Buying a first home is easier when the mortgage process is broken into clear decisions. A first time home buyer mortgage is not just one product. It is a financing choice that depends on credit, income, savings, location, interest rate, loan term, and long-term plans. Before comparing lenders, first-time buyers should understand what is a mortgage and why the loan structure matters. A simple mortgage definition is a loan used to buy property, where the home acts as collateral for the lender. That explains the basic legal relationship, but buyers also need to know how do mortgages work month by month.

First Time Home Buyer Mortgage Basics

A first-time buyer should begin by estimating the full monthly cost of owning the home, not just the listing price. Principal and interest are only part of the payment. Taxes, homeowners insurance, mortgage insurance, HOA dues, utilities, and maintenance can all change what is affordable. This is why the question how much mortgage can I afford should be answered before touring homes aggressively. A good budget protects the buyer from becoming house poor and gives the lender a clearer picture of the buyer’s comfort zone.

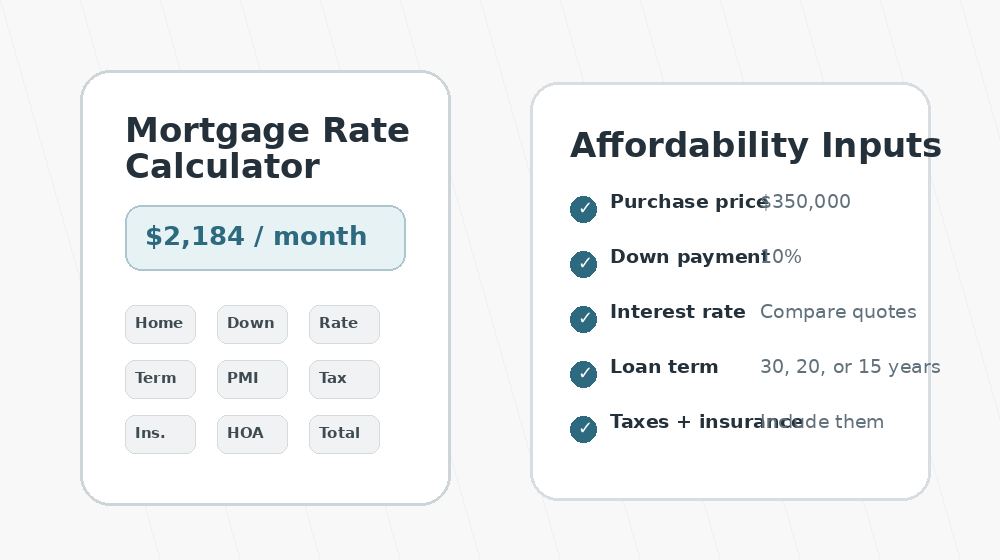

A mortgage rate calculator is one of the most useful tools in the early research stage. The buyer can enter a purchase price, down payment, interest rate, and term to estimate the payment. The calculator is especially helpful when comparing 30 year mortgage rates, 15 year mortgage rates, and 30 year fixed mortgage rates. A 30-year term usually lowers the monthly payment because the loan is spread out over a longer period. A 15-year term usually has a higher monthly payment but may reduce total interest over the life of the loan.

Mortgage Interest Rates Today and Loan Term Choices

Checking mortgage interest rates today helps buyers understand the current market, but the advertised rate is only a starting point. The actual rate can change based on credit score, down payment, loan amount, property type, loan program, and whether the buyer pays points. Buyers should compare official loan estimates rather than relying on one rate shown online. They should also ask whether the payment estimate includes taxes, insurance, and mortgage insurance.

For many buyers, the main decision is between a fixed rate mortgage and an adjustable rate mortgage. A fixed-rate loan keeps the principal and interest portion of the payment stable for the life of the loan. That predictability can be valuable for first-time buyers who are still adjusting to the cost of homeownership. An adjustable-rate mortgage may start with a lower rate, but the rate can change after the introductory period. That can be useful for someone who expects to sell or refinance within a few years, but it adds payment risk.

Some buyers also need to understand jumbo mortgage rates. A jumbo loan is used when the loan amount is above the standard conforming loan limit for the area. These loans may require stronger credit, more savings, and lower debt levels. First-time buyers considering a jumbo mortgage should compare the payment carefully and ask the lender what reserves or documentation will be required.

First Time Home Buyer Loan Programs

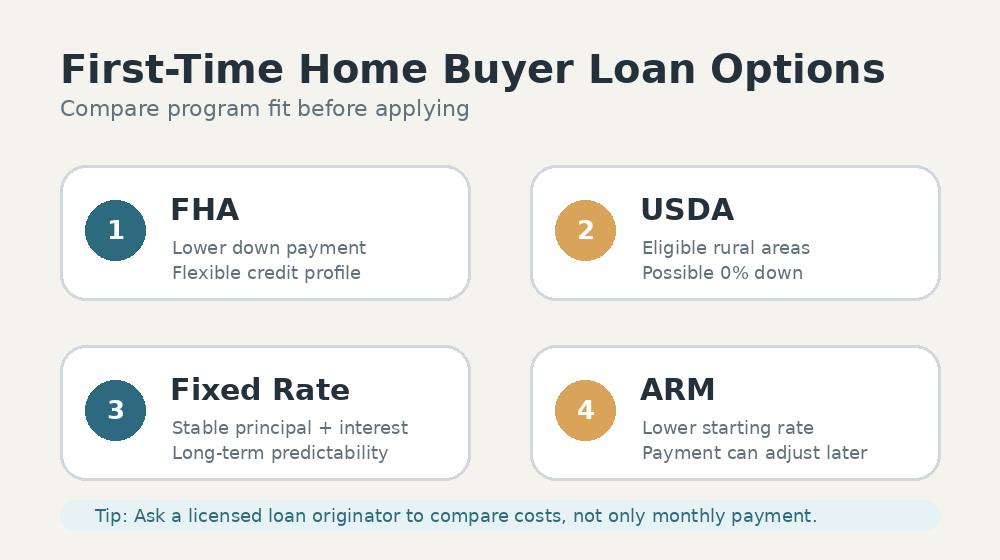

A first time home buyer loan can come from several program types. Conventional loans are common for buyers with stronger credit and savings. FHA loans can help buyers who need more flexible credit or down payment requirements. Anyone researching FHA should review fha loan requirements and compare fha mortgage rates with conventional options. FHA can be useful, but the buyer should understand mortgage insurance and how it affects the monthly payment.

A usda home loan may help eligible buyers purchasing in qualified rural or suburban areas. This can be attractive for buyers looking outside dense city centers, but eligibility depends on the property location and borrower qualifications. Buyers should also ask about state or local assistance programs, especially if down payment or closing costs are the biggest challenge.

How to Apply for a Mortgage

Learning how to apply for a mortgage early makes the process smoother. A buyer usually needs pay stubs, W-2s, tax documents, bank statements, photo identification, and a list of current debts. The lender reviews income, assets, credit, debt-to-income ratio, and the property being purchased. A pre-approval is not a final approval, but it helps the buyer shop in a realistic price range and make a stronger offer.

This is also where professional guidance matters. Some buyers search for a mortgage company near me because they want direct support from a lender. Others search for a local mortgage broker because they want help comparing multiple lending options. In either case, a licensed mortgage loan originator should explain the difference between rate, APR, loan fees, mortgage insurance, closing costs, and cash needed at closing.

Good mortgage advice should be specific to the buyer’s situation. A buyer with limited savings may need a low-down-payment loan. A buyer with high income but little time may value speed and certainty. A buyer who expects to move in five years may compare an ARM with a fixed option. A buyer who wants long-term stability may choose a 30-year fixed loan even if another product appears cheaper at first.

Pros and Cons of a 30 Year Mortgage

The pros and cons of a 30 year mortgage are important because the 30-year loan is one of the most common options for first-time buyers. The biggest advantage is payment flexibility. A lower required monthly payment can leave room for savings, repairs, furniture, emergencies, and future life changes. The main disadvantage is total interest. Because the loan lasts longer, the borrower may pay more interest over time than with a shorter loan.

The best mortgage choice is the one that fits the buyer’s monthly budget and long-term plan. A buyer should compare loan term, rate type, program requirements, closing costs, and future refinance possibilities. Later, if market conditions improve, the homeowner may compare best mortgage refinance options and mortgage refinance rates. Refinancing can reduce a payment, shorten a term, or move from an adjustable loan into a fixed loan, but the closing costs should be measured against the savings.

A first-time buyer does not need to know every mortgage rule before getting started. They need a clear budget, a basic understanding of loan types, and a lender who can explain the numbers in plain language. When buyers compare rates, use calculator tools, ask better questions, and choose a program that fits their life, the mortgage process becomes much easier to manage.

Learn more: CFPB guide to mortgage loan types

Try it: Fannie Mae mortgage calculator