The dream of homeownership in the Beehive State is an exciting journey, but navigating today’s

market can feel like chasing a moving target. With the housing market mortgage rates

experiencing constant shifts, local buyers often find themselves wondering exactly what it takes

to transition from casually browsing homes online to holding the keys to a new property. When

you first begin your search, it is completely natural to look at a national index or play around

with a basic web tool to see what your monthly payment might look like. However, there is a

massive structural difference between an unverified web estimate and a firm, underwritten file. If

you want to successfully secure a property in Utah’s competitive real estate landscape, you need

a concrete, step-by-step strategy to move from digital speculation to true transactional readiness.

Current Mortgage Rates and the Limitations of Online

Estimators

When analyzing current mortgage rates, remember that the lowest advertised rate online isn’t

automatically the rate you will receive. For most buyers, the journey begins with an online

mortgage calculator. You type in a home price, plug in an estimated down payment, and look at

the resulting number. While these tools are fantastic for a baseline visual, they operate in a

vacuum. They rarely account for localized property taxes, exact home insurance premiums, or

the specific pricing adjustments that lenders apply based on individual credit profiles. To stay

grounded on what benchmark products look like systematically, buyers can review the market

data updated weekly by Freddie Mac’s Primary Mortgage Market Survey. Relying solely on a

generic tool can lead to severe sticker shock later on. For instance, if you are looking at a

higher-end market and calculating jumbo mortgage rates, a minor fluctuation in your final

qualified tier can swing your monthly obligation by hundreds of dollars. To protect your budget,

you need a tool that digs deeper into your actual financial health. Utilizing a mortgage

prequalification calculator is a much smarter starting point, as it begins to look at your actual

financial baseline rather than just hypothetical numbers.

Mortgage Pre-Approval Requirements: DTI, Income, and

Assets

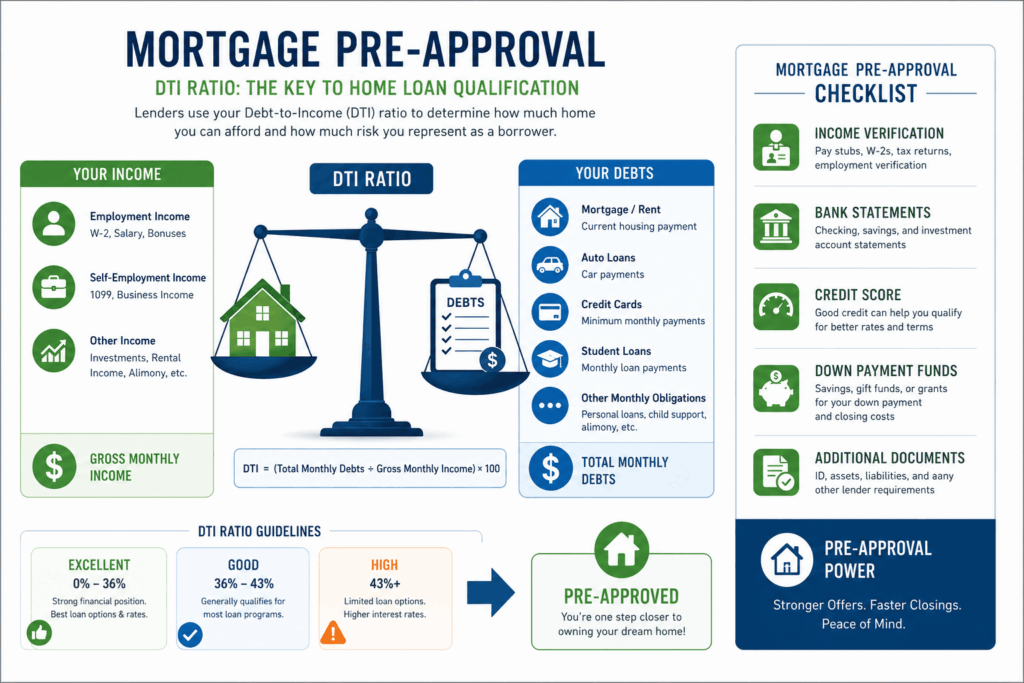

Securing a formal mortgage pre approval requires a deep dive into your personal financial

history. Before you ever speak with a loan officer, you need to understand the two heavyweights

of lending criteria: your assets and your debts. First, let’s look at the cash required to close.

Determining your down payment for house purchases isn’t just about hitting a magical 20%

mark. While 20% down avoids private mortgage insurance (PMI), many federal and state loan

programs allow you to buy a home with as little as 3% to 3.5% down. Second, lenders will

scrutinize how much of your gross monthly income is already spoken for by existing liabilities.

Your debt to income ratio for mortgage qualification—often referred to as your DTI—is

arguably the most critical metric on your application. Lenders cross-reference these percentages

through automated underwriting systems to see how safely you can handle a new monthly

payment. Understanding this formula is the exact key to figuring out what am i qualified for

mortgage options across the state. When you formally request a home loan pre approval or

house loan pre approval, you are essentially completing the heavy lifting of the mortgage

application upfront. Having an official letter in hand proves to real estate agents and sellers that

you have the confirmed financial backing to close the deal. In a tight real estate market, a

verified house loan pre approval letter is often the exact tie-breaker that causes a seller to

choose your offer over a competitor’s.

Mortgage pre-approval infographic showing debt-to-income ratio calculation, income

verification, credit score requirements, bank statements, and down payment savings

Activating Specialized and Local Loan Programs

One of the biggest content gaps on nationwide financial sites is the failure to highlight localized

assistance. Utah buyers have access to incredible lending vehicles designed to make

homeownership highly accessible. If you have never owned a home before, or haven’t owned one

in the past three years, you should aggressively explore specific first time home buyer

programs. These can include down payment assistance grants and zero-interest second

mortgages that cover your upfront transactional costs. Depending on where you are looking to

buy and your personal background, standard conventional financing might not be your best path.

An fha home loan is backed by the Federal Housing Administration and features more lenient

credit requirements and a low 3.5% down payment baseline. If you are a military member or

veteran, a va loan offers a zero-down payment structure and some of the most competitive terms

in the entire industry. Meanwhile, if you are looking at more rural or suburban developments

(such as parts of Tooele, Utah, or Weber counties), a usda mortgage provides another zero-down

framework targeted at rural development.

Best Mortgage Lenders in Utah: Navigating Your Closing

Options

Finding the best mortgage lenders means searching for professionals who provide custom

tailored strategies rather than standard automated answers. The final piece of the housing puzzle

is selecting who will originate your loan. You should never simply accept the first offer from a

national bank. Instead, take the time to interview and vet reputable mortgage lenders who

understand the unique nuances of the Utah real estate landscape. A good loan officer will

carefully monitor the market shifts to lock in the lowest mortgage refinance rates or purchase

rates on your behalf. Furthermore, checking house loan rates today is a vital habit because

pricing can move drastically based on daily financial shifts. For live context on how localized

daily adjustments behave, buyers can review the pricing structures dynamically managed on

pages like the U.S. Bank Mortgage Rate Tracker. Top tier institutions will do far more than just

quote you a random interest rate. They will look at your long-term wealth goals, evaluate

whether a cash out refinance makes sense down the road, map out your home equity loan rates

if you want to tap into future equity, or set up a flexible heloc loan for subsequent home

renovations. When you are ready to take the leap, gather your financial documents, visit our

internal portal to apply for a mortgage online, or read our breakdown on how to get pre approved

for a home loan locally. By moving methodically from an online calculation to a verified

certified status, you place yourself in the absolute best position to secure the perfect home for

your family.

Utah neighborhood with Wasatch Mountain backdrop illustrating FHA loans, VA loans, USDA

loans, and down payment assistance programs for homebuyers