The dream of owning a home in the Beehive State is more achievable than many realize, especially with the current Utah housing market forecast 2026 indicating a shift toward a more balanced environment. After years of rapid price escalation, inventory has stabilized, and buyers finally have more room to breathe. However, the most common question remains: Is now a good time to buy a house in Utah? For those prepared to leverage state resources, the answer is a resounding yes. By understanding the various Utah first time home buyer programs, you can navigate the path from renting to owning with financial confidence.

How to Qualify for a Mortgage in Utah and Secure Your Financing

Before you begin touring neighborhoods, you must understand the financial benchmarks required by local lenders. Learning how to qualify for a mortgage in Utah starts with a deep dive into your credit health. The minimum credit score for mortgage in Utah typically ranges between 580 and 620 depending on the loan type, though a higher score will always unlock more competitive interest rates.

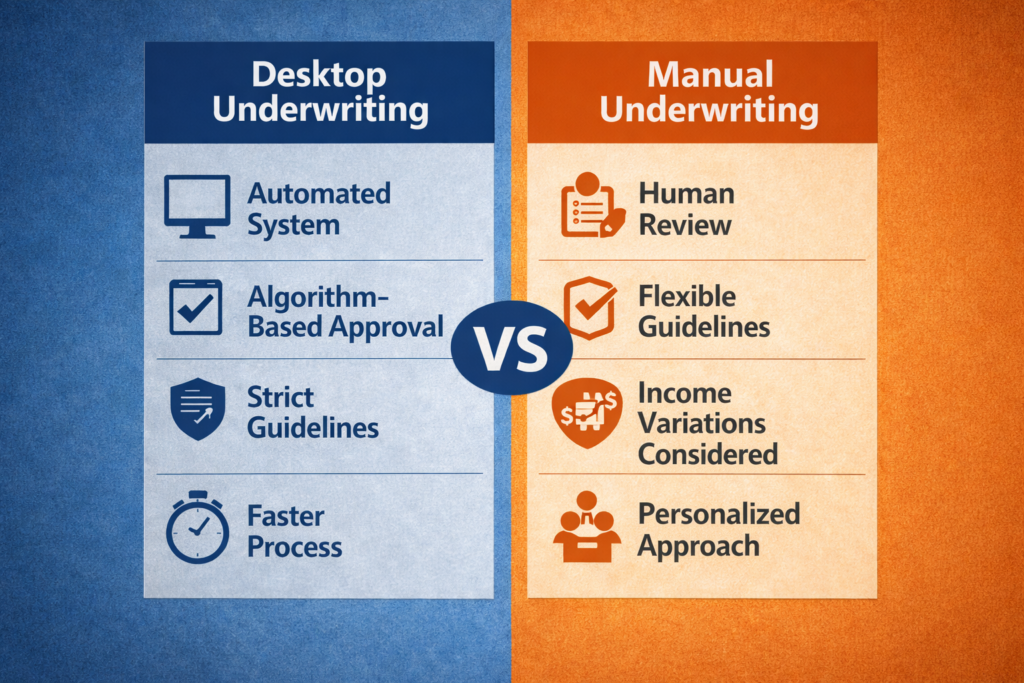

To gain a competitive edge, you should initiate the Utah home loan prequalification process as early as possible. This preliminary step gives you a ballpark figure of your borrowing power. However, in a serious market, a formal mortgage pre approval Utah is the “gold standard.” This document proves to sellers that a lender has fully vetted your financial documents and is ready to fund your purchase. During this phase, many buyers ask, “how long does mortgage approval take in Utah?” Generally, once you are under contract, the full underwriting process takes between 30 and 45 days.

Choosing the right loan product is equally vital. Most buyers weigh the pros and cons of an FHA vs conventional loan Utah. An FHA loan is excellent for those with lower credit scores or smaller down payments, while conventional loan requirements Utah often demand a slightly higher credit profile but may offer lower long-term costs. For specific groups, there are specialized paths:

- Utah VA loan eligibility: Veterans and active-duty members can often buy with $0 down.

- Utah rural development loan requirements: Those looking in less populated areas may qualify for zero-down USDA financing.

Utah Home Buying Process Step by Step: From Search to Closing

Navigating the Utah home buying process step by step requires a blend of patience and preparation. Once you have secured your pre-approval, the next step is determining your budget. Use a Utah mortgage calculator to look beyond the listing price and understand the full monthly impact of your investment. This tool will help you answer the critical question: “How much house can I afford in Utah?”

When calculating your budget, don’t forget to account for the average mortgage payment in Utah, which includes principal, interest, taxes, and insurance (PITI). As you monitor the market, keep a close eye on Utah mortgage rates today. In early 2026, 30 year fixed mortgage rates Utah have stabilized, offering a more predictable environment than the volatility seen in previous years. You will also need to decide between a fixed vs adjustable mortgage Utah. While a fixed rate offers a “set it and forget it” stability, an adjustable-rate mortgage (ARM) might offer a lower initial rate if you plan to move or refinance within a few years.

As you approach the finish line, you must prepare for closing costs in Utah. These fees, which cover everything from title insurance to appraisals, typically range from 2% to 5% of the home’s purchase price. To ensure you aren’t overwhelmed by these upfront costs, work with the best mortgage lenders for first time buyers Utah who can help you structure your offer to potentially include seller concessions or lender credits.

Maximizing First Time Home Buyer Grants Utah and Assistance

The most powerful tool in a new buyer’s arsenal is the availability of first time home buyer grants Utah residents can access. The state government and local municipalities have recognized the affordability challenge and created robust down payment assistance Utah initiatives.

One of the most popular programs is the “silent second” mortgage offered through the Utah Housing Corporation, which can provide the funds needed to cover your initial down payment or closing costs. These programs are often designed to work in tandem with other local first time home buyer grants Utah, effectively lowering the barrier to entry. For example, some cities offer forgivable loans if you stay in the home for a set number of years.

Even after you’ve successfully closed on your home, your financial strategy shouldn’t stop. As market conditions change, keep an eye on Utah refinance options for first time buyers. If interest rates drop significantly after your purchase, refinancing can help you lower your monthly payment or eliminate private mortgage insurance (PMI) more quickly as your home equity grows.

Conclusion: Securing Your Future in Utah

The 2026 market presents a unique opportunity for those who are well-informed and ready to act. By mastering the Utah home buying process step by step and taking full advantage of Utah first time home buyer programs, you can secure a home that fits both your lifestyle and your budget. Whether you are aiming for a zero-down path through Utah VA loan eligibility or seeking the best down payment assistance Utah has to offer, the resources are there to support you. Start your journey today by speaking with a local expert to begin your mortgage pre approval Utah and turn the dream of homeownership into a reality.

")