If you are buying your first home, one of the biggest questions you may have is: Should I lock my mortgage rate in Utah? It is a smart question because mortgage rates can change daily, and even a small change in your interest rate can affect your monthly payment. For many buyers, the decision to lock a rate can feel stressful because no one wants to lock too early and miss a lower rate, but no one wants to wait too long and watch rates rise.

A mortgage rate lock is an agreement with your lender that locks in your interest rate for a specific period while your loan moves toward closing. In simple terms, it protects you from rate increases during the home-buying process. This is especially important for Utah first-time buyers who are trying to stay within a specific monthly budget.

Mortgage Rates Today: Why Timing Matters

Mortgage rates today are important because they give buyers a general idea of the current market. However, the rate you see online may not be the exact rate you qualify for. Your personal mortgage rate depends on your credit score, income, debt, loan type, down payment, and the property you are buying.

That is why it is helpful to follow current mortgage rates, but it is even more important to get a personalized quote from a lender. Online rate tables can be a good starting point, but they do not always include the full picture, including lender fees, discount points, mortgage insurance, and closing costs.

Current Mortgage Rates and Utah Buyer Affordability

Current mortgage rates matter because they directly affect affordability. When rates increase, your monthly payment can rise, even if the home price stays the same. When rates decrease, your buying power may improve. This is why many first-time buyers check home loan interest rates before deciding when to make an offer or lock a rate.

For Utah buyers, affordability is especially important because home prices in many areas can already feel high. A small rate change may be the difference between a payment that feels manageable and one that stretches your budget too far. Before locking, buyers should look at the full payment, not just the interest rate.

Best Mortgage Rates: What Buyers Should Really Compare

Finding the best mortgage rates does not always mean choosing the lowest advertised number. A lender may offer a low rate but charge higher fees or points. Another lender may offer a slightly higher rate with lower upfront costs. The better deal depends on your situation, how long you plan to stay in the home, and how much cash you want to bring to closing.If you want to compare mortgage rates in Utah, ask each lender for the same type of quote. Compare the interest rate, APR, closing costs, loan term, and whether the quote includes points. This makes it easier to understand which offer is actually better.

Home Loan Rates and Rate Locks Explained

Home loan rates can rise or fall with the broader economy. Inflation, employment data, bond markets, and expectations about future Federal Reserve decisions can all influence rates. Because of this, rates may change from one day to the next.

A rate lock gives buyers protection. If you lock your rate and rates rise before closing, your locked rate usually stays the same. If rates fall, you may not automatically get the lower rate unless your lender offers a float-down option. This is why it is important to ask your lender what happens if rates drop after you lock.

Utah Mortgage Rates for First-Time Home Buyers

Utah mortgage rates for first-time home buyers can vary depending on the loan program. Some buyers may qualify for conventional financing, while others may use government-backed programs. First-time buyers should also research first-time homebuyer programs, as some may help with down payment or closing cost challenges.

If you are looking for the best Utah mortgage rates for first-time buyers, remember that the best option is not always the lowest rate by itself. The best option is usually the loan that gives you a monthly payment you can afford, reasonable closing costs, and a structure that fits your long-term goals.

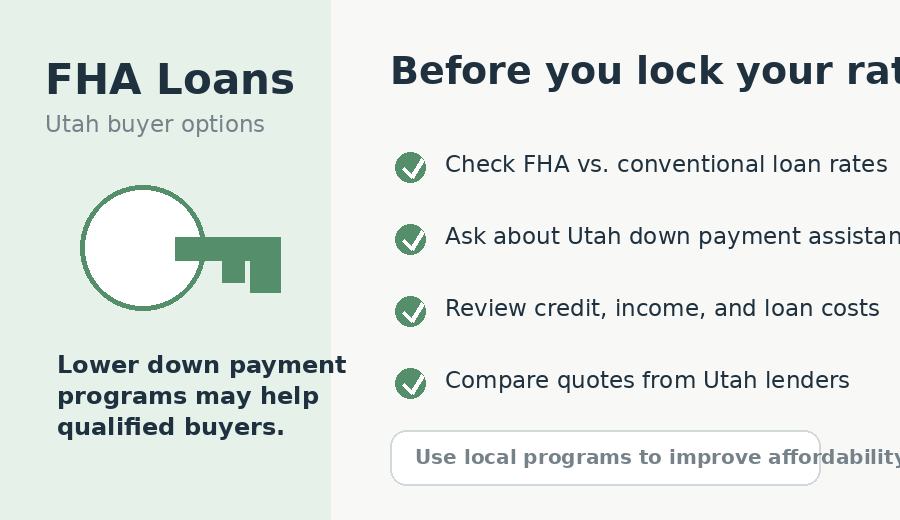

FHA Loans vs. Conventional Loan Rates in Utah

Many first-time buyers consider FHA loans because they can be more flexible for borrowers with lower credit scores or smaller down payments. If you are researching FHA mortgage rates in Utah, make sure you also understand mortgage insurance and other FHA loan costs.

Conventional loans may be a good option for buyers with stronger credit, more savings, or a larger down payment. When comparing conventional loan rates in Utah with FHA options, do not only compare the rate. Compare the total monthly payment, cash needed to close, mortgage insurance, and long-term cost of the loan.

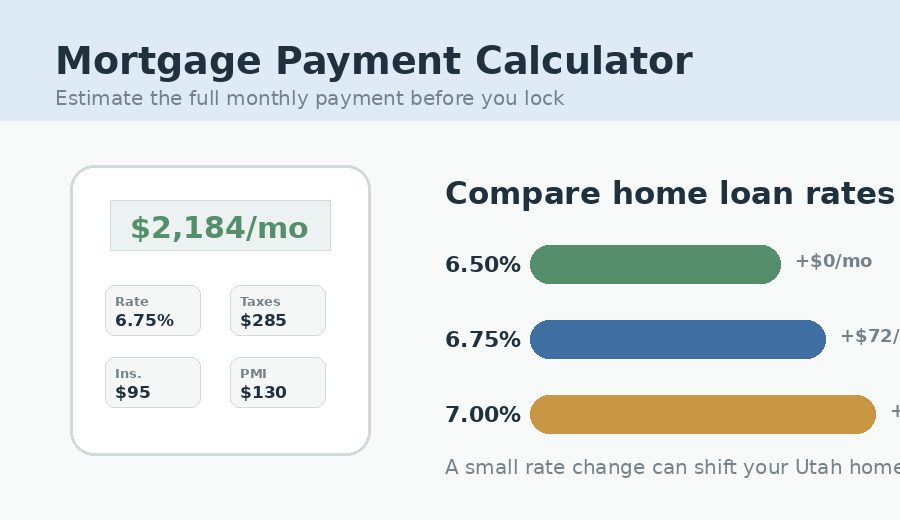

Mortgage Payment Calculator: Check the Payment Before You Lock

A mortgage payment calculator is one of the most useful tools before locking your rate. It helps you estimate your monthly payment based on loan amount, interest rate, taxes, insurance, and other costs. This matters because a rate may look good, but the full payment still needs to fit your budget.

Buyers should also look at the average mortgage rate in Utah and Utah home loan interest rates today to understand the local market. These searches can help you see where rates are generally moving, but your final rate will depend on your personal financial profile and the lender you choose.

Mortgage Pre-Approval Before Locking Your Rate

Getting a mortgage pre-approval is one of the first steps before locking in a rate. Pre-approval helps you understand how much home you may be able to afford and what loan programs could fit your situation. It also shows sellers that you are a serious buyer. Once you are pre-approved and under contract, your lender can give you a more accurate mortgage quote. This is usually when the rate lock conversation becomes more important. If your closing date is set and the payment works for your budget, locking may be a smart move.

How to Get the Lowest Mortgage Rate in Utah

If you are wondering how to get the lowest mortgage rate in Utah, start with the factors you can control. A higher credit score, lower debt-to-income ratio, larger down payment, and stable income can all improve your chances of qualifying for a better rate. It can also help to shop around. You may search for a mortgage broker near me, contact a credit union, compare online lenders, or work with a local Utah mortgage professional. Before you apply for a mortgage, gather your documents, review your credit, and understand your budget.

Utah Mortgage Down Payment Assistance and First-Time Buyer Programs

Some buyers delay purchasing because they are worried about the down payment. That is why it is worth researching Utah mortgage down payment assistance and first-time homebuyer loan programs. These programs may help qualified buyers reduce the upfront cash needed to purchase a home.

Buyers may also want to review Utah housing loan rates if they are considering housing assistance programs. These programs can be helpful, but they may have specific requirements, income limits, or property rules. A lender who understands Utah programs can explain whether you qualify and how the program affects your loan.

Should You Lock or Wait?

The answer depends on your timing and comfort level. If you are under contract, have compared lender quotes, understand your payment, and feel comfortable with the numbers, locking your rate may be the safer choice. It protects you from the risk that rates will increase before closing.

Waiting may make sense if you are still shopping for homes, have not chosen a lender, or believe rates may improve. However, trying to perfectly time mortgage rate trends in Utah can be risky. Rates can move quickly, and waiting too long can create stress if your payment suddenly increases.

Final Takeaway

For most first-time buyers, the best time to lock a mortgage rate is after you are pre-approved, under contract, and comfortable with the monthly payment. Checking mortgage rates today and following current mortgage rates can help you understand the market, but the final decision should be based on your personal loan quote, budget, and closing timeline.

Before locking your rate, take time to compare mortgage rates in Utah, use a mortgage payment calculator, and speak with a lender who understands Utah buyers. A mortgage rate lock is not about guessing the market perfectly. It is about protecting a payment that works for you.