Before shopping for a home, it helps to know how much of your income is already committed to debt. Your debt to income ratio compares required monthly debt payments with gross monthly income, or income before taxes and other deductions. Mortgage lenders use this percentage as one part of a broader underwriting review. A lower ratio generally leaves more room for a new housing payment, while a higher ratio may signal that your monthly budget is already stretched. Understanding the debt to income ratio for mortgage financing can help you set a realistic price range, avoid surprises during preapproval, and decide whether paying down debt should come before making an offer.

What Is a Debt to Income Ratio for Mortgage Approval?

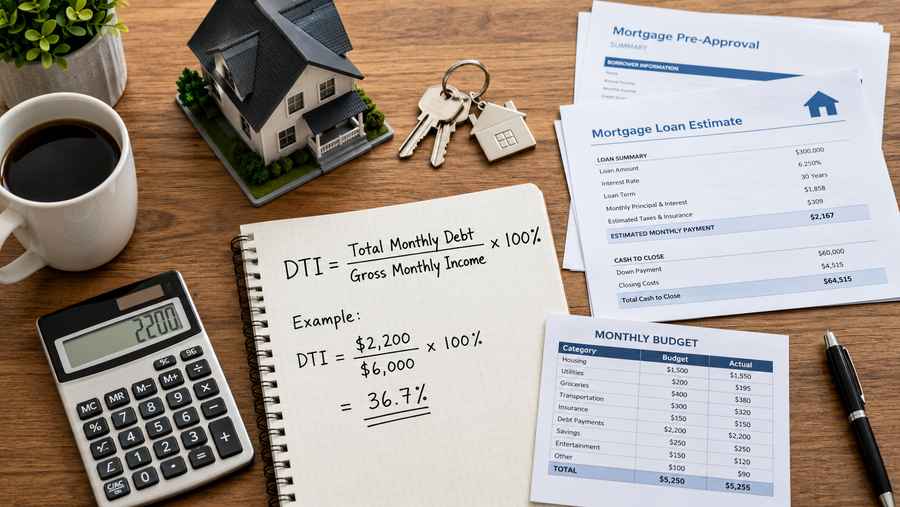

The debt to income ratio for mortgage approval is calculated by dividing your recurring monthly debt obligations by your gross monthly income and multiplying the result by 100. For example, suppose your monthly debt payments total $2,100 and your gross monthly income is $6,000. Dividing $2,100 by $6,000 produces 0.35, so your DTI is 35%. The Consumer Financial Protection Bureau explains that lenders use DTI to evaluate a borrower’s ability to manage monthly payments, while also noting that different loan products and lenders may apply different limits.

You may see several similar phrases online, including mortgage debt to income ratio, debt ratio for mortgage, dti ratio for mortgage, and debt to income for mortgage. These phrases usually describe the same basic comparison: how much monthly income is committed to debt after accounting for the proposed housing expense. DTI is important, but it does not operate alone. Lenders may also evaluate credit history, income stability, available cash, down payment, property type, and the specific loan program.

How to Calculate Debt to Income Ratio for Mortgage

To calculate debt to income ratio for mortgage purposes, begin by listing recurring obligations that are typically reviewed by lenders. These can include the proposed mortgage payment, property taxes, homeowners insurance, association dues, auto loans, student loans, minimum credit card payments, installment loans, child support, and other required debt payments. Then total the gross monthly income that can be documented and used for qualification. Divide the monthly debt total by the qualifying gross income and convert the answer to a percentage.

For a quick personal estimate, ask: “How can I calculate my debt to income ratio before speaking with a lender?” Gather the minimum required monthly payment for each debt rather than the outstanding balance. Next, estimate the full monthly housing payment, not merely principal and interest. A complete estimate may include taxes, insurance, mortgage insurance, and homeowners association dues. This gives you a more useful picture of your debt to income ratio for home loan planning and your likely debt to income ratio for buying a house.

The basic formula is straightforward: total recurring monthly debt payments divided by gross monthly income, multiplied by 100. Using a documented income of $7,500 per month and total monthly obligations of $2,625 results in a 35% dti ratio. Remember that a self-calculated estimate is not a loan decision. A lender may calculate income or certain debts differently based on documentation and underwriting rules.

Using a DTI Calculator Before Applying for a Mortgage

A calculator can make the first estimate faster. Whether you search for a dti calculator, debt to income calculator, mortgage debt to income ratio calculator, dti mortgage calculator, debt to income ratio mortgage calculator, or debt to income mortgage calculator, the underlying formula should remain the same. Enter gross monthly income, current monthly debt payments, and the estimated new housing payment. Review the result as a planning tool rather than a guarantee of approval.

Some buyers search for a debt to income ratio to buy a house calculator because they want to test different home prices or down payments. Others use a dti ratio calculator to compare scenarios such as paying off a car loan, reducing a credit card payment, or increasing the down payment. A useful calculator should let you separate the housing payment from other debts and should clearly explain which numbers belong in each field.

Use NerdWallet’s Mortgage Calculator to estimate a complete monthly housing payment before calculating DTI.

Front End Debt to Income Ratio vs. Total DTI

The front end debt to income ratio focuses only on housing expenses compared with gross monthly income. Depending on the loan and lender, housing expenses may include principal, interest, property taxes, homeowners insurance, mortgage insurance, and association dues. The total or back-end DTI includes the housing payment plus recurring obligations such as auto loans, student loans, minimum credit card payments, and other required debts.

This distinction matters because two applicants with the same income and housing payment can have very different overall debt loads. A borrower with no auto loan and low credit card payments may have more flexibility than a borrower with several large installment payments. When reviewing a good dti ratio, avoid treating one number as a universal cutoff. Lender standards, loan programs, compensating factors, and automated underwriting results can all affect the decision.

Review the Consumer Financial Protection Bureau’s explanation of DTI and its calculation method: What is a debt-to-income ratio?

FHA Debt to Income Ratio and Loan Guidelines

Borrowers often research the fha debt to income ratio because FHA-insured loans may be evaluated differently from conventional loans. A search for debt to income ratio for fha loan guidance should lead to a careful review of current lender and program requirements rather than a single number copied from an old article. FHA underwriting considers the complete application, and individual lenders may apply additional standards.

A debt to income ratio calculator fha search can still be useful for estimating the percentage, but the calculator cannot determine whether documented income is acceptable, how a particular debt will be counted, or whether other factors support approval. For this reason, buyers should use calculator results to prepare questions for a licensed mortgage professional. The result can identify whether paying down a balance, avoiding a new loan, or selecting a lower housing payment may strengthen the application.

For conventional-loan underwriting details, review Fannie Mae Debt-to-Income Ratios.

How to Improve Your DTI Ratio for Mortgage Approval

If your estimate is higher than expected, focus on changes that improve the monthly calculation. Paying off a debt entirely can remove its required payment, while paying down a revolving balance may reduce the minimum payment reported to the lender. Avoid taking on new installment debt shortly before applying. If overtime, commissions, bonuses, or self-employment income are part of the plan, ask a lender what documentation and history may be needed before assuming the income will count.

Also test the housing side of the equation. A lower purchase price, larger down payment, less expensive property-tax area, or lower homeowners insurance premium may reduce the projected housing payment. The best target is not simply the maximum DTI a lender might accept. A mortgage should leave enough room for utilities, maintenance, repairs, savings, health costs, and everyday spending that do not appear in the lender’s formula.

Before seeking preapproval, update the estimate using recent statements and realistic housing costs. Then review your credit reports, preserve cash for closing and reserves, and compare loan options.

Learn how mortgage preapproval works and which documents a lender may request in NerdWallet’s Mortgage Preapproval Guide.

Use DTI as a Planning Tool, Not the Entire Decision

Your DTI gives you a valuable snapshot of monthly debt pressure, but it does not measure every part of affordability. A buyer can satisfy a lender’s ratio and still feel uncomfortable after accounting for childcare, transportation, food, medical costs, home repairs, and savings goals. Use the calculation to create a sensible range, then build a complete household budget before choosing a mortgage payment.

In practical terms, understanding DTI helps you ask better questions and make better decisions. Calculate the ratio early, test multiple housing scenarios, verify the result with a lender, and leave room for the costs of owning a home. That approach makes the debt to income ratio for mortgage more than an approval statistic; it becomes a useful tool for buying a home you can afford over the long term.