For borrowers with a 700 credit score, mortgage qualification becomes significantly more favorable compared to lower credit tiers. While a 700 score is generally considered “good,” approval still depends on more than just credit. Lenders evaluate income stability, debt obligations, employment history, and overall financial risk before determining how much mortgage you can qualify for.

Understanding how a mortgage with 700 credit score is evaluated helps borrowers prepare beyond simply checking their credit report.

What Does a 700 Credit Score Mean for Mortgage Approval?

A mortgage with 700 credit score typically qualifies borrowers for conventional loan programs with competitive interest rates. Compared to lower credit ranges, a 700 score often results in:

- More favorable interest rates

- Lower private mortgage insurance (PMI) costs

- Stronger approval likelihood

- Greater flexibility in down payment requirements

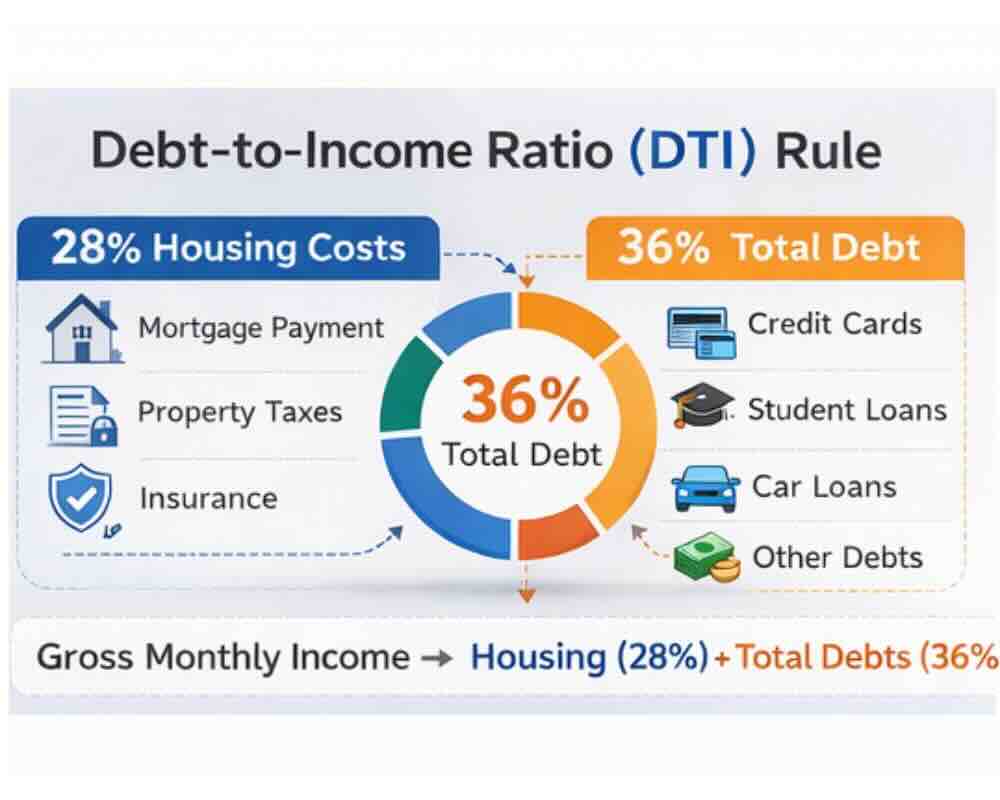

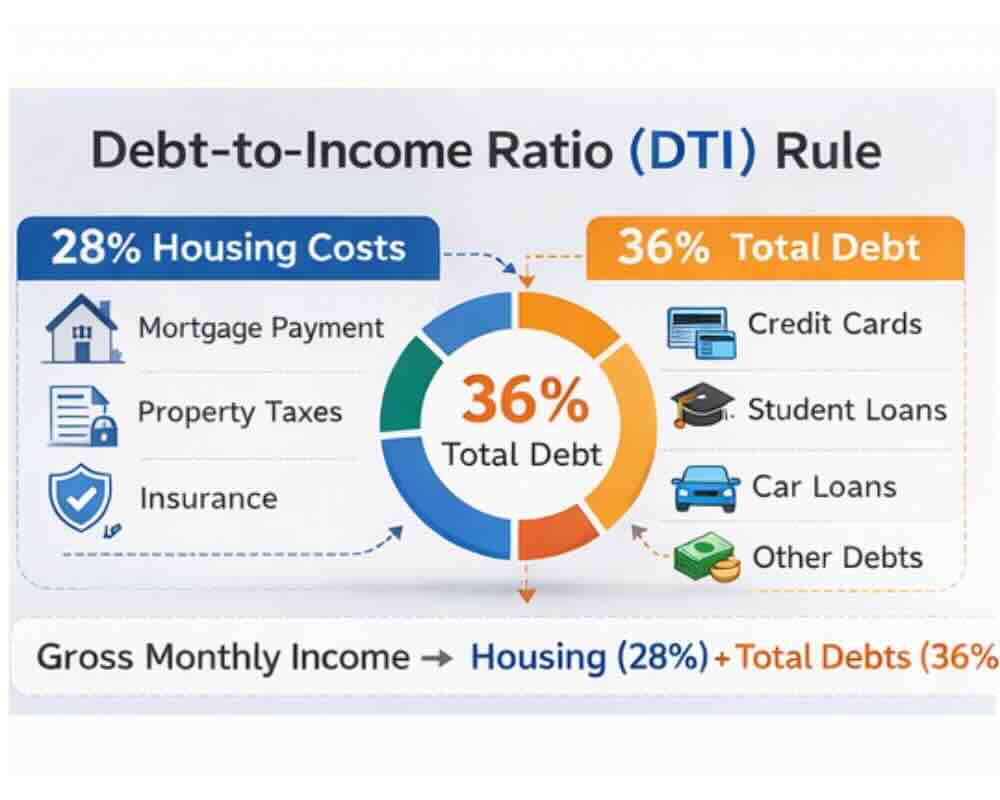

However, lenders still calculate your debt to income ratio for mortgage approval to ensure total monthly obligations remain within acceptable limits. A strong credit score improves eligibility, but excessive debt can reduce approval amounts.

This reinforces an important principle: credit score alone does not determine approval. Overall financial stability carries equal weight in the underwriting process.

Income and Debt Still Determine How Much You Can Qualify For

Even with solid credit, lenders analyze:

- Gross monthly income

- Total recurring debts

- Employment consistency

- Minimum income for mortgage approval standards

- Your overall debt-to-income ratio

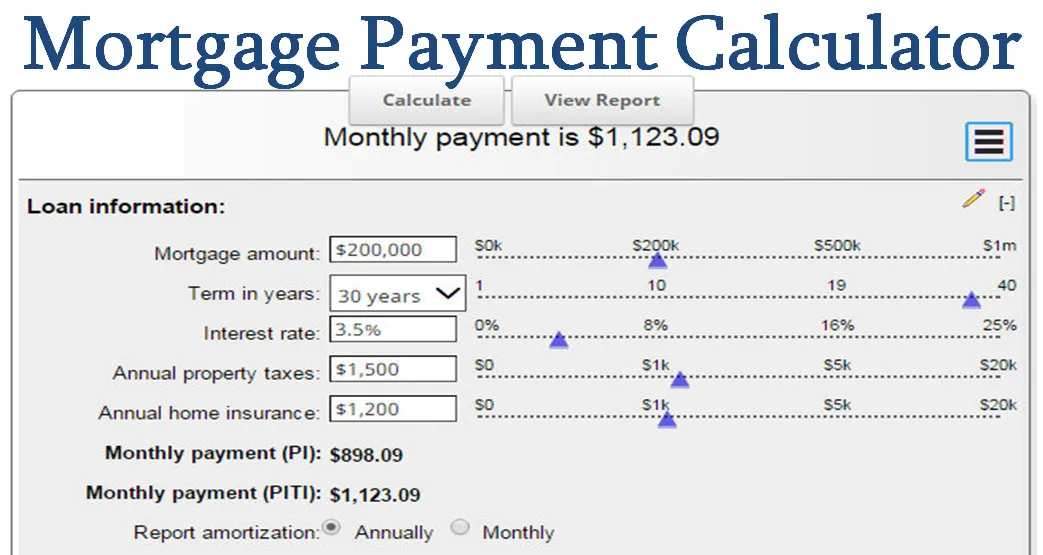

Borrowers often use tools like a mortgage calculator with down payment or a 30 year fixed mortgage calculator to estimate monthly obligations before formally applying. These tools provide a realistic payment expectation but do not replace full lender evaluation.

Ultimately, how much mortgage you can qualify for depends on the relationship between income, debt, and long-term repayment capacity.

Down Payment Strategy and Loan Structure

Down payment size also influences approval and loan terms. A larger down payment can:

- Reduce monthly payment obligations

- Lower PMI requirements

- Strengthen underwriting confidence

- Improve long-term affordability

First-time buyers may compare options using a mortgage calculator first time buyer bad credit tool to understand how interest rates shift across different credit brackets.

Even with a 700 score, optimizing down payment strategy can improve loan performance and financial flexibility.

What Else Affects Mortgage Affordability?

Beyond credit score, lenders consider:

- Length of credit history

- Recent credit activity

- Existing loan balances

- Stability of employment

- Overall financial behavior

These factors collectively determine approval risk and influence final loan structure. Understanding what affects mortgage affordability allows borrowers with a 700 credit score to strengthen weak areas before applying.

Final Thoughts

A mortgage with 700 credit score provides access to strong lending opportunities, but it represents only one component of mortgage qualification. Income consistency, debt management, down payment size, and loan selection all influence final approval outcomes.

Borrowers who evaluate their full financial profile instead of relying solely on credit score position themselves for stronger long term affordability and sustainable homeownership.