Most Utah buyers start their home search backwards. They spend weekends touring homes, fall in love with something, then find out the financing doesn’t work. The fix is simple: mortgage pre-approval first, house hunting second.

This guide walks through the full mortgage pre-approval process — what lenders look at, what you need to prepare, and how to make yourself the strongest possible applicant in Utah’s competitive housing market.

Mortgage Pre-Approval vs. Pre-Qualification: What’s the Difference?

Mortgage pre-qualification — sometimes called pre-qualify mortgage — is a surface-level estimate. You share basic income and debt information, the lender does a soft credit pull, and you get a rough range of what you might borrow. It takes a few minutes and carries almost no weight with sellers.

Mortgage pre-approval is different. A lender actually verifies your income, reviews your credit, and issues a conditional commitment. When you submit an offer with a pre-approval letter, sellers take it seriously. If you’re asking how to prequalify for home loan as a starting point, that’s fine — but don’t stop there. In Utah’s market, you need the full pre-approval.

What is Needed to Get Pre-Approved for a Mortgage

Most buyers ask what is needed to get pre-approved for a mortgage at the wrong time — after they’ve already found a property. Do this before you start looking.

Here’s what lenders will ask for:

- W-2s and tax returns from the past two years

- Recent pay stubs (typically the last 30 days)

- Bank and asset statements from the past 60 days

- Government-issued ID

- Employment history (lenders want two years of consistent employment)

- Documentation of any other income — rental income, alimony, freelance work

If you’re self-employed, budget additional time. Lenders will want two years of business returns and a profit-and-loss statement.

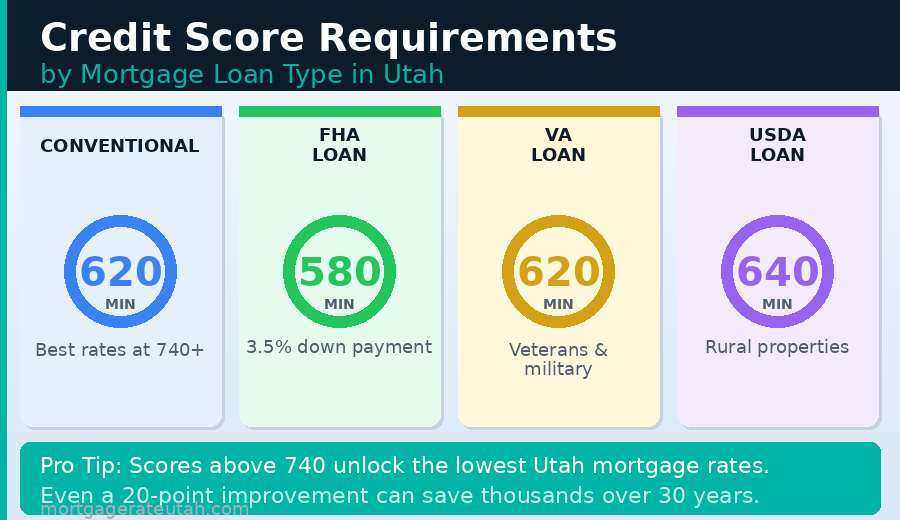

Credit Score to Buy a House in Utah: What You Need

Credit score to buy a house is one of the most-searched questions in Utah real estate, and for good reason — it’s one of the biggest levers you control.

Here’s what most loan programs require:

- Conventional loans: 620 minimum

- FHA: 580 (3.5% down) or 500 (10% down)

- VA: no official minimum, most lenders want 620+

- USDA: 640 preferred

The minimum credit score for mortgage approval is one thing. What gets you the best rate is another. Borrowers above 740 consistently receive the most competitive pricing. If your mortgage credit score is below 680, it’s worth spending 3–6 months improving it before applying — even a 20-point improvement can save tens of thousands over the life of a 30-year loan.

Quick ways to strengthen your score before applying:

- Pay down revolving balances below 30% of your credit limit

- Don’t open any new accounts

- Dispute any errors on your credit report

- Avoid closing old accounts

Debt to Income Ratio for Mortgage Approval: The Other Number That Matters

Your credit score gets most of the attention, but debt to income ratio for mortgage approval is just as important.

Debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments — including your future mortgage. Most lenders want your total DTI below 43–45%. FHA loans can sometimes allow up to 50% with compensating factors.

Example: If you earn $7,000 per month and your proposed mortgage payment plus existing debts total $2,800, your DTI is 40%. That’s workable for most loan programs.

To improve your DTI before applying, pay down credit card balances, avoid financing a new car, and don’t take on new installment debt of any kind.

How Much Can I Qualify for a Home Loan? Using a Mortgage Affordability Calculator

How much can I qualify for a home loan is usually the first question buyers have. The answer depends on income, debts, credit, and current rates.

A rough starting point: most lenders allow a housing payment up to 28–31% of your gross monthly income (the “front-end ratio”), though the actual number depends on your full financial picture.

How much mortgage can I qualify for is best answered with a mortgage pre-approval calculator — these tools factor in your income, existing debts, credit score, and the current rate environment to give you a realistic ceiling. A mortgage affordability calculator takes it a step further by helping you figure out not just what you can borrow, but what monthly payment you can actually sustain without financial strain.

Worth knowing: the number lenders will approve and the number that’s comfortable for your life are often different. Build in room for property taxes, HOA fees, insurance, maintenance, and the unexpected. Many Utah buyers at the top of their approval range end up feeling house-poor within a year.

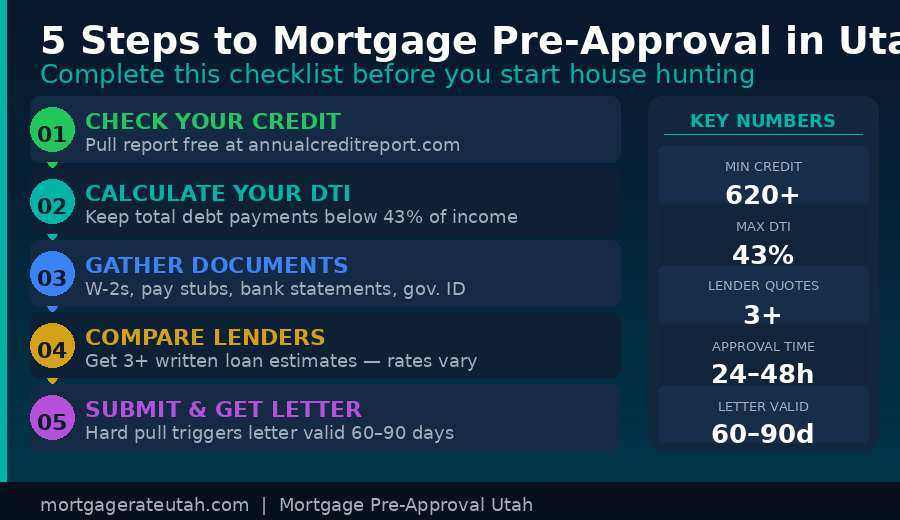

How to Get Pre-Approved for a Mortgage: Five Steps

How to get pre-approved for a mortgage comes down to five steps:

- Check your credit. Pull your credit report at annualcreditreport.com [https://www.annualcreditreport.com] and review it for errors before a lender does. Fix any issues you find.

- Calculate your DTI. Add up your monthly debt payments (credit cards, car loans, student loans), divide by your gross monthly income, and multiply by 100. If it’s above 43%, work on reducing it before applying.

- Gather documents. Use the list above. Getting this together before you start talking to lenders saves a week of back-and-forth.

- Talk to multiple lenders. Studies consistently show that borrowers who get three or more quotes save meaningfully on rate and fees. Don’t assume the first offer is the best one.

- Submit your application and get your letter. The formal application triggers a hard credit pull. Once approved, you’ll receive a pre-approval letter specifying the loan amount, loan type, and expiration date (usually 60–90 days).

If you’re wondering how to get pre-approved for a home loan as quickly as possible, the biggest variable is document readiness. Buyers who walk in with everything organized can get pre-approved in 24–48 hours.

Utah First Time Home Buyer Programs and Loans

The Utah housing market has specific dynamics that matter at the pre-approval stage.

Home prices across the Wasatch Front have stayed elevated. Salt Lake County median prices regularly exceed $500,000, which means many buyers need to be deliberate about what they qualify for before shopping. Getting your pre-approval number locked in isn’t just administrative — it defines the neighborhoods you’re realistically looking at.

If you’re a Utah first time home buyer, there are additional programs worth knowing about:

Utah Housing Corporation (UHC) [https://utahhousingcorp.org/homebuyer/sb240/] offers down payment assistance loans for eligible buyers. The SB 240 First-Time Homebuyer Assistance Program provides up to $20,000 in assistance for new construction homes. These programs have income limits and purchase price caps, so they’re not for everyone — but for buyers who qualify, they meaningfully reduce upfront costs.

First time home buyer programs typically define “first-time buyer” as someone who hasn’t owned a home in the past three years, which opens eligibility to a broader group than the name suggests.First time home buyer loans — including FHA, USDA, and certain conventional programs — allow lower down payments and more flexible credit standards than standard conventional financing. FHA loans remain the most common choice for first-time buyers in Utah because of the 3.5% down payment minimum and the relatively accessible credit requirements. See also: Utah First Time Home Buyer Loan Guide

Mortgage Lenders Near Me: How to Find the Right Fit in Utah

When it comes to deciding where to apply for a mortgage, the lender you choose matters as much as the loan program.

Working with a mortgage lender Utah who understands the local market — seasonal inventory patterns, property tax structures, common HOA situations in newer communities — can make the process go more smoothly than working with a national online lender who treats every state the same.

If you’re searching mortgage lenders near me or specifically a mortgage broker Salt Lake City, the distinction matters. A bank or direct lender originates its own loans, which means one set of products and pricing. A mortgage broker works across multiple wholesale lenders and can shop your application to find competitive pricing — potentially valuable if your financial profile has any complexity.

A home loan Utah through a local credit union is another option worth considering. Utah has one of the densest credit union markets in the country, and they frequently offer pricing that competes with or beats the big national banks.

Regardless of where you apply for a mortgage, get written loan estimates from at least two to three sources. The rate, origination fees, and APR will differ between them, and comparing formally — not just verbally — is how you make sure you’re not leaving money on the table. See also: Utah Mortgage Rates Today and CFPB Loan Estimate guide

After Pre-Approval: What Comes Next

Your pre-approval letter is the starting line, not the finish line.

Once you have it, keep your finances stable. Don’t open new credit accounts, don’t make large unexplained deposits, don’t change jobs without talking to your lender first. Underwriters will re-verify your financial picture before closing, and anything that’s changed from what was on your application will slow things down.

Pre-approval letters typically expire in 60–90 days. If you’re taking longer to find the right home, you may need to refresh your application.

The process works best when buyers treat pre-approval as the beginning of a partnership with their lender — not a box to check and forget.

Quick Reference: What Affects Your Pre-Approval

Credit score: 620+ minimum; 740+ for best rates

DTI ratio: Under 43–45% total

Employment: 2+ years consistent history

Down payment: 3–20%+ depending on loan type

Income documentation: 2 years W-2s, recent pay stubs

Getting pre-approved for a mortgage in Utah isn’t complicated, but it does reward preparation. Buyers who understand what lenders are looking at, fix problems before they apply, and shop across multiple lenders consistently get better outcomes than those who rush the process. Start there, and the rest of the homebuying journey gets significantly easier.