When I started seriously thinking about buying my first home, the very first piece of advice everyone gave me was the same: get mortgage pre approval before you do anything else. It sounded like one more box to check, but it turned out to be the single most useful step in the entire process. A pre approval tells you exactly how much house you can afford, shows sellers you are a serious buyer, and surfaces any credit or income problems while there is still time to fix them. This guide walks first-time home buyers through the whole process, from checking your credit score to receiving your pre approval letter.

What Is Mortgage Pre Approval (and How Is It Different from Pre Qualification)?

Mortgage pre approval is a lender’s conditional commitment to loan you a specific amount, based on a real review of your credit report, income, assets, and debts. Pre qualification, by contrast, is just an estimate based on numbers you self-report, and no lender verifies any of it. That difference matters when you make an offer. A seller who receives two similar offers will almost always favor the buyer holding a pre approval letter, because that buyer’s financing has already been vetted. If you are choosing between the two, choose pre approval every time.

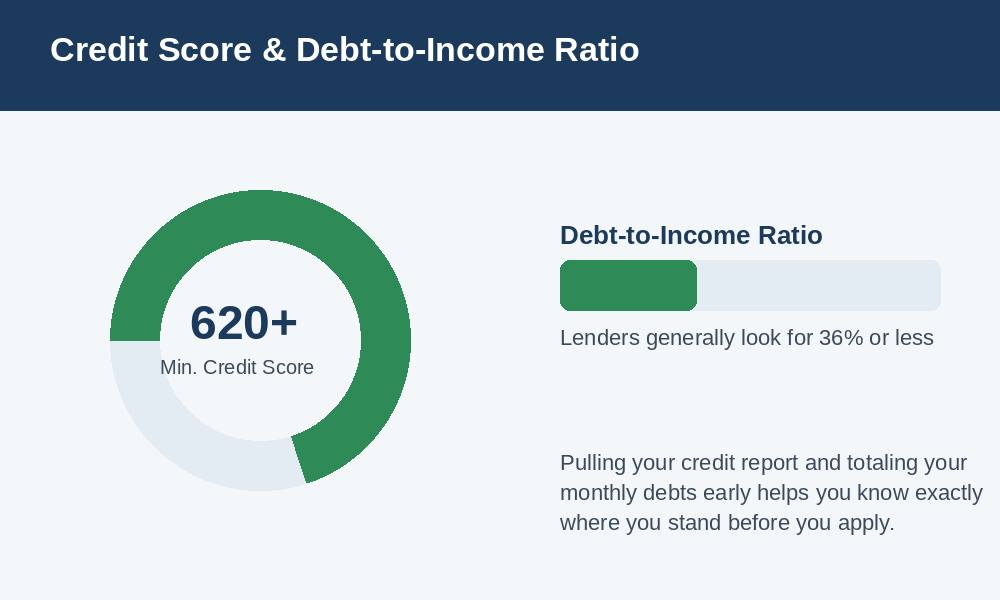

What Credit Score Do You Need to Buy a House?

Most conventional loans require a minimum credit score of 620, while FHA loans allow scores as low as 580 with a 3.5 percent down payment, or 500 to 579 with 10 percent down. But the minimum score only gets you in the door. Your interest rate improves as your score climbs, and buyers with scores of 740 or higher typically qualify for the best rates available. Before applying, pull your free credit reports, dispute any errors, pay balances below 30 percent of your credit limits, and avoid opening new accounts. Even a 20-point improvement can lower your monthly payment for the life of the loan.

Understanding Your Debt-to-Income Ratio

Your debt-to-income ratio, or DTI, is the percentage of your gross monthly income that goes toward debt payments, including your future mortgage payment. Most lenders want to see a DTI of 43 percent or less, and many prefer 36 percent. To calculate yours, add up your monthly debt payments (car loans, student loans, credit card minimums, and the estimated mortgage payment) and divide by your gross monthly income. If your DTI is too high, you have two levers: pay down debt or increase documented income. Paying off a car loan or a credit card in the months before you apply can meaningfully raise the loan amount you qualify for.

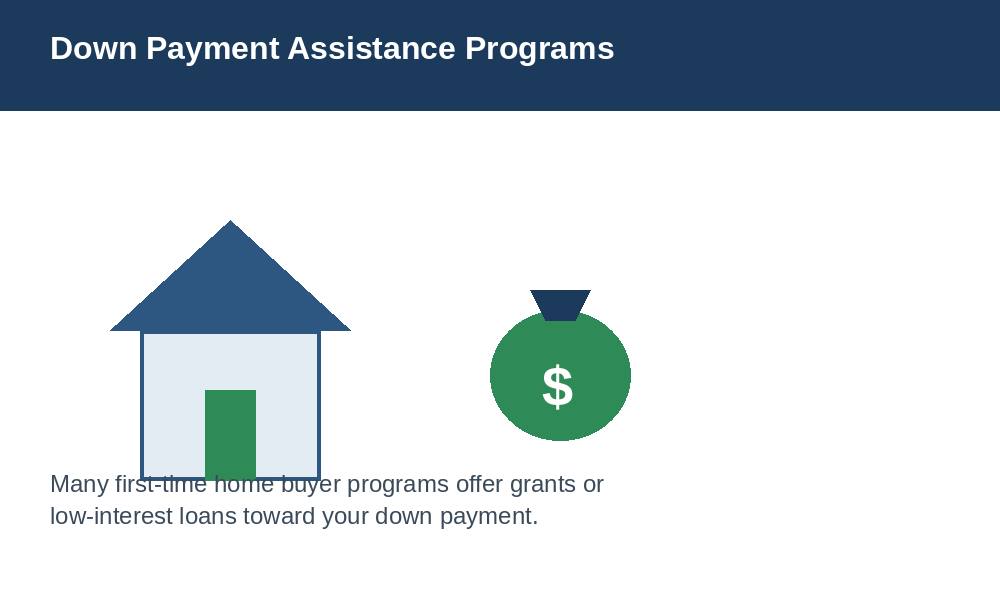

Down Payments and Down Payment Assistance for First-Time Buyers

You do not need 20 percent down to buy a home. Conventional loans allow as little as 3 percent down for first-time buyers, and FHA loans require 3.5 percent. Putting down less than 20 percent usually means paying private mortgage insurance, but it can still make sense if it gets you into a home sooner. First-time home buyers should also look into down payment assistance programs. Many states, counties, and housing authorities offer grants or low-interest second loans that cover part or all of a down payment, and some employers and credit unions offer assistance as well. Ask each lender you interview which programs they work with, because participation varies.

Documents You Need for Mortgage Pre Approval

Lenders verify everything, so gather your paperwork before you apply. Plan on providing your two most recent pay stubs, W-2s and federal tax returns from the last two years, two months of bank statements for every account, statements for retirement and investment accounts, a photo ID, and documentation for any other income such as bonuses or side work. Self-employed buyers should expect to provide two full years of business tax returns and a profit-and-loss statement. Having a clean folder ready to go can shrink the pre approval timeline from weeks to a couple of days.

How to Get Pre Approved: Compare Lenders and Apply

Do not stop at one lender. Rates, fees, and program availability vary more than most first-time buyers expect, and applying with three to five lenders lets you compare official Loan Estimates side by side. Credit bureaus treat multiple mortgage inquiries within a 45-day window as a single inquiry, so shopping around will not wreck your credit score. Once you choose a lender and submit your documents, underwriting reviews your file and issues a pre approval letter stating the maximum loan amount you qualify for.

Your Pre Approval Letter: What It Means and How Long It Lasts

A pre approval letter typically remains valid for 60 to 90 days, because your credit and income can change. Time your application so the letter is fresh when you start touring homes. Keep in mind that the letter states a maximum, not a recommendation; qualifying for a payment and being comfortable with it are two different things. And protect your approval between the letter and closing: do not open new credit cards, finance a car, change jobs, or make large unexplained deposits, because lenders re-verify your file before funding the loan.

Quick Answers: Mortgage Pre Approval FAQ

Does mortgage pre approval hurt your credit score?

It triggers a hard inquiry, which may drop your score a few points temporarily. Multiple mortgage inquiries within a 45-day shopping window count as one.

How long does mortgage pre approval take?

With documents ready, many lenders issue a pre approval letter within one to three business days.

How long does a pre approval letter last?

Usually 60 to 90 days. If it expires before you find a home, your lender can refresh it with updated documents.

Can you get pre approved with student loan debt?

Yes. Student loans count toward your DTI, but they do not disqualify you as long as your total DTI stays within the lender’s limit.

Is pre approval a guarantee that you will get the loan?

No. Final approval depends on the specific property, an appraisal, and re-verification of your finances at closing.

Getting mortgage pre approval is the moment house hunting stops being a daydream and starts being a plan. Check your credit score, know your debt-to-income ratio, gather your documents, compare a handful of lenders, and walk into your first showing with a pre approval letter in hand. For a first-time home buyer, there is no better way to start.