Buying a home in Utah is one of the biggest financial decisions most people will ever make, and understanding Utah mortgage rates today is an important part of that process. Mortgage rates affect monthly payments, long-term interest costs, and how much home a buyer can realistically afford. When people search for mortgage rates, mortgage rates today, or current mortgage rates, they are usually trying to answer one key question: what rate can I actually qualify for right now?

Mortgage rates are not the same for every borrower. A lender will usually look at credit score, income, debt-to-income ratio, down payment, loan amount, loan type, and current market conditions. This means two Utah buyers could apply on the same day and receive different rate offers. That is why it is important to understand the difference between general rate information and a personalized loan quote.

Current Mortgage Rates Utah: Why Rates Change

People often search for current mortgage rates Utah, mortgage interest rates, and mortgage interest rates today because rates can change often. Mortgage rates are influenced by broader economic factors such as inflation, Federal Reserve policy, bond market movement, and lender competition. While borrowers cannot control the market, they can control some of the factors that influence the rate they are offered.

For example, a higher credit score can often help a borrower qualify for a better rate. A larger down payment may also reduce lender risk and improve loan options. Borrowers should also pay attention to the annual percentage rate, or APR, because it includes both the interest rate and certain loan costs. A low interest rate may look attractive, but if it comes with high fees, it may not actually be the best deal.

For more general mortgage information, buyers can review the Consumer Financial Protection Bureau mortgage guide.

30 Year Mortgage Rates and Fixed Loan Options

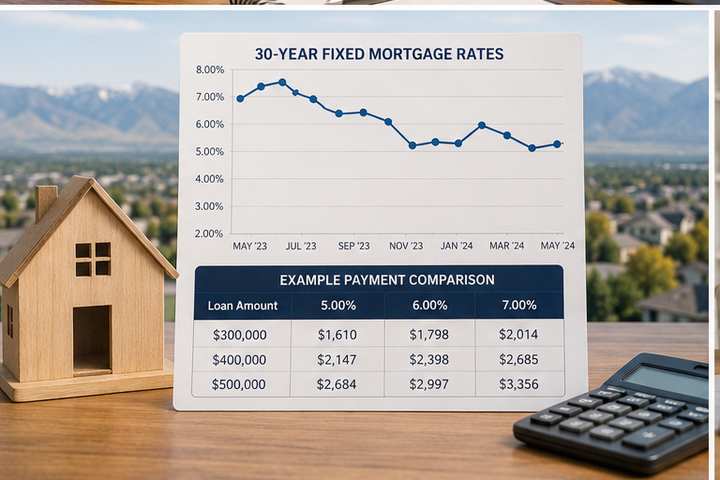

Many Utah buyers search for 30 year mortgage rates, 30 year mortgage rates today, current 30 year mortgage rates, 30 year fixed mortgage rates, and current 30 year fixed mortgage rates because the 30-year fixed mortgage is one of the most common home loan options. This type of loan spreads payments over a longer period and keeps the interest rate stable for the life of the loan. That stability can make budgeting easier for homeowners.

The main advantage of a fixed-rate mortgage is predictability. If a buyer plans to stay in the home for a long time, a fixed rate can protect them from future rate increases. However, buyers should still compare offers from multiple lenders because the rate, fees, and closing costs can vary. A slightly lower rate can save money over time, but only if the overall loan terms make sense.

Best Mortgage Utah: How to Compare Offers

Searching for best mortgage rates, best mortgage rates today, best mortgage rates Utah, or lowest mortgage rates can be helpful, but buyers should be careful. The lowest advertised rate is not always the best mortgage. Some lenders advertise low rates that require discount points, higher upfront fees, or specific borrower qualifications. A buyer should compare the full loan estimate instead of focusing only on the rate.

A stronger comparison looks at the interest rate, APR, lender fees, closing costs, loan type, and monthly payment. Buyers should also ask whether the quoted rate includes points. Paying points can lower the interest rate, but it increases upfront costs. This may make sense for someone who plans to keep the loan for a long time, but it may not be worth it for someone who plans to sell or refinance sooner.

Home Loan Rates Today in Utah

For many buyers, the search begins with home loan rates, home loan rates today, current home loan rates, home mortgage rates, home mortgage rates today, and current home mortgage rates. These searches all point to the same basic need: buyers want to understand what it will cost to borrow money for a home. The challenge is that mortgage rates are only one part of affordability.

A buyer should also consider property taxes, homeowners insurance, mortgage insurance, HOA fees, and closing costs. In Utah, local market conditions can also affect affordability. A buyer comparing Salt Lake City mortgage rates may face different home prices and competition than a buyer looking in a smaller Utah market. Because of this, it is smart to compare both the loan and the local housing market before making a decision.

Another useful resource for rate trends is the Freddie Mac mortgage rate survey.

Mortgage Rates Right Now: What Buyers Should Do Next

When evaluating mortgage rates right now, buyers should start by getting organized. This means checking their credit report, estimating a comfortable monthly payment, saving for a down payment, and gathering financial documents before applying. Being prepared can make the loan process smoother and may help the buyer qualify for better terms.

The next step is to compare multiple lenders. A buyer wondering how to get the best mortgage rate in Utah should not rely on only one quote. Comparing offers from banks, credit unions, mortgage brokers, and online lenders can reveal differences in rates and fees. Buyers should ask each lender for a loan estimate so they can compare the total cost of each option.

Final Thoughts on Utah Mortgage Rates

Finding the right mortgage is not just about chasing the lowest number. It is about understanding the full loan, comparing lenders, and choosing an option that fits your budget and goals. Utah buyers should pay close attention to the interest rate, APR, fees, loan type, and monthly payment before making a final decision.

Overall, researching Utah mortgage rates today can help buyers make smarter decisions. Whether someone is comparing current mortgage rates Utah, looking for best mortgage rates Utah, or trying to understand home loan rates today, the key is to compare carefully and look beyond the advertised rate. With the right preparation, Utah buyers can improve their chances of finding a mortgage that supports both their home purchase and their long-term financial goals.