Mortgage Loan Processing Time: What to Expect

At first, applying for a home loan may seem overwhelming. However, understanding what to expect can help reduce uncertainty and you can apply for a mortgage loan now! Once you apply, the lender immediately begins reviewing your finances, verifying your details, and ordering a home appraisal. Typically, the home loan processing time lasts between 30 and 45 days. Nevertheless, this can vary depending on your financial profile, loan type, and how quickly you submit required documents.

https://www.mortgagerateutah.com/understanding-mortgage-rates-for-first-time-utah-homebuyers/

The Mortgage Application Process

Now that you know the typical timeline, let’s look at what actually happens during that time. The mortgage application process begins with preapproval—this gives you a clear sense of your budget. After that, you’ll submit a formal application. From there, the lender evaluates your credit, income, and assets during underwriting. Once approved, you’ll schedule a closing and sign your final loan documents.

Mortgage Documents Needed to Get Started and Apply

To keep things moving smoothly, you’ll want to have your documents ready early. Most lenders require:

- Recent pay stubs or income statements

- W-2s or tax returns from the past two years

- Bank statements

- A valid photo ID

- Proof of employment

By gathering these mortgage documents ahead of time, you’ll speed up the approval process and reduce the chance of delays.

Mortgage Loan Terms You Should Know

As you fill out your application and review loan options, you’ll likely encounter unfamiliar terminology. Key mortgage terms include:

- Fixed-rate vs. adjustable-rate (ARM): Fixed rates remain constant, while ARMs may increase or decrease over time.

- Loan term: Most commonly 15 or 30 years, this defines how long you’ll repay your loan.

- Principal and interest: The principal is the loan amount; interest is the cost of borrowing.

- Escrow: A third-party account that holds funds for taxes and insurance.

Understanding these terms will help you compare loan offers with confidence.

Choosing the Right Mortgage Loan for You

With a basic understanding of terms, the next step is choosing the right loan. If you’re looking for lower payments upfront, an interest only mortgage might work for you—this lets you pay just the interest for a set period before principal payments begin.

Alternatively, if you’re buying in a rural or suburban area, a USDA mortgage could offer zero down payment and competitive rates—perfect for buyers who meet income and location requirements

Down Payment Assistance for Homebuyers

Many buyers struggle with saving enough for a down payment—but down payment assistance programs can help. These programs may offer grants, low-interest loans, or forgivable loans to cover part of your upfront costs. They are often available for first-time buyers, low-income households, or those purchasing in certain areas.

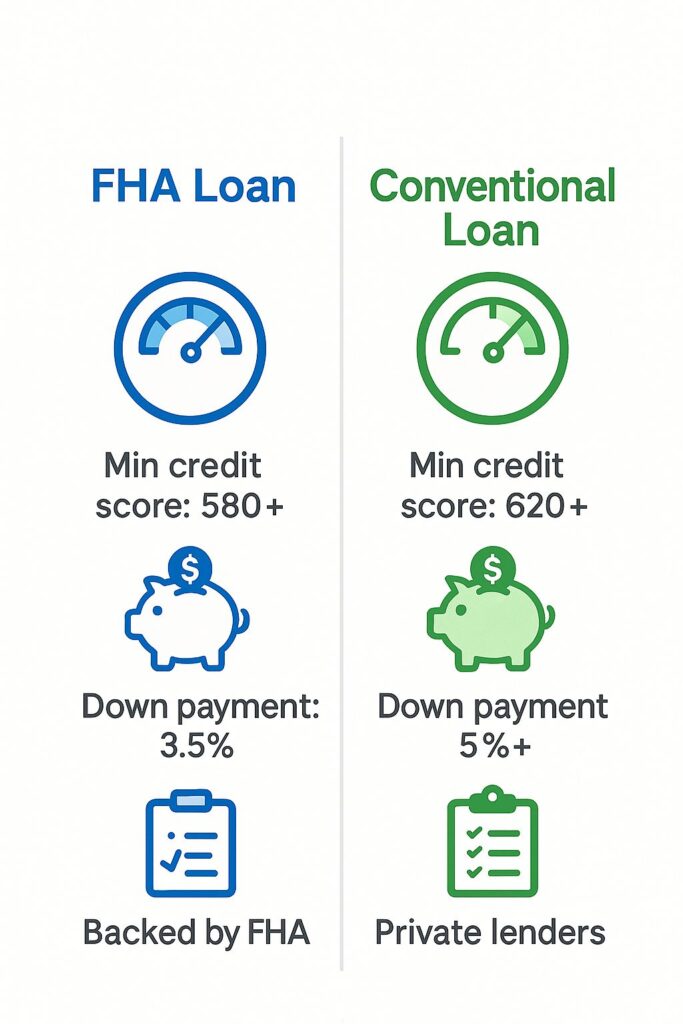

Mortgage Insurance: What you need to know

If your down payment is less than 20%, your lender will likely require mortgage insurance. This protects the lender—not you—in case of default. Conventional loans use PMI (Private Mortgage Insurance), while FHA and USDA loans include their own insurance structures. Make sure to factor this into your monthly costs.

Refinancing with Bad Credit: Know Your Options

Yes, you can still refinance with less-than-perfect credit. Government-backed programs—such as the FHA Streamline or VA IRRRL—allow qualified borrowers to lower their monthly payments or move into a fixed-rate mortgage. While your interest rate may be higher, refinancing can still offer long-term savings and stability

You can Apply Today!

Buying a home is one of the most meaningful financial decisions you’ll ever make—and you don’t have to do it alone. By understanding the loan process, preparing your documents, and exploring the right mortgage options, you’re already one step closer to achieving your goal. Whether you’re a first-time buyer, exploring refinancing, or looking for down payment support, the tools and resources are within reach. So take that next step with confidence and apply for a mortgage loan now—your new home is closer than you think.