Completing these steps ahead of time can make the application process faster and reduce unexpected delays once you’ve found the right home.

For many buyers, the most valuable resource available isn’t necessarily a lower interest rate—it’s reducing the amount of money needed at closing.

Utah offers several first-time home buyer programs designed to make homeownership more attainable. These programs may provide education, affordable financing, or assistance with down payment and closing costs through participating lenders.

Many buyers specifically search for first-time home buyer Utah grants or Utah first-time home buyer grants because they’re hoping to receive money that doesn’t have to be repaid. While true grant opportunities do occasionally exist, many assistance programs today are structured differently. Some use deferred-payment second mortgages, while others offer repayment only if certain conditions occur, such as selling or refinancing the home before a specified period.

Understanding how each option works is important before deciding which program best fits your financial goals.

Continuing from the previous section…

A good lender will explain how each option works, including whether assistance must be repaid, how repayment is triggered, and whether you can combine assistance with other loan products.

If you’re comparing first-time home buyer programs in Utah, don’t focus only on the amount of assistance offered. Consider the entire financing package, including interest rate, monthly payment, loan term, mortgage insurance, and long-term affordability.

Many borrowers also search for a Utah first-time home buyer assistance program because they want help overcoming the largest hurdle—saving enough cash upfront. These programs are often administered through participating lenders in partnership with state housing initiatives, making it easier for qualified buyers to access affordable financing.

Imagine Sarah and Alex, a young couple renting an apartment in Salt Lake County. They’ve been saving for years but only have about $12,000 available for a home purchase. They assumed they needed far more before they could buy.

After meeting with a mortgage professional, they learned they qualified for first-time home buyer assistance in Utah through a participating lender. By pairing an FHA loan with an eligible assistance program, they were able to reduce the amount of cash needed at closing while still purchasing a home that fit their budget.

Instead of waiting several more years to save a larger down payment, they were able to become homeowners much sooner—all because they explored the programs available before assuming they couldn’t qualify.

Every buyer’s situation is different, but this example highlights why it’s worth discussing available assistance before delaying your homeownership goals.

The application process is often more straightforward than many first-time buyers expect. Working with a knowledgeable lender early can help you understand your options and avoid unnecessary delays.

A typical process looks like this:

Before touring homes, obtain a mortgage pre-approval. This gives you a realistic price range and helps sellers take your offer more seriously.

Suggested Internal Link:

Your lender will determine whether you qualify for programs based on your credit, income, employment, and property type.

If you’re researching first-time home buyer Utah down payment assistance, remember that eligibility varies by program. Some are designed specifically for first-time buyers, while others may also be available to repeat buyers who meet certain requirements.

Some assistance programs require borrowers to complete a homebuyer education course. These courses help buyers understand budgeting, homeownership responsibilities, mortgage payments, insurance, and long-term financial planning.

Although it requires a little extra time, many buyers find these courses extremely helpful.

Your lender will collect documents such as:

Providing complete documentation early can help your loan move through underwriting more efficiently.

Once your loan is approved, you’ll review your closing disclosure, sign the final paperwork, and receive the keys to your new home.

For many first-time buyers, this process feels much less stressful than they expected because most of the work is completed before closing day.

If you’d like to learn more about statewide housing resources, these organizations provide valuable information:

These organizations regularly update eligibility guidelines, educational materials, and homebuyer resources.

There’s no single loan that’s right for everyone. The best financing option depends on your financial goals, credit profile, and how long you plan to stay in the home.

Some buyers prioritize the lowest monthly payment, while others want the smallest upfront investment. That’s why comparing loan options is so important.

For example:

Don’t make the mistake of assuming the lowest interest rate automatically means the best loan. Looking beyond first-time buyer mortgage rates and evaluating total loan costs often results in a smarter financial decision.

Another common mistake is waiting until you’ve found your dream home before speaking with a lender. Pre-approval not only helps establish your budget, but it also gives you time to explore available assistance programs before making an offer.

Finally, buyers frequently search online for a Utah first-time home buyer tax credit. Tax laws and available incentives can change over time, so it’s always wise to discuss potential tax benefits with a qualified tax professional rather than relying on outdated online information.

If you’re interested in learning more about FHA financing, be sure to explore our:

Suggested Internal Link:

Understanding how different loan options work together with assistance programs can help you choose financing that supports both your immediate needs and your long-term financial goals.

Not always. While many first-time home buyer programs are designed for people purchasing their first home, some assistance programs are available to repeat buyers who meet specific eligibility requirements. The definition of “first-time buyer” can also vary by program, so it’s worth speaking with a lender before assuming you don’t qualify.

The answer depends on the loan you choose. Some conventional loans allow qualified buyers to put down as little as 3%, FHA loans may require as little as 3.5%, and certain VA and USDA loans may require no down payment for eligible borrowers. If you qualify for a Utah down payment assistance program, your required cash at closing could be even lower.

Yes. Many borrowers combine assistance programs with FHA financing. An FHA loan for first-time home buyers is one of the most popular choices because of its flexible qualification requirements and lower minimum down payment.

Some programs include first-time home buyer Utah income limits, while others have broader eligibility guidelines. Income limits can vary based on household size, county, and the specific assistance program you’re applying for. Your lender can review the most current requirements and determine which options you qualify for.

Not necessarily. Many buyers search for Utah down payment grants or first-time home buyer Utah grants, expecting free money that never has to be repaid. In reality, some programs are true grants, while others are structured as second mortgages with deferred payments or favorable repayment terms. Understanding those differences before choosing a program is important.

Don’t assume you’re automatically disqualified. Loan programs have different credit requirements, and many first-time buyers qualify even if their credit isn’t perfect. Improving your credit score before applying may expand your loan options, but there are still financing solutions available for many borrowers with average credit.

For many buyers, yes. The Utah Housing loan program offers access to financing options and assistance through participating lenders. If you’re comparing different mortgage solutions, it’s worthwhile to ask whether this program fits your financial goals and eligibility.

Buying your first home is one of the biggest financial decisions you’ll ever make, but it doesn’t have to be overwhelming. The biggest mistake many buyers make is assuming they need a large down payment before they can even begin the process.

Today’s lending options are far more flexible than many people realize. Whether you’re exploring first-time home buyer loans, comparing the best first-time home buyer loans, researching first-time buyer programs, or looking for home-buying programs that reduce upfront costs, taking the time to understand your options can make a significant difference.

If you’re searching for first-time home buyer Utah programs, wondering about first-time home buyer Utah requirements, or comparing first-time buyer mortgage rates, the best first step is speaking with a knowledgeable mortgage professional who understands the Utah market. They can help you compare loan options, explain available assistance, and determine whether you qualify for programs that fit your financial situation.

Remember that many buyers who search for first-time home buyer Utah down payment assistance, Utah first-time home buyer grants, or a Utah first-time home buyer assistance program are surprised to learn they qualify sooner than expected. Even if you’ve only recently started saving, it may be worth exploring your options before deciding to postpone homeownership.

At Mortgage Rate Utah, our goal is to help first-time buyers make informed decisions with clear, honest guidance. Whether you’re ready to begin the application process or simply want to understand your financing options, we’re here to help you take the next step with confidence.