Utah homeowners have watched their property values climb steadily over the past decade — and with that growth comes a powerful financial tool many are only beginning to tap into: home equity. Whether you’re planning a kitchen remodel, consolidating high-interest debt, or funding a major life expense, understanding how to access the equity you’ve built is one of the smartest financial moves you can make. This guide breaks down the two most popular options — the home equity loan and the home equity line of credit — so you can decide which one fits your situation.

What Is a Home Equity Loan?

A home equity loan lets you borrow a lump sum against the equity in your home at a fixed interest rate. You receive all the money upfront and repay it in equal monthly installments over a set term — typically between 10 and 30 years. Because the rate is fixed, your payment never changes, making it easy to budget.

Lenders offering the best home equity loans generally require a credit score of 620 or higher, a debt-to-income ratio below 43%, and at least 15–20% equity in your home. Home equity loan rates today typically range from 7% to 10% depending on your credit profile, loan term, and lender. Comparing the best home equity loan rates from multiple lenders before committing can save you thousands over the life of the loan.

Some of the most well-known options come from major institutions. A Wells Fargo home equity loan, for example, offers competitive terms for borrowers with strong credit, while Discover home equity loans are known for no origination fees and flexible repayment terms. Shopping around and comparing best home equity lenders is always worth the extra effort.

What Is a HELOC?

A HELOC — or home equity line of credit — works more like a credit card than a traditional loan. Instead of receiving a lump sum, you’re approved for a credit limit and can draw from it as needed during a set “draw period,” usually 10 years. You only pay interest on what you actually use, which gives you flexibility that a standard loan doesn’t.

HELOC rates are typically variable, meaning they move with the market. Current HELOC rates and HELOC rates today hover between 8% and 12% for most borrowers, though your rate will depend on your credit score, loan-to-value ratio, and the lender you choose. Because HELOC interest rates can change month to month, it’s important to factor potential rate increases into your planning.

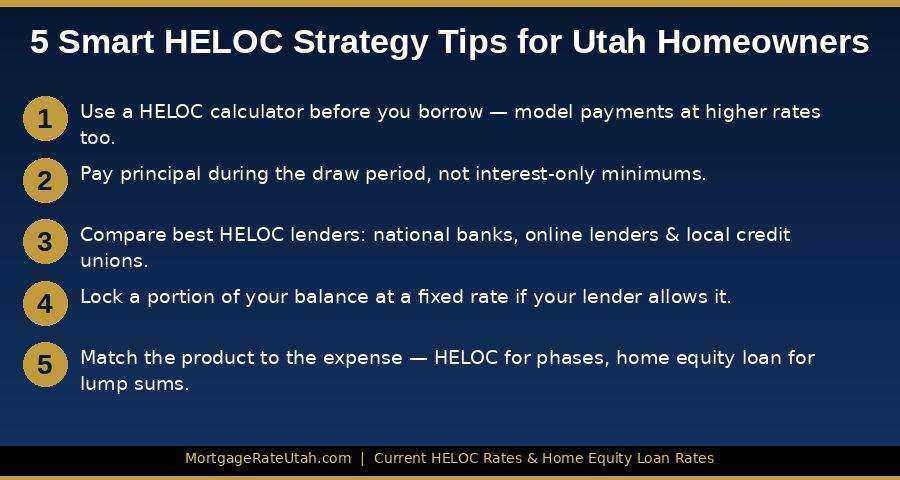

If you want to compare offers, tools like a HELOC calculator can help you estimate monthly payments under different rate scenarios. Pairing that with an amortization calculator gives you a full picture of how your balance decreases over time — and how much total interest you’ll pay.

HELOC vs. Home Equity Loan: Which Is Better for You?

The right choice depends on how you plan to use the money.

A HELOC loan is ideal if your expenses are ongoing or unpredictable — think a multi-phase home renovation, ongoing tuition payments, or a business you’re gradually building out. You can draw exactly what you need, when you need it, and leave the rest untouched.

A home equity loan is better when you have a single, well-defined expense — a roof replacement, a medical bill, or a debt consolidation payoff — and you want the predictability of a fixed payment.

For homeowners focused on long-term financial planning, developing a clear HELOC strategy before you open the line of credit matters just as much as the rate. Decide in advance how much you’ll draw, what you’ll use it for, and how aggressively you’ll pay it down during the draw period. Paying down principal early — rather than interest-only minimums — can dramatically reduce your costs when the repayment phase begins.

Finding the Best HELOC and Home Equity Products

Not all lenders are created equal. When searching for the best HELOC or the best home equity line of credit, look beyond just the rate. Consider origination fees, annual fees, minimum draw requirements, and whether the lender allows rate locks on a portion of your balance.

The Bank of America HELOC, for instance, is well-regarded for having no application fees, no closing costs, and the option to convert part of your variable-rate balance to a fixed rate. For borrowers who want rate certainty without fully committing to a home equity loan, this kind of flexibility is valuable.

When comparing home equity line of credit rates across lenders, pay attention to the index each lender uses to set your variable rate — most tie to the Wall Street Journal Prime Rate — and what margin they add on top. That margin is where lenders differentiate themselves, and it’s negotiable if you have strong credit.

For the best heloc rates available right now, check with local Utah credit unions in addition to the big national banks. Credit unions often offer lower margins and more personalized service, which can make a meaningful difference in your total cost.

The Bottom Line for Utah Homeowners

Utah’s rising home values have put real financial power in homeowners’ hands. Whether you pursue a home equity loan for a lump-sum need or a HELOC for flexible, ongoing access to funds, both products can be smart tools when used with a clear plan.

Start by using a HELOC calculator or amortization calculator to run the numbers on both options. Then compare the best home equity loan rates and best HELOC rates from at least three lenders — including local credit unions, national banks, and online lenders like Discover home equity loans — before making your decision.

Your home equity is one of your most valuable financial assets. Make sure you’re putting it to work in the way that serves your goals best.

For more Utah-specific mortgage guidance, explore our other posts on mortgage rates, refinancing, and first-time buyer programs at MortgageRateUtah.com.