Purchasing a home is one of the largest financial commitments most people will ever make. Before you begin shopping for homes or speaking with a lender, it’s important to understand exactly what your monthly mortgage payment may look like. A Mortgage payment calculator is one of the most valuable tools available because it helps estimate your monthly housing costs based on factors like your loan amount, interest rate, down payment, loan term, taxes, insurance, and mortgage insurance.

While many online calculators provide a quick estimate, understanding what goes into your payment can help you make better financial decisions. Whether you’re buying your first home, refinancing your current mortgage, or purchasing a second property, using the right mortgage calculator allows you to compare loan options, evaluate affordability, and plan for the future.

At Mortgage Rate Utah, our goal is to educate borrowers while helping them find competitive mortgage solutions. This guide explains how different mortgage calculators work, what information they provide, and how they can help you choose the financing option that best fits your financial goals.

Home Loan Monthly Payment Calculator – Estimate Your Monthly Costs

A Home loan monthly payment calculator helps estimate your total monthly housing expense before you begin shopping for homes. Rather than focusing only on the home’s purchase price, this calculator considers multiple financial factors that determine your monthly payment.

Most mortgage payments include:

- Principal

- Interest

- Property Taxes

- Homeowners Insurance

- Mortgage Insurance (PMI), when applicable

- HOA Fees (if applicable)

Because property taxes and insurance vary from one property to another, using a Mortgage payment calculator with taxes and insurance provides a much more realistic estimate than calculating principal and interest alone.

Some buyers also prefer using a House payment calculator with taxes, especially when comparing homes in different counties or school districts where tax rates may differ significantly.

Likewise, a Mortgage calculator with property taxes allows borrowers to understand how local tax rates affect long-term affordability before making an offer on a home.

Understanding your complete monthly payment helps eliminate surprises during the mortgage process and allows you to create a realistic household budget.

Home Loan Principal and Interest Calculator – Understand How Your Mortgage Works

Your monthly mortgage payment is divided between principal and interest. During the first several years of your loan, a larger percentage of each payment goes toward interest. As your loan balance decreases, more of your payment begins reducing the principal balance.

A Home loan principal and interest calculator illustrates this breakdown so borrowers can understand exactly where their money is going each month.

Many homebuyers also benefit from using a Housing loan amortization calculator, which generates a complete amortization schedule showing:

- Remaining loan balance

- Principal paid each month

- Interest paid each month

- Total interest over the life of the loan

Viewing your amortization schedule helps borrowers understand how making larger payments or refinancing can affect both the length and cost of their mortgage.

Instead of thinking about your mortgage as one large debt, an amortization schedule demonstrates how every payment builds equity in your home.

Housing Loan Affordability Calculator – Determine How Much House You Can Afford

One of the biggest mistakes first-time buyers make is shopping for homes before determining what comfortably fits within their budget.

A Housing loan affordability calculator estimates how much home you may qualify for based on several important financial factors, including:

- Annual household income

- Existing monthly debt

- Available down payment

- Loan term

- Estimated interest rate

Lenders also evaluate your debt-to-income ratio during the mortgage approval process. A Debt-to-Income Ratio Calculator allows borrowers to estimate whether they fall within common lending guidelines before applying.

Using these affordability tools before beginning your home search helps prevent disappointment while narrowing your search to homes that fit comfortably within your financial goals.

Remember that qualifying for a certain loan amount doesn’t necessarily mean it’s the right financial decision. Purchasing below your maximum budget often provides greater flexibility for future expenses and unexpected costs.

FHA Mortgage Payment Calculator – Estimate FHA Loan Payments

FHA loans remain one of the most popular financing options for first-time homebuyers because they offer flexible credit requirements and lower down payment options.

An FHA mortgage payment calculator estimates monthly payments while accounting for FHA-specific costs that conventional loan calculators often overlook.

For even greater accuracy, borrowers should use an FHA calculator with PMI and taxes, which includes:

- FHA mortgage insurance premiums

- Property taxes

- Homeowners insurance

- Estimated monthly payment

Many buyers also underestimate the amount of cash needed at closing. An FHA down payment and closing cost calculator estimates upfront expenses such as your required down payment, lender fees, prepaid taxes, homeowners insurance, and other closing costs.

Understanding these expenses early helps buyers prepare financially and avoid delays during the closing process.

While FHA loans offer significant advantages for many borrowers, comparing FHA financing with conventional loan options is always recommended before making a final decision.

15 Year Mortgage Payment Calculator – Compare Short- and Long-Term Loans

One of the biggest decisions borrowers make is choosing the length of their mortgage. While a 30-year mortgage is the most common option, a shorter loan term can save you a significant amount of money over time.

A 15 year mortgage payment calculator allows you to compare monthly payments and total interest costs between a 15-year and 30-year mortgage. Although monthly payments are higher with a 15-year loan, you’ll typically build equity faster and pay substantially less interest over the life of the loan.

If you’re leaning toward a traditional mortgage, a 30 year mortgage rates calculator can help you compare different interest rates and determine how rate changes affect your monthly payment. Even a small difference in your interest rate can translate into thousands of dollars in savings over the life of your mortgage.

When comparing loan terms, consider your monthly budget, long-term financial goals, and how quickly you’d like to build equity in your home.

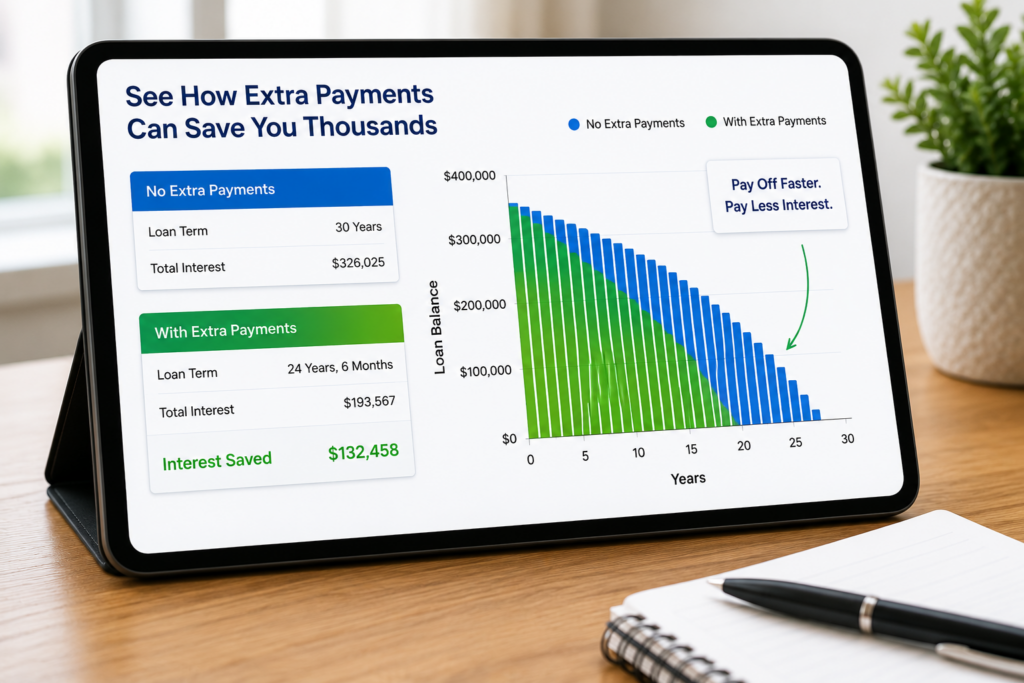

Mortgage Calculator with Extra Payments – Save Thousands in Interest

One of the easiest ways to reduce the overall cost of your mortgage is by making additional principal payments whenever possible. Even an extra $50 or $100 per month can shorten your loan term and reduce the total interest you pay.

A Mortgage calculator with extra payments allows you to see exactly how much time and money you could save by paying more than your required monthly payment.

Depending on your repayment strategy, you may also find these calculators helpful:

- Mortgage loan calculator with extra payments

- Mortgage payment calculator with extra payments

- Mortgage amortization calculator with extra payments

- Payment calculator with extra payments

Each calculator demonstrates how additional principal payments reduce your outstanding balance faster than making only the required payment.

For homeowners looking for even more detailed projections, a Mortgage calculator with extra payments and amortization provides an updated amortization schedule that shows how each extra payment affects your remaining loan balance and future interest costs.

If you plan to apply bonuses, tax refunds, or inheritances toward your mortgage, a Mortgage calculator with extra payments and lump sum can estimate the impact of one-time principal payments. Many homeowners are surprised to learn that a few strategically timed lump-sum payments can eliminate years from their mortgage.

Biweekly Mortgage Payment Calculator – Pay Off Your Loan Faster

Another popular strategy for paying off a mortgage sooner is making biweekly payments instead of monthly payments.

A Biweekly mortgage payment calculator shows how paying half of your monthly mortgage payment every two weeks results in 26 half-payments each year, which equals 13 full monthly payments instead of 12.

That one additional payment each year can significantly reduce your loan balance and decrease the total interest paid over the life of your mortgage—all without making large additional monthly payments.

This strategy works especially well for borrowers who are paid every two weeks and want to align their mortgage payments with their paycheck schedule.

Mortgage Calculator Based on Monthly Payment – Shop with Confidence

Many buyers begin their home search by looking at listing prices, but a smarter approach is starting with your monthly budget.

A Mortgage calculator based on monthly payment estimates the maximum home price you can comfortably afford based on the monthly payment you want to make.

This approach helps borrowers:

- Stay within budget

- Compare different down payment amounts

- Evaluate multiple interest rate scenarios

- Avoid becoming “house poor”

Planning your purchase around a comfortable monthly payment helps ensure long-term financial stability and reduces stress after closing.

Specialized Mortgage Calculators for Unique Financing Needs

Some homebuyers have financing situations that require more specialized planning tools.

A 40 year interest only mortgage calculator estimates payments for borrowers considering alternative mortgage products with extended repayment periods or temporary interest-only payments. While these loans may reduce initial monthly payments, it’s important to understand the long-term financial implications before selecting this type of financing.

If you’re purchasing a vacation home or investment property, a Second home mortgage qualification calculator helps estimate qualification requirements based on your current income, existing mortgage obligations, and projected housing expenses.

Homebuyers in eligible markets may also benefit from using a Help to buy mortgage repayment calculator to estimate monthly payments associated with homeownership assistance programs. These calculators help borrowers understand repayment obligations and determine whether assistance programs align with their financial goals.

Why Work with Mortgage Rate Utah?

While online calculators provide excellent estimates, they can’t replace personalized guidance from an experienced mortgage professional.

Every borrower has unique financial circumstances, and factors such as your credit score, debt-to-income ratio, employment history, loan type, and current market conditions all influence the financing options available to you.

At Mortgage Rate Utah, we help borrowers:

- Compare loan programs

- Understand closing costs

- Evaluate refinancing opportunities

- Estimate monthly mortgage payments

- Find competitive mortgage rates

- Choose financing that supports their long-term financial goals

Whether you’re purchasing your first home, upgrading to a larger property, refinancing, or investing in real estate, our experienced team is here to help you navigate every step of the mortgage process.

Frequently Asked Questions

What is included in a mortgage payment?

A typical mortgage payment includes principal, interest, property taxes, homeowners insurance, and mortgage insurance (PMI) when required.

Why should I use a mortgage payment calculator?

A mortgage payment calculator provides a realistic estimate of your monthly housing costs before applying for a loan, allowing you to compare financing options and budget more effectively.

Can making extra payments really save money?

Yes. Making additional principal payments can shorten your loan term and reduce the amount of interest paid over the life of your mortgage.

Should I choose a 15-year or 30-year mortgage?

A 15-year mortgage generally offers lower total interest costs and faster equity growth, while a 30-year mortgage provides lower monthly payments and greater financial flexibility.

How accurate are online mortgage calculators?

Mortgage calculators provide excellent estimates, but your final payment depends on factors such as your interest rate, taxes, insurance premiums, loan program, and lender fees. Speaking with a mortgage professional can provide the most accurate estimate.