Current Mortgage Rates Utah: What Buyers Should Know Before Choosing a Loan

Utah buyers searching for mortgage rates today are usually trying to answer one basic question: can I afford the payment right now? That question matters more than trying to guess the perfect time to buy. Current mortgage rates Utah buyers see online can change quickly, but the bigger decision is understanding how rates, loan terms, fees, and lenders all work together.

For most borrowers, current mortgage rates are only the starting point. A lender may advertise one rate, but the final number can depend on credit score, down payment, debt-to-income ratio, loan size, property type, and whether the borrower is buying or refinancing. This is why mortgage interest rates should always be compared with APR, because APR includes more of the cost of the loan.

If you are reviewing mortgage rates Utah today, you will probably see different numbers for 30-year fixed, 15-year fixed, FHA, VA, conventional, jumbo, and refinance loans. Utah mortgage rates 30 year fixed are popular because the longer term usually creates a lower monthly payment. Current 30 year mortgage rates in Utah can be a good fit for buyers who want flexibility, especially in higher-priced markets like Salt Lake City.

Current 15 year mortgage rates in Utah are usually lower than 30-year rates, but the monthly payment is higher because the borrower repays the loan faster. The main benefit is long-term interest savings. Buyers who have stable income and want to build equity faster may prefer the 15-year option, while buyers who need more budget room may choose a 30-year fixed loan and make extra payments when possible.

Loan type also matters. Utah conventional loan rates are common for borrowers with solid credit and enough down payment. Utah FHA mortgage rates may help buyers who need more flexible credit or down payment requirements. Utah VA mortgage rates can be valuable for eligible veterans and service members because VA loans often have strong terms. Utah jumbo loan rates apply when the loan amount is above the conforming loan limit, which can happen in expensive Utah neighborhoods.

Refinancing is a separate decision. Utah refinance mortgage rates today may be slightly different from purchase rates. Refinance mortgage rates can make sense if the new loan lowers the monthly payment, shortens the term, removes mortgage insurance, or helps a homeowner consolidate costs. However, closing costs should always be compared against the expected savings.

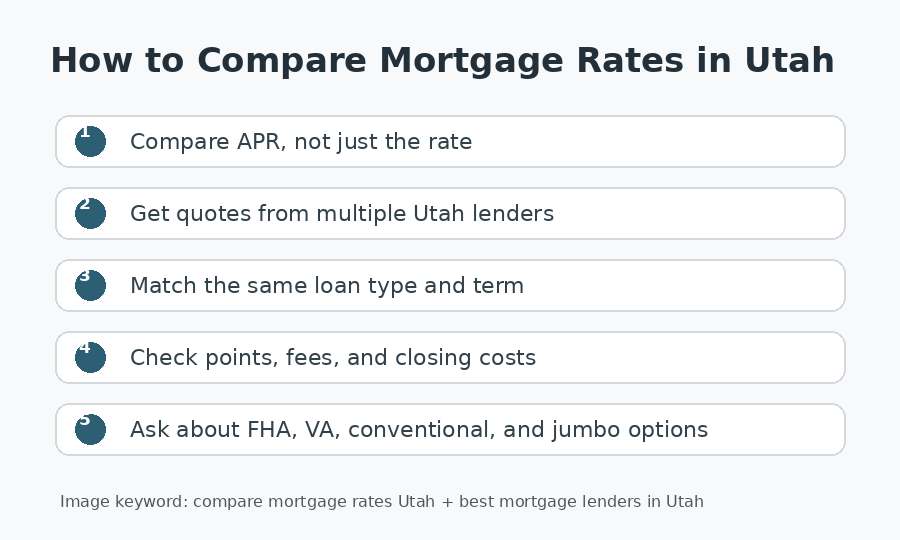

Buyers should compare mortgage rates Utah from more than one lender. Mortgage lenders Utah rates can vary even for the same borrower on the same day. The best mortgage rates Utah buyers qualify for usually come from shopping carefully, asking for the same loan type and term from each lender, and comparing lender fees as well as interest rates.

For local buyers, mortgage rates Salt Lake City and Salt Lake City mortgage rates today may follow national trends, but local housing prices, competition, and lender experience still matter. Home loan rates Utah buyers receive are connected to both the market and the borrower’s personal profile. First-time buyers should pay close attention to loan programs, down payment options, and the total monthly housing payment, not just the advertised rate.

The best mortgage lenders in Utah are not always the ones with the lowest advertised number. The best lender is the one that offers a strong combination of rate, APR, service, closing speed, loan options, and clear communication. To find the best mortgage rates, Utah borrowers should gather quotes, compare loan estimates, and choose a mortgage that fits their long-term financial goals.

Current Mortgage Rates Utah: How to Compare Rates, Lenders, and Loan Options

If you are searching for current mortgage rates Utah, you are probably trying to make a real decision: buy now, wait, refinance, or compare lenders before choosing a loan. That is why a good mortgage-rate guide should do more than list a number. Rates change daily, but the way you compare them stays fairly consistent. A Utah buyer needs to understand the difference between the interest rate, APR, fees, loan type, and monthly payment before deciding which offer is actually the best deal.

Across the country, mortgage rates today are still one of the biggest factors affecting affordability. A small change in mortgage interest rates can shift a monthly payment by hundreds of dollars, especially in Utah markets where home prices have stayed high. For buyers in Salt Lake City, Utah County, Davis County, and growing communities along the Wasatch Front, the goal should not be to chase the lowest advertised rate. The goal should be to compare the full cost of the loan and choose the option that fits your budget for the long run.

Mortgage Rates Utah Today: Why Advertised Rates Are Only a Starting Point

When people look up mortgage rates Utah today, they often see a single rate number and assume that is the rate they will receive. In reality, advertised rates are usually based on a very specific borrower profile. The quote may assume excellent credit, a certain down payment, a single-family primary residence, a specific loan amount, and discount points paid upfront. Your actual home loan rates can be higher or lower depending on your own financial situation.

This is why the phrase current mortgage rates should always be paired with a second question: current for whom? A borrower with a higher credit score, lower debt-to-income ratio, and larger down payment will usually qualify for better pricing than a borrower with more risk factors. Even two people buying similar homes in the same Utah city can receive different Utah mortgage interest rates because lenders evaluate borrower risk differently.

The smartest move is to compare APR as well as the interest rate. The rate tells you the cost of borrowing the principal balance, but APR includes additional loan costs. If one lender offers a lower rate but charges higher fees or points, it may not actually be the cheaper loan. This is one of the most important reasons to compare mortgage rates Utah using full loan estimates instead of only website rate tables.

Utah Mortgage Rates 30 Year Fixed vs. 15 Year Fixed

For many buyers, Utah mortgage rates 30 year fixed are the first option they consider. A 30-year fixed mortgage spreads the loan across a longer repayment period, which usually creates a lower monthly payment than a 15-year loan. That lower payment can be useful in Utah, where many buyers are balancing home prices, property taxes, insurance, utilities, and family expenses. Current 30 year mortgage rates in Utah are especially important for buyers who want predictable payments and more room in the monthly budget.

The trade-off is that a 30-year mortgage usually costs more in total interest over the life of the loan. That is where current 15 year mortgage rates in Utah become attractive. A 15-year fixed loan often comes with a lower rate and allows the borrower to build equity faster. However, the monthly payment is higher because the loan is paid off in half the time. A 15-year loan can be a strong choice for buyers with stable income, low debt, and enough cash flow to handle the larger payment comfortably.

Neither option is automatically better. The right decision depends on the borrower. If the 15-year payment creates stress, a 30-year fixed mortgage may be safer. A buyer can choose the 30-year loan and make extra principal payments when possible. If the buyer wants to minimize total interest and can handle the payment, the 15-year loan may be worth serious consideration.

Mortgage Rates Salt Lake City Buyers Should Watch

Local search terms like mortgage rates Salt Lake City and Salt Lake City mortgage rates today matter because many Utah buyers want information that feels relevant to their actual market. Salt Lake City housing costs can make small rate differences feel much larger. Even a modest difference in APR can affect affordability when the loan amount is high, which is why buyers should compare more than one lender before locking a rate.

At the same time, mortgage rates are not completely separate by city. Home loan rates Utah buyers receive usually follow national mortgage-market trends, but local lender competition, loan programs, and property values can still affect the final offer. A Salt Lake City buyer should look at both national rate averages and local lender quotes before deciding whether a rate is competitive.

Utah FHA, VA, Conventional, and Jumbo Loan Rates

Loan type is one of the biggest reasons two borrowers can receive different quotes. Utah conventional loan rates are common for borrowers with stronger credit, steady income, and enough down payment to qualify under conventional guidelines. Conventional loans can be a good fit for many Utah buyers, but they may not be the best option for every situation.

Utah FHA mortgage rates may appeal to buyers who need more flexible credit or down payment requirements. FHA loans can be especially useful for buyers who have enough income to make the payment but do not have a large down payment saved. For eligible military borrowers, Utah VA mortgage rates can be very competitive, and VA loans may offer advantages such as no required down payment in many cases. Buyers should compare the total cost of each loan type, not just the rate, because mortgage insurance, funding fees, and closing costs can change the overall value.

Utah jumbo loan rates apply when the loan amount is above the conforming loan limit. Jumbo loans are more common in expensive areas or for larger properties. Because jumbo loans create more lender risk, qualification standards may be stricter, and the rate structure may differ from a standard conventional mortgage.

Utah Refinance Mortgage Rates Today: When Refinancing Might Make Sense

Homeowners searching for Utah refinance mortgage rates today are usually hoping to lower their payment, shorten their loan term, or improve their overall loan structure. Refinance mortgage rates can be slightly different from purchase rates, so it is important to compare refinance-specific quotes. A refinance may make sense if the savings outweigh the closing costs and if the homeowner expects to stay in the home long enough to reach the break-even point.

A refinance can also be useful for someone who wants to move from an adjustable-rate mortgage into a fixed loan, remove mortgage insurance, or switch from a 30-year mortgage to a 15-year mortgage. However, refinancing is not automatically a good idea just because rates are lower than a homeowner’s current loan. The best decision depends on closing costs, remaining loan term, monthly savings, and long-term financial goals.

Utah Mortgage Rates for First Time Buyers

Utah mortgage rates for first time buyers deserve special attention because first-time buyers often focus too heavily on the rate and not enough on the total payment. A monthly housing payment can include principal, interest, property taxes, homeowners insurance, mortgage insurance, and HOA dues. A low advertised rate does not help if the full payment stretches the budget too far.

First-time buyers should ask lenders about down payment assistance, FHA options, conventional first-time buyer programs, and whether buying points makes sense. They should also get pre-approved before shopping seriously. A strong pre-approval helps the buyer understand the real payment range and can make an offer more credible in a competitive Utah housing market.

Mortgage Lenders Utah Rates: How to Find the Best Offer

The phrase mortgage lenders Utah rates is important because lender pricing can vary more than buyers expect. One lender may have a lower rate, another may have lower fees, and another may provide better guidance for a complex borrower profile. The best mortgage rates Utah buyers qualify for usually come from comparing several offers on the same day using the same loan amount, down payment, credit profile, and loan term.

To find the best mortgage rates, request loan estimates from at least three lenders. Compare the interest rate, APR, points, origination charges, lender credits, estimated cash to close, and monthly payment. Ask each lender whether the rate is locked, how long the lock lasts, and what happens if rates move before closing. A borrower should also ask about service quality, closing speed, and communication because the cheapest quote is not always the best experience.

The best mortgage lenders in Utah are the lenders that combine competitive pricing with clear explanations and reliable execution. A buyer should feel comfortable asking questions and should understand why a specific loan is being recommended.

Final Takeaway on Current Mortgage Rates Utah

Current mortgage rates Utah buyers see online are useful, but they are only the beginning of the decision. The better question is whether the loan fits the buyer’s budget, timeline, and long-term financial goals. By comparing APR, loan type, lender fees, and monthly payment, Utah buyers can make a smarter decision and avoid choosing a mortgage based only on the lowest advertised number.

Whether you are comparing home loan rates Utah for a first purchase, checking best mortgage lenders in Utah, reviewing mortgage rates Salt Lake City, or deciding whether to refinance, the process should be the same: gather multiple quotes, compare the same loan terms side by side, and choose the mortgage that gives you the best total value.

Separate Image Submission Files

| File name | Placement | Alt text | Compressed size |

| current-mortgage-rates-utah-guide.jpg | Hero image at top of article | Utah home and mountain graphic illustrating current mortgage rates Utah and local home loan rate comparisons. | 25.0 KB |

| utah-mortgage-rates-30-year-fixed-vs-15-year.jpg | After 30-year vs 15-year section | Side-by-side graphic comparing Utah mortgage rates 30 year fixed with current 15 year mortgage rates in Utah. | 33.5 KB |

| compare-mortgage-rates-utah-lenders-checklist.jpg | Near lender comparison section | Checklist graphic showing how to compare mortgage rates Utah and evaluate the best mortgage lenders in Utah. | 35.3 KB |

Source URLs Used for Research

- Bankrate: https://www.bankrate.com/mortgages/mortgage-rates/

- NerdWallet: https://www.nerdwallet.com/mortgages/mortgage-rates

- Freddie Mac PMMS: https://www.freddiemac.com/pmms

- Mortgage News Daily: https://www.mortgagenewsdaily.com/mortgage-rates

- Mortgage Rate Utah: https://www.mortgagerateutah.com/