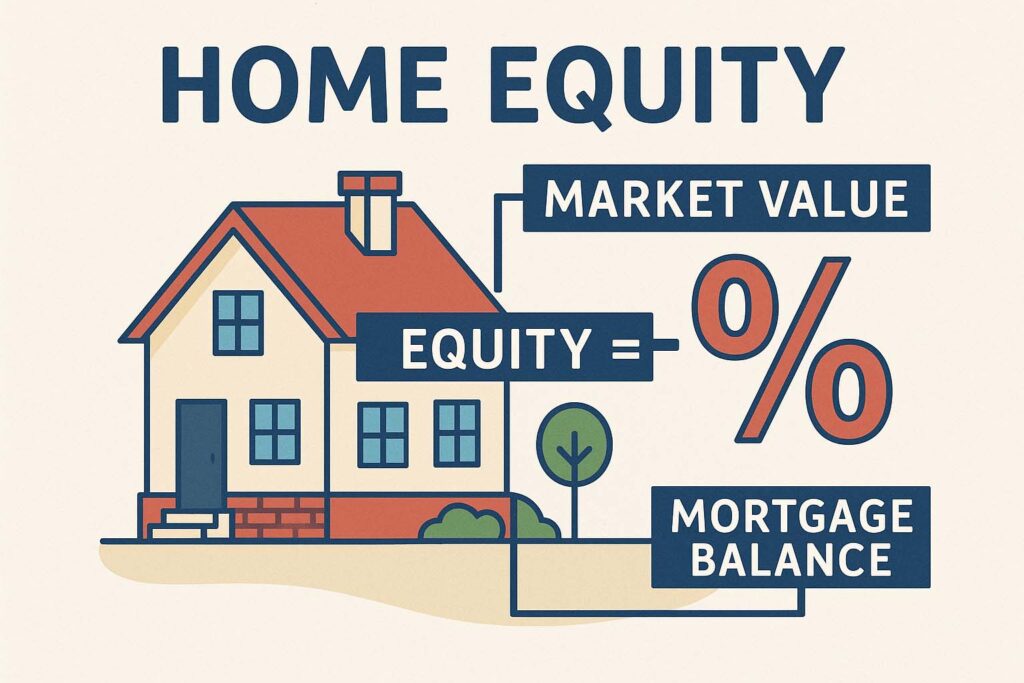

If you own a home in Utah, you may be sitting on a financial opportunity that you’re not aware of. Thanks to strong property appreciation across the Wasatch Front and beyond, many Utah homeowners have built up significant home equity—the difference between your home’s current market value and what you still owe on your mortgage.

Leveraging that equity through a home equity loan, a home equity line of credit (HELOC), or even a fixed-rate HELOC can be a smart way to fund major expenses. Whether your goal is remodeling your Salt Lake bungalow, consolidating high-interest debts, or covering college tuition at Utah State, understanding how these products work is essential.

What is a HELOC?

A HELOC, short for Home Equity Line of Credit, provides Utah homeowners with flexible access to their equity. It’s a revolving line of credit secured by your house—almost like a credit card, but typically with much lower HELOCS because it’s tied to your home. Unlike a traditional equity loan, which provides a lump sum upfront, a HELOC allows you to borrow as needed, up to a set limit.

Currently, HELOCs in Utah can be very competitive, especially compared to unsecured personal loans or credit cards. That’s why many locals actively shop around for the best HELOCS or look up HELOCS today to secure the most favorable deal.

How is a Home Equity Loan Different?

A home equity loan is often referred to as a second mortgage. This type of equity loan provides you with a one-time lump sum, which you repay in fixed monthly installments. Many Utah homeowners like the predictability of home equity loan rates, which are usually fixed for the entire term.

If you’re planning a one-time significant expense—like building out a basement apartment in Provo or paying off high-interest debts—a home equity loan might be the right fit. Some Utahns even explore hybrid products, such as a fixed-rate HELOC, which combines the flexibility of a line of credit with the security of stable payments on a portion of your balance.

Comparing Rates and Lenders in Utah

Not all lenders are the same, and neither are their offers. Utah homeowners often start by comparing products from national players, such as Bank of America HELOCs, Wells Fargo home equity loans, or Rocket Mortgage HELOCs. But many also consider local credit unions and regional banks that specialize in Utah real estate.

It’s important to remember: even a slight difference in interest rates can save thousands over the life of your loan. That’s why phrases like best HELOC lenders, best home equity loans, and best home equity line of credit are so commonly searched in Utah.

Don’t stop at just comparing rates. Look carefully at fees, draw periods, repayment schedules, and how lenders rank in customer service. The correct option isn’t always the one with the absolute lowest advertised rate—it’s the one that best fits your financial goals.

Popular Uses for Home Equity Loans and HELOCs in Utah

Utah homeowners often use home equity loans and HELOCS for smart investments or essential needs. Here are some of the most common reasons:

- Home renovations: From adding an ADU in Ogden to updating a kitchen in Sandy, improvements can boost your home’s value and quality of life.

- Debt consolidation: Paying off high-interest credit cards with lower HELOC rates or home equity loan rates can save you big.

- Education expenses: Funding tuition at BYU, UVU, or for kids’ LDS missions is a common local goal.

- Unexpected costs: Covering medical bills or family emergencies without touching retirement funds.

Because a HELOC acts like a line of credit, it’s beneficial for costs that come in phases, like a multi-stage remodel or landscaping overhaul.

Managing Risks

Keep in mind: any home equity loan, heloc loan, or equity line of credit is secured by your house. That means if you can’t keep up with payments, foreclosure becomes a risk. Financial planners in Utah generally advise using home equity for investments that build value or reduce costly interest elsewhere, not for everyday spending.

Tips for Finding the Right Utah HELOC or Home Equity Loan

If you’re starting your search here in Utah, try these smart steps:

- Compare multiple lenders: Consider both large national banks and local Utah institutions or credit unions.

- Look beyond rates: Pay attention to origination fees, annual costs, and any early payoff penalties.

- Consider your future plans: If you might sell your Utah home or refinance soon, select options with minimal penalties.

- Check reviews, especially for a home equity line of credit, as you may be managing it for years.

Bottom Line for Utah Homeowners

Whether you’re leaning toward a heloc loan, a simple home equity loan, or just want to find the best heloc lenders in Utah, there’s a wide range of choices right now. Using tools to compare best heloc rates, current heloc rates, and heloc interest rates can help ensure you make a confident, well-informed decision.

At the end of the day, your Utah home is likely your biggest investment. Using it to secure financing through a home equity line of credit or home equity loan strategy can be a powerful move—just be sure to weigh your options, read the fine print, and consider speaking with a local financial advisor who understands the Utah market.