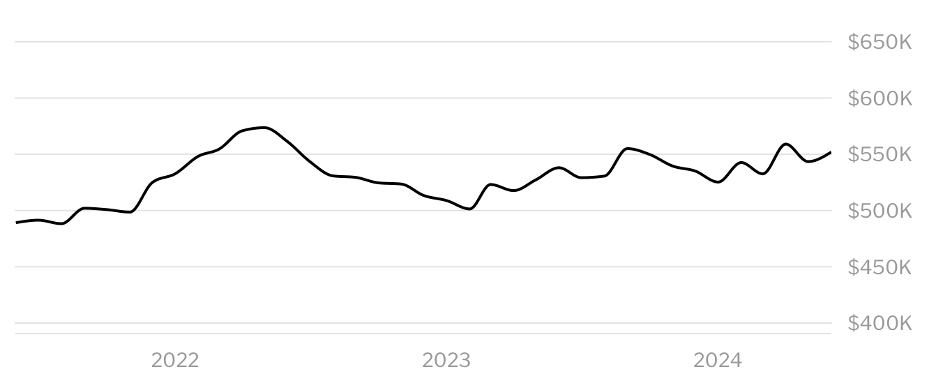

The median home sales price in May 2024 has increased in the past 3 months to $545,900. That’s up 3.1% and $16,300 higher than May 2023 of last year. That is higher than the national median home sales price of $439,716.

How many houses are available in Utah?

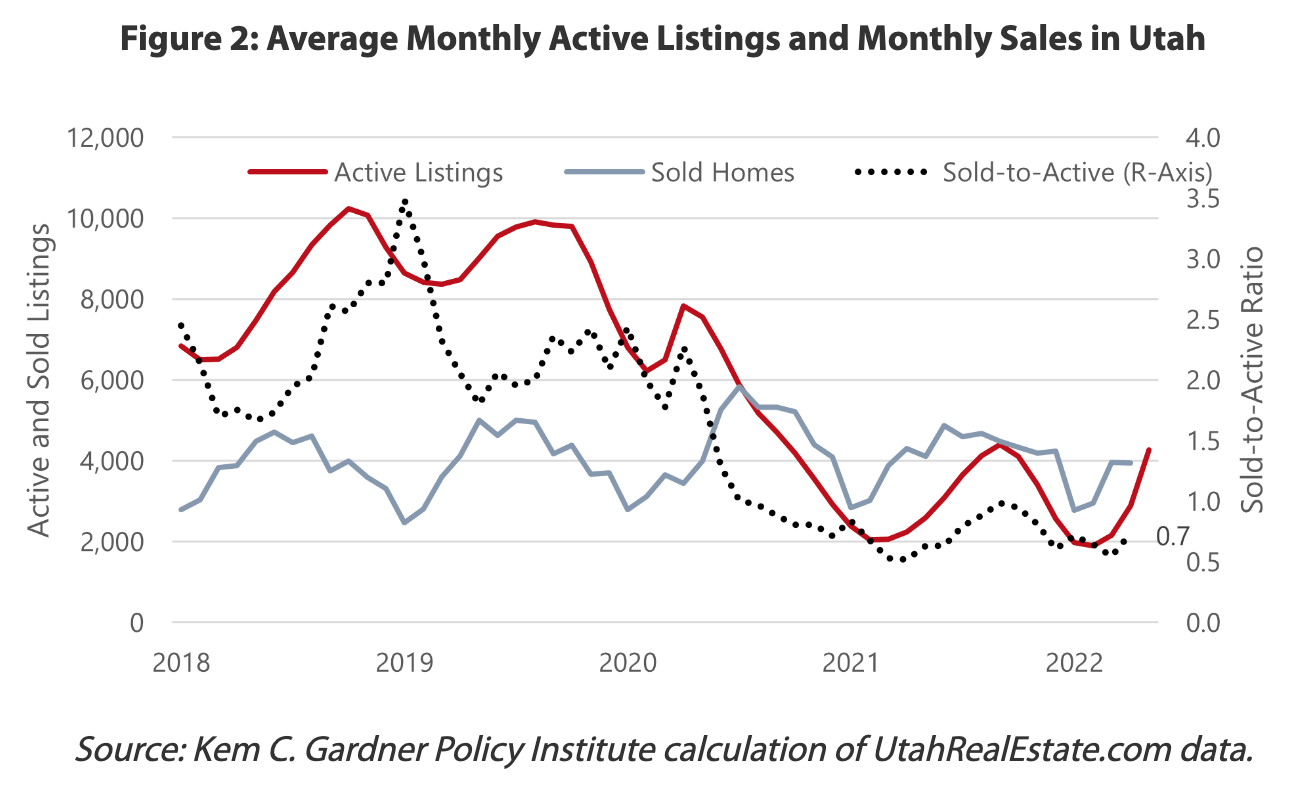

The real estate market in Utah had 9,935 homes for sale in May 2024 and is up from 9004 homes for sale the month prior and up from 8,286 homes in May 2023 which is 19.9% up.

How many houses are sold in Utah?

There were 3468 homes sold in May 2024, trending up from 3116 homes sold a year ago. This is up 352 homes and 11.3% since May 2023.

How long does it takes to sell a house in Utah?

Homes in Utah are staying on the market for 35 days. That’s 4 days slower than the median in May 2023, which is 12.9%. This shows that the market is less competitive today.

Utah Housing Market in 2025

Impact of Mortgage Rates

Our forecast for existing home sales through 2025 has been modestly revised downward due to expectations of higher mortgage rates. Rates are expected to remain close to 7% through the end of the year before potentially trending downward in 2025.

Yearly Comparisons

In 2023, the growth rate was 6.6%, and for 2024, we forecast a 4.8% increase. By 2025, the growth rate will dip to 1.5%, well below the long-run average of 3-5% annual increases.

Comparing January and May Forecasts

In January, a lot of real estate professionals predicted a 3.2% increase in home prices for 2024. By May, this forecast was revised to 4.8%. For 2025, the January forecast was a 3% increase, which was later adjusted to 1.5% in May.

Historical Context

The average number of existing home sales per year since 1989 is just over 5 million. The 2025 forecast of 4.5 million is about 500,000 less than this historical norm.

Purchasing a home is an accomplishment that everyone hopes to look forward to in their life. Ensuring that you secure the right mortgage for you is crucial to be comfortable financially while enjoying your new home. Trying to sort and calculate through the numerous mortgage banks in Utah can be a confusing and intimidating experience. However, if you approach it by analyzing your options and informing yourself the best you can, you will hopefully be able to make a decision that benefits you and your home.

Assess Your Financial Situation

When deciding which mortgage bank you should choose, you should first assess your own financial situation. Take time to understand your credit score and how that will affect the interest rate and terms you will be offered by different Utahbanks. Double check your credit score history for any mistakes that could have been made. After doing so, work to calculate your debt-to-income ratio. This will give you a good idea of how much you can afford to borrow. For reference, many banks prefer a debt-income ratio of 43% or lower.

Research Mortgage Types: what makes the most sense for you?

Once you analyze your financial situation, it is important to educate yourself on the different mortgage types available and which one will work best for you. Most of these mortgages will have both advantages and disadvantages which is why it is needed to weigh all your options before coming to a decision. Here is a brief overview of the most common types of mortgages that you may encounter.

Fixed-Rate Mortgages: You can expect these loans to have a consistent interest rate throughout the term. This is often preferred as it provides stability in monthly payments.

Adjustable-Rate Mortgages (ARMs): These loans normally start with a lower fixed rate for the first couple of years. Afterwards, you will see the rate adjusted based on the market’s conditions.

FHA Loans: This type of loan is provided by The Federal Housing Administration. These loans are usually preferred for first-time homebuyers that have a lower credit score.

VA Loans: These loans are available to veterans and active military members. They offer loans at a competitive rate and require no down payment.

Jumbo Loans: This is the loan that you would want for a property that exceeds the conforming loan limit. Jumbo loans are a great option for people who need them, but along with the larger lump sum of money comes higher interest rates and stricter requirements.

Compare Mortgage Rates and Terms

Having a reasonable interest rate is a vital detail to ensure that you will be comfortable with the overall cost of your mortgage. To find the best rate it is important that you compare the offers and terms from multiple institutions. Reach out to banks for a personalized mortgage quote and compare the Annual Percentage Rate (includes the interest rate and additional fees) as that will give you the best overall view of the loan. After analyzing the interest rates, reading and evaluating the loans terms and conditions is just as important. Consider factors such as:

Loan Fees: This can include origination fees, closing costs, and other charges that can unexpectedly add up. Ensure you understand all costs associated with the bank.

Prepayment Penalties: Some banks will have loans penalties for paying off your mortgage early. This is something you want to make yourself aware of, especially if you plan to sell or refinance before the end of the loan. Try to avoid these penalties if possible.

Flexibility: When a bank offers flexibility in payment scheduling and rate locks it could be end of being very helpful in the future. It is worth checking out each bank’s options.

Do your research on who you are trusting your money with

After combing through the rates and terms of each bank, it is important to ensure that the institution you are going through will be reliable and safe with your money. Reading through other people’s reviews from their personal experiences is a great way to understand more about the mortgage bank’s reputation and how your experience with them will likely go. Look into banks with a strong reputation for customer satisfaction as you will more likely have a smooth experience with their institution.

Utilize Utah’s financial resources

Once you have completed your research into your own financial capability and into the banks that you are considering it is always a good idea to get a professional opinion as well. Utah has many different resources that can help guide homebuyers. For first-time homebuyers, The Utah Housing Corporation offers programs that assist with down payments and finding competitive mortgage rates. Local credit unions and banks also offer services tailored to serve Utah homebuyers.

How to Find Your Ideal Utah Mortgage Bank

For more information on The Utah Housing Corporation click here

For more information on banks and credit unions in Utah click here

To see our recommendations for Utah mortgage banks click here

Finding the right mortgage lender is crucial if you’re looking to buy a home in Utah. With a booming real estate market and various options available, knowing where to start can be challenging. To help you navigate this important decision, here are our top five mortgage banks and brokers in Utah known for their excellent service, competitive mortgage rates, and local expertise.

1. SecurityNational Mortgage Company

SecurityNational Mortgage Company, headquartered in Salt Lake City, Utah, stands out for its comprehensive and innovative mortgage solutions. Founded in 1993, SecurityNational offers a wide range of loans designed to meet the diverse needs of Utah homeowners. Their product offerings include conventional, FHA, VA, USDA, and jumbo loans. Additionally, they provide specialized programs for first-time homebuyers, offering lower down payments and flexible credit requirements to make homeownership more accessible.

Note: Some customers have reported that the processing time can be longer than expected, which could be an issue if you need a quick closing.

Intercap Lending, based in Orem, Utah, is another leading mortgage company in Utah. Known for their streamlined processes and quick turnaround times, Intercap Lending makes the mortgage process straightforward and stress-free. They offer competitive mortgage rates and a variety of loan products, including fixed-rate and adjustable-rate mortgages, FHA and VA loans, and refinancing options. Intercap Lending’s commitment to customer satisfaction and their deep knowledge of the Utah housing market make them a top choice for many homebuyers.

Note: While they offer quick turnaround times, some clients have mentioned that communication can be inconsistent, leading to potential misunderstandings during the process.

Altius Mortgage Group, located in South Jordan, Utah, is a highly regarded mortgage broker that offers a personalized approach to home financing. As a broker, Altius works with multiple banks to find the best loan options for their clients. This flexibility allows them to offer highly competitive mortgage interest rates and a wide range of loan products.

Note: As a broker, their rates and terms are subject to the lenders they partner with, which can sometimes result in less control over the final loan conditions.

Guild Mortgage, with several branches throughout Utah, has been providing home financing solutions since 1960. Known for their strong commitment to customer service, Guild Mortgage offers a variety of loan products tailored to meet the needs of Utah homeowners. They provide conventional loans, FHA and VA loans, jumbo loans, and refinancing options. Guild Mortgage’s knowledgeable loan officers are well-versed in the local market conditions and work closely with clients to find the best mortgage solutions to fit their needs.

Note: Some borrowers have experienced higher closing costs compared to other lenders, which could affect your overall budget.

Citywide Home Loans, headquartered in Sandy, Utah, is a full-service mortgage lender with a strong presence in the state. They, like their competitors, offer a comprehensive range of loan products, including conventional loans, FHA and VA loans, USDA loans, and jumbo loans. Citywide Home Loans is highly regarded by many Utah homeowners for their exceptional customer service and competitive mortgage rates.

Note: Despite their excellent service, some customers have noted that their application process can be more documentation-heavy and rigorous than other lenders.

When selecting a mortgage lender, it’s important to consider factors such as mortgage interest rates, loan options, customer service, and the lender’s knowledge of the local market. These five mortgage companies in Utah have established themselves as leaders in the industry, offering excellent service and competitive mortgage rates to help you achieve your homeownership dreams. Be sure to contact multiple lenders, compare their offerings, and choose the one that best meets your needs and financial situation.

By selecting a reputable mortgage lender, you can navigate the home-buying process with confidence, knowing you have a trusted partner to help you every step of the way. Whether you’re buying your first home, refinancing, or investing in property, these top Utah mortgagebanks and brokers are ready to assist you in securing the best possible mortgage for your needs.

Looking to purchase your first home and need advice? Click here.

Need a mortgage rate calculator? Visit our Mortgage Rate Calculator blog here.

Great! You’ve decided to set roots in Utah, the land of stunning landscapes and vibrant communities. But before you picture yourself sipping tea on a cozy porch overlooking the Wasatch Range, there’s the hurdle of navigating the home-buying journey. This guide will provide a one-stop shop for buying a home in Utah real estate market.

Utah is known for its stunning landscapes, strong economy, and family-friendly communities. Here’s why buying a home in Utah could be one of the best decisions you make:

Booming Economy: Utah boasts a robust job market, particularly in tech and healthcare, which makes it a prime location for career growth and stability.

Outdoor Lifestyle: From skiing in Park City to hiking in Zion National Park, outdoor enthusiasts will find plenty to love. Utah’s natural beauty offers numerous recreational opportunities year-round.

Family-Friendly: With excellent schools and safe neighborhoods, Utah is a great place to raise a family. Communities are designed to be welcoming and supportive, making it an ideal place for young families.

Understanding the Utah Real Estate Market

The Utah real estate market is unique and has its own set of trends and characteristics:

Growth Areas: Salt Lake City, Provo, and St. George are some of the fastest-growing areas, attracting new residents due to their vibrant economies and desirable living conditions.

Price Trends: While prices have been rising, there are still affordable options, particularly in emerging neighborhoods across the valley. This offers opportunities for both first-time homebuyers and those looking to invest in real estate.

Overlooking shot of St. George, Utah. (Courtesy of Livability)

Utah Home Buying Statistics

Understanding the current market statistics can help you make informed decisions:

Statistics about Utah Home Buying

Average sale price of homes in Utah (June 2024) [i]

The Economy: Utah boasts a healthy economy, but buying a home requires sound financial planning. In June 2024, 26.6% of homes in Utah sold above list price[iv], which is something to consider when putting in an offer for a home. On the other hand, property tax rates in Utah are low. Utah has the sixth lowest property tax rate in the country at 0.55%.[v]

Getting a Mortgage: Whether you have 3% to put down on a home or 20%, finding the right lender is critical. We’ll explore top Utah lenders offering competitive rates and programs tailored to first-time homebuyers or specific needs.

Finding a Real Estate Agent: A solid real estate agent who will advocate for you in your Utah home buying journey is critical. We’ll discuss the benefits of working with an agent, along with tips for finding the perfect match who understands your needs and the local market.

Once you understand some of the important financial information, you can look at some important considerations for first-time homebuyers to make sure you’re well-prepared.

Tips for First-Time Homebuyers in Utah

Consider State Programs: Utah offers various first-time homebuyer programs and grants. Visit the Utah Housing Corporation for more information.

Budget for Closing Costs: In addition to your down payment, budget for closing costs, which can include fees for inspections, appraisals, and title insurance.

Research Neighborhoods: Take the time to research and visit different neighborhoods to find the one that best suits your lifestyle and needs.

Make sure to look into down payment assistance and loan programs that you may qualify for!

Utah Down Payment Assistance and Loan Programs

Programs

FirstHome

FHA or VA Mortgage

Conventional HFA Advantage Loan

Qualifications

– First time homebuyer – 660 or higher credit score

– Previously owned a home or first-time homebuyer – 620 or higher credit score

This program typically has lower purchase price and income limits and lower interest rates.

Homebuyers can purchase residence with up to 2 units

Financing option for this loan might have a higher interest rate but a lower mortgage insurance costs, which might result in a lower monthly payment.

Source: Down Payment Assistance and Loan Programs. (2023). In Utah Housing Corporation. Utah Housing Corporation. Retrieved July 18, 2024, from https://utahhousingcorp.org/pdf/Form211.pdf

Now that you have all of the information, you are ready for the next steps.

Next Steps to Buying Your Utah Home!

Take the next steps to buying your home!

Get Pre-Approved for a Mortgage

What are today’s mortgage rates in Utah? Check them out here.

Remember: interest rates will vary by lender and by borrower, depending on factors like credit score, loan program, down payment, etc. Compare quotes from at least 3 different lenders to make sure you’re getting the lowest rate.

Ask about down payment and closing cost assistance.

Partner with a knowledgeable real estate agent who knows the Utah market. Consider agents from reputable firms like Coldwell Banker and Re/Max.

Make sure they’re licensed, read reviews, ask questions about how they will help you, and trust your instincts to find the right person to help you buy your home.

[iii] GOBankingRates. (n.d.). The average credit score in each state — see where your state ranks. Nasdaq. https://www.nasdaq.com/articles/the-average-credit-score-in-each-state-see-where-your-state-ranks#

[v] Pitts, E. (2024, February 22). Some states have more affordable property taxes than others. Where does Utah rank? Deseret News. https://www.deseret.com/utah/2024/2/20/24078329/state-ranking-property-tax-value-utah-housing-market/

In the competitive world of home services, having a professional online presence isn’t just an advantage—it’s a necessity. Red Raven AI has revolutionized how local pros grow by creating the first web platform designed specifically for the unique needs of service-based businesses.

Whether you are looking for the best contractor websites to drive leads or need a specialized electrical services website, our platform delivers enterprise-grade technology tailored for the “backbone of our economy”.

Specialized Web Design for Every Trade

Generic site builders often fail to capture the nuances of the service industry. Red Raven AI provides industry-specific solutions, ensuring you have the best roofing websites, best plumbing websites, or best general contractor websites in your local market.

For Electricians: We offer the best electrical contractor websites and electrician website design that focus on safety, reliability, and emergency service calls. Our electrician website builder tools allow for rapid deployment.

For Plumbers: From plumbing company website development to showcasing plumbing website examples, we ensure your plumbing website is optimized for high-intent search terms.

For HVAC & Mechanical: Our hvac company websites and hvac contractor website designs are built to handle peak seasonal demand with 99.99% uptime.

For Landscapers: We build high-performance lawn care websites and landscaping websites that turn visitors into recurring maintenance clients.

The Best Website Builder for Contractors

If you are searching for a website builder for contractors or a website builder for roofing company, Red Raven AI offers two distinct paths to success:

Full-Service Creation: Our expert team can have your contracting company website or renovation company website up and running in as little as three business days.

AI-Enhanced DIY: Use our intuitive electrician website builder or website builder contractor tools featuring drag-and-drop technology and AI-assisted content generation to fill in the gaps.

SEO-First Engineering for Maximum Lead Gen

A contractor website is only effective if customers can find it. Every building construction company website or home improvement contractor websites we build comes with a “Built-in SEO Core”.

Local Dominance: We optimize your contractor website design to rank on Google and Google Maps, ensuring you appear when homeowners search for a building contractor website or electrical contractor website.

Speed & Performance: Red Raven AI delivers lightning-fast pageloads, which is critical for websites for general contractors and landscaping business website owners who can’t afford to lose leads to slow load times.

Conversion Optimization: Every website for electrician, website for plumber, or website for lawn care business is designed with clear calls-to-action to convert traffic into booked jobs.

Enterprise Power for Small Business Budgets

Until now, the level of connectivity found in a Red Raven AI contracting company website—including seamless integrations with CRMs, scheduling, and inventory—was only available at enterprise-level pricing.

“Red Raven AI makes these best sites for contractors accessible to everyone, from solo pros to large teams. Whether you need a simple electrical website templates-based start or a complex roofing company website design, our platform acts as the digital backbone of your business.” – Tony Passey, CEO Red Raven AI Inc (linkedin) and also a Professor of Marketing.

Ready to dominate your local market? Stop settling for a generic website for contractors. Choose the roofing web design company and web design for contractors specialist that understands your trade. Check out Red Raven AI today.

Before you begin to sell your home, it’s important to understand that there are a number of factors you can control to make the home-selling process easier. There are many factors to consider when you are thinking about selling your home. The housing market has undergone some major shifts in the last year so it’s important to consider your options and use the tips we have listed below to aid you in your home-selling process. We go over setting a timeline, home inspections, advising with an agent, and finally listing your home.

Set A Timeline For Selling Your Home

Before beginning the process of selling your home, you need to consider when you want it to be sold and how long it may typically take. There are a variety of websites that offer advice on the best times to sell your home but oftentimes it can be contradictory. Real estate market agencies and companies such as Zillow, Utah Real Estate, and UpNest, offer advice based on the analysis of the home sales around Utah.

5. Put together your listing with a description, photos, and video

6. Hold home showings/ open houses

7. Wait for an offer (or offers) to roll in and negotiate the best deal

8. Accept an offer, and wait for the home inspection/appraisal

9. Close the deal

10. Move out

While this may not be an exhaustive list- it gives opportunity to consider the factors that play a role in selling your home.

Home Inspections

When it comes to getting your home ready to sell/list on the market there are a few things you want to make sure you have done first, as this is a key part in winner over your buyers.

Start with getting a deep clean of your house.

Get an inspector to check the electrical, plumbing, and physical integrity of the home.

Consider contracting for repairs and replacements that may need to be done by professionals after inspection.

Get an handyman to to check all the locks, squeaky doors, running toilets, and other small fixes that can turn a buyer off.

Repaint the walls if necessary, make sure the home is looking new and nice so buyers are attracted to it.

Stage your home with furniture looking nice, nothing lying around and outside landscaped, bushes, grass, trees, etc…

Finally, get a good photographer to take nice professional pictures of the home to make buyers want to come out and schedule a viewing.

This is the make or break for selling a home. No one want’s to buy a home that looks like it has not been taken care of properly. First impressions are everything and you want your buyer to have love at first sight when viewing your home.

Advising with an Agent

Many people either choose the route of selling on their own or going through an agent. Before getting ready to list your home on the market, consider advising with an agent to make all the preparations and gather all the details you need. Advising with an agent and having them assist in the home selling process can position your home on the market for the best possible sale.

It’s important to research agents’ profiles and consider their time in the industry, sales, and how they are marketing their listings-note the quality of their photo listings and where they post their listings is an important factor to consider as well.

Advising with an agent who understands the current market is a key factor in having a smooth and successful sale.

Listing Your Home

When it comes to listing your home on the market one of the best practices is to take professional photos and clean the home to make it appealing. You might want to have the home without furniture (staging the home), or you might want to give the home buyers a picture of what the home looks like with everything in it. Either way, you want the home to be appealing to potential home buyers.

Another great thing that helps when listing your home for sale is to focus on an online appeal. Experts say that nearly all homebuyers look at online listings; meaning that your home’s first showing is online (Bankrate, 2023). So, taking good photos, adding a detailed description, and adding an open/time-slotted showing can help you sell your home quickly.

Summary

Selling your home can be a hassle, but doing all the topics mentioned above can help one sell their home in no time. We have covered most of what it takes to sell a home in order, starting with planning a timeline for the whole process of selling your home. We have also gone over what it takes to make the home look appealing. Whether that is renovating it, decorating it, staging it, or taking professional photos so that it catches one’s attention. However, if you are a first-time home buyer, selling a home is much different than buying a home. If you are interested in buying a home, check out our site on how to buy a home.

A money market account (MMA) is an interest-bearing savings account that enables banks to pay customers on a yearly interest rate in exchange for account owners to store money in their bank. Money Market Accounts allow customers to deposit money and earn interest similar to a savings account while simultaneously reaping the benefits of a checking account. These benefits include debit cards, the ability to write checks, and ATM withdrawals. MMAs are unique from other interest-bearing accounts because these accounts pay a tiered variable interest rate (different rates) determined by how much money an account holder has in the account. These rates will vary depending on the current interest rate within the money markets. The interest rate offered is usually more than a typical savings account but can fluctuate depending on market conditions.

First-time home buying? Refinancing? Wanting painless mortgage payments? This article is for YOU!

Why Create a Money Market Account?

There are a variety of options that provide similar solutions to money market accounts. Savings accounts, certificates of deposit (CDs), and mutual funds are all available alternatives to MMAs. So, what’s the difference between these, and why go with an MMA over the others? Money market accounts are similar to savings accounts, but they offer more flexibility with varying ways to use and move funds. Savings accounts also typically offer lower interest rates. Similar to MMAs, certificates of deposit offer competitive interest rates. The primary difference is that MMAs make it easier and faster to access your funds, and CDs often have penalties for early withdrawal. Finally, the main distinction between MMAs and mutual funds is that mutual funds are not insured like MMAs, which we will discuss more in-depth later.

MMA Benefits (Refinancing, Down Payments, and Mortgages)

Who doesn’t want to save money? Money market accounts provide a very safe method of storing finances while simultaneously earning interest. Many banks and credit unions offer these accounts along with interest rates as high as 5%, and they often place characteristics of both savings and checking accounts. We know how hard it is to save up for an initial down payment on a home, and money market accounts help take some of that unwanted stress off your hands. To explore more of the pros and cons of putting your funds in a money market account, look at this educational article by Forbes.

Is a Money Market Account Right For You?

To know whether a money market account is right for you, reach out to one of our experts here. One of the main must-know advantages of a money market account is being able to use checks or a debit card linked to the account WHILE you earn interest. Another great thing to know is that $250,000 is insured for each individual owning an account, and up to a maximum of $500,000 is federally insured for joint accounts.

Best Market Conditions to Open an MMA

Whether you’re preparing to save money for a down payment, to refinance your home, or to pay a monthly mortgage, MMAs have minimal downsides. The require down payments slightly more than your average savings account, typically around $1,000. To do additional research, you can read this article that gives an overview on regulations regarding transfers and withdrawals. Right now in today’s market, some of the best MMAs include UFB Direct, Vio Bank, and CFG Community Bank. Take a look at some of the other top MMAs and what they have to offer to get a better understanding of current market conditions and which specific MMA is the best for you. At the end of the day, money market accounts are worth considering, especially when preparing to make mortgage payments, take out a home loan, refinance your home, or even increase your home equity.

Say Yes to an MMA Because There Are No Reasons to Say No

Deciding whether or not a money market account is a good fit for you is based on what it is you are looking to get out of an interest-bearing account as well as what things you will be using it for, such as mortgage payments, saving up for a down payment, and maybe even preparing to take out a home loan. To figure out what account type is right for you, there are many different articles, such as an article called “What is an Interest Baring Account,” which has a lot of great information, as well as our site, which provides more information on what a money market account would mean to you.

Become a millionaire real estate investor by simply purchasing homes.

Have you considered the benefits of becoming a landlord as rent prices and real estate prices around the world continue to increase? To illustrate, interest rates are a negligible detail when a renter is paying the entirety of your mortgage. Wouldn’t you agree?

Investing in real estate has a reputation that discourages Americans.

Yet, the most tried and true path to building generational wealth involves owning multiple homes and having tenants cover your mortgage expenses. However, traditional investment properties, secondary mortgages, and rental loans often demand a 20% down payment and savings.

Furthermore, these requirements create a substantial barrier for aspiring investors and families. Not to mention these mortgages designed specifically for rentals often carry unattractive interest rates that prevent the ability to qualify further.

Housing is the only necessity disguised as an investment vehicle.

21,951,000 people in the U.S. have a net worth of $1 million or more. 40% of an average millionaire’s assets consist of real estate.

federal reserve

The key to this strategy is occupancy.

For this reason, at Utah Mortgage Rate we provide a unique pathway to help you become a millionaire real estate investor. Especially, for our clientele with limited cash assets. To begin, the strategy to growing an abundant real estate portfolio is through primary mortgages.

Owning a real estate portfolio worth millions is achievable through primary mortgages.

Image the equity gains you’ll acquire over time if you own multiple mortgages.

To clarify, this strategic approach regarding occupancy allows you to accumulate home loans that require minimal cash down payments. You can transition your first property into a rental property when you’re ready to occupy a new home. It’s crucial to buy your next property with the intent to live in it initially. Primary mortgages are only originated for owner-occupied properties.

In other words, this strategy secures better mortgage terms and gives investors the opportunity to accumulate properties without large down payments. Eventually, after that one year has passed you can apply again for another primary mortgage with a Mortgage Broker.

As a result, your first home becomes an income-generating asset, generating generational wealth and appreciating over time. More importantly, the mortgage terms remain unchanged throughout this process.

Don’t wait to buy real estate. Buy real estate and wait.

However, imagine sitting down with an expert Mortgage Broker and a Local Utah Realtor today. Above all, we can discuss the beginning of many investments in real estate with a no obligation consultation.

Welcome to a beginner’s guide to banking. If you are looking to get a better understanding of basic banking for beginners, or just starting out on your financial journey, you are in the right place. Banking is the foundation of personal finance, and it is important to understand it with confidence. This page provides you with a basic understanding of four crucial pieces to a healthy personal financial plan. Once you are familiar, we recommend that you navigate to other pages on this website for deeper insights.

Checking and Savings Accounts

The first step of the beginner’s guide to banking is opening checking and savings accounts. A checking account stores the majority of your spending money. This account is used for day to day purchases and a great start for banking with 16 year olds. You can access the money in this account by making cash withdrawals at a branch or using a debit card. You can fund this account with cash or check deposits. Once you are comfortable with the amount in your checking account, you can start a savings account. It is recommended that every adult has a savings account that can cover you for 3-6 months with no income. Savings accounts are a place to store money for a rainy day. They are not as easily accessible as a checking account. However, you can make transfers from your savings account to your checking account if needed. Savings accounts typically pay interest. Hence, the balance in your account will increase by a specific percentage each month, even if you do not make any additional deposits. To find what are good banks to open an account with, you can check different interest rates on websites such as Nerdwallet. There are also different types of savings such as money market accounts and CD’s. (insert internal links to money market page and CD page)

Learn Banking For Beginners To Help Your Family

Credit Score

Your credit score is essentially a ranking given to you by a reporting from places such as Transunion or Experian. A good credit score allows you to take out loans with better interest rates and apply for credit cards with better benefits. Eligibility for a credit card begins at 18. Therefore, many parents help their children open this account when they start banking for seniors. In order to have a good credit score you must have a credit history. You collect this by obtaining a credit card, using it, and paying it off on time. Credit cards allow you to borrow a set amount of money each month. It is important to pay it off before the end of the month so that there is no interest. However, the longer each month you wait to pay it, interest will accrue meaning that the balance will grow. To have good credit you also must make good on your loan payments.

Credit Score Ranges

800 to 850: Excellent – Borrowers within this range are deemed low-risk. This makes it easier for them to secure loans compared to those with lower scores.

740 to 799: Very good – Those falling into this category have a track record of positive credit behavior, increasing their chances of approval for additional credit.

670 to 739: Good – Lenders generally regard individuals with credit scores of 670 and above as acceptable or low-risk borrowers.

580 to 669: Fair – People in this group are often labeled as “subprime” borrowers. They are considered higher-risk by lenders and may struggle to qualify for new credit.

300 to 579: Poor – Individuals within this range frequently face challenges in obtaining new credit. If you find yourself in the poor category, it’s likely that you’ll need to take steps to improve your credit scores before securing any new credit.

How It Feels To Have a Good Credit Score

Loans

A loan is an arrangement where one party borrows money from another. In this case, we will assume that you are the borrower and a bank is the lender. You will pay back this money over time with interest. This means that you will pay the lender back more money than what you borrowed. Paying back a loan quickly reduces the amount of interest you’ll need to pay. People use loans for various purposes, including buying cars, boats, managing personal finances, and acquiring homes. There are multiple different types of home loans, such as FHA loans and VA loans. Loans are a valuable resource but can cause intense levels of debt. That is why it is important that you comprehend the terms and repayment schedules of your loans.

Investing

To learn to invest is where finances get more complicated. However, trained professionals can help you. Investment companies such as Fidelity and Edward Jones can help match you with an advisor. Financial advisors help find an investment strategy that meets your goals while staying within your risk tolerance and financial capability. These strategies can include stocks, bonds, real estate, or businesses. The typical goals of investing are to generate and preserve capital. In today’s economy, to begin investing is often a vital piece of a healthy financial plan.

Next Steps In Banking For Beginners

While some banks might offer different interest rates or incentives, there is no best bank for beginners. It depends on your situation and preferences. Banking is crucial, and although there are many different ways to go about it, we are here to help. Just by being on this page, you are taking the first step to learn more about finances. After reading a beginner’s guide to banking, you can find many other helpful resources on our website. Learn about Home Equity Lines of Credit HELOC, Refinancing, How to Start Investing, and How to Prepare for Buying a Home.