Buying your first home in Utah is a thrilling yet often intimidating journey. Understanding the costs and lenders is essential. One of the best tools to start with is a first time home buyer down payment calculator, which gives you a clear picture of how much you’ll need upfront. This guide helps you navigate every step, from loan application to approval.

Whether you’re learning how to apply for a home loan first time buyer or comparing the best mortgage lenders for first time home buyers, this guide has you covered

How to Apply for a First Time Home Loan Using a Down Payment Calculator

To begin with, the first step is knowing how to apply for a home loan first time buyer. Check your credit and gather documents like pay stubs and bank records. Having this ready makes the application process smoother.

You might also be asking how to apply for a mortgage first time home buyer. The answer is similar, but often includes choosing the right lender who understands your needs as a new buyer. Many Utah lenders offer local support and digital applications, making it easier than ever.

In addition, don’t miss out on incentives. Understanding how to apply for first time home buyer incentive programs can lead to reduced costs or lower interest rates. These vary by location, so be sure to ask lenders if they offer state or federal aid. For more guidance on the mortgage process and how lenders evaluate borrowers, visit the Consumer Financial Protection Bureau’s home buying guide.

How to Qualify Using a First Time Home Buyer Down Payment Calculator

Before applying, many people ask how to qualify for a home loan first time buyer. Lenders want to see consistent income, good credit, and manageable debt. Programs like FHA loans are designed to help new buyers and offer flexible requirements.

Searching how to qualify for home loan first time buyer often leads people to state and federal options. These programs help lower-income or lower-credit applicants. If you’re unsure where to start, consult a Utah-based mortgage advisor who can help you determine your eligibility.

Getting Approved and Pre-Approved

Many new buyers confuse approval with pre-approval. To clarify, getting approved for a home loan means you’ve submitted all documents and received a firm loan offer. In contrast, pre-approval is an initial review based on basic financials.

To strengthen your position as a buyer, seek out the best pre-approval mortgage options for first-time home buyers. These offers provide a letter you can show to sellers to confirm you’re financially qualified, giving you an edge in Utah’s competitive housing market. You can learn more by reading our step-by-step guide to mortgage pre-approval in Utah.

When you’re ready, look up where to apply for a first-time home buyer loan and explore both local and national options. Utah-based lenders may offer better rates or service.

Best Mortgage Lenders for First Time Home Buyers in Utah

Choosing the best mortgage lenders for first time home buyers can be daunting. Start by comparing interest rates, down payment requirements, and customer service.

Also look for:

• best mortgage lenders for first time home buyer

• best mortgage lenders for first time homebuyers

• top mortgage lenders for first time home buyers

• best home mortgage lenders for first time buyers

Furthermore, local lenders might also qualify among the best loan companies for first time home buyers, especially if they offer customized advice and faster response times.

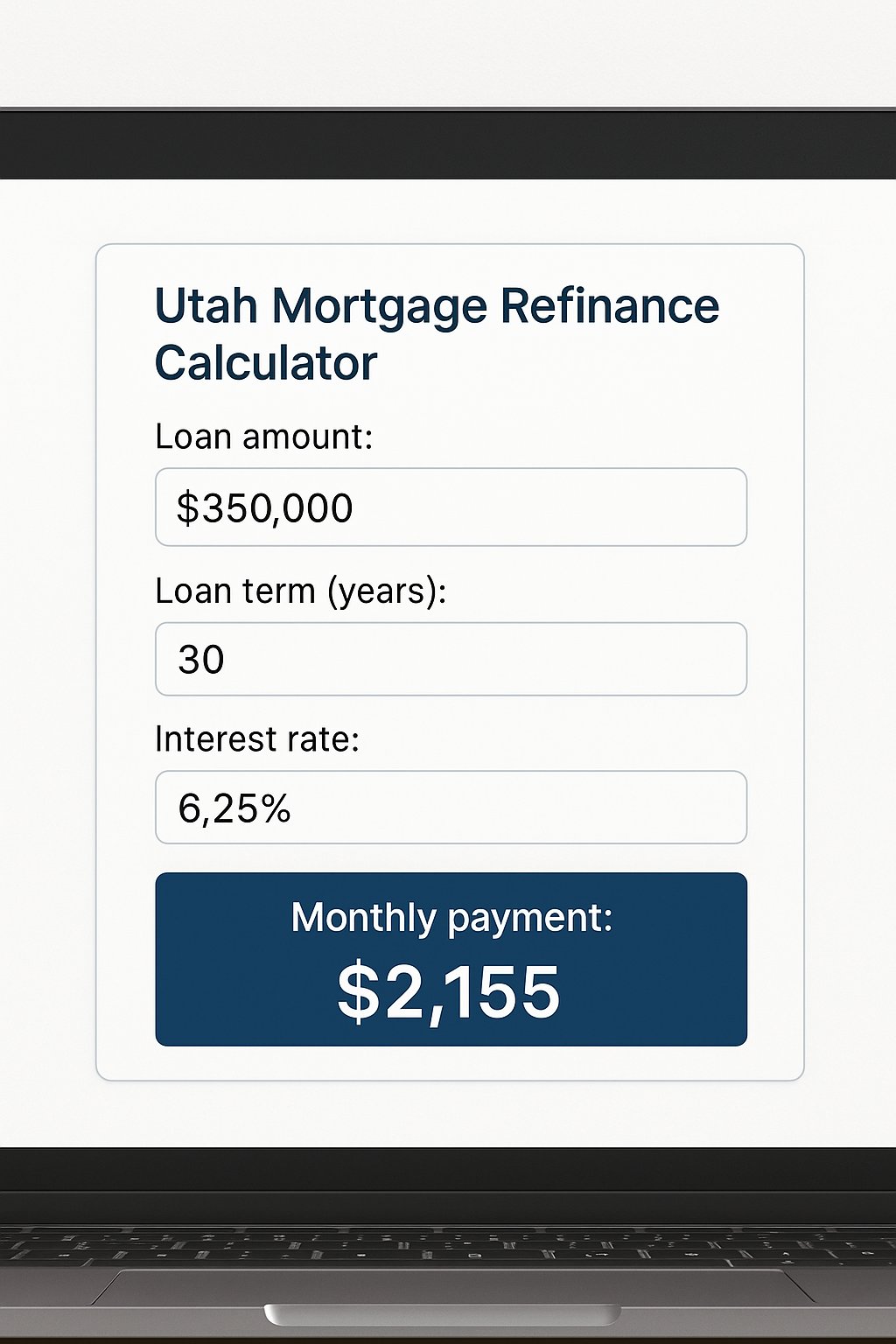

Down Payment Calculators and Financial Tools for First Time Home Buyers

A first time home buyer down payment calculator is your best friend when budgeting. It helps you estimate your upfront costs and monthly payments based on property value, loan terms, and credit.

If money is tight, explore first time home buyer programs with bad credit. These typically include FHA, VA, or USDA loans, which reduce credit score requirements and often allow for down payments as low as 3.5% (https://www.hud.gov/program_offices/housing/fhahistory).

Some of the best lenders for home loans first time buyers will walk you through these options. Use this tool to compare what’s required from the best mortgage company for first time home buyers versus other banks or brokers.

Compare and Choose Wisely

You might also come across the following when doing your research:

• best mortgage company for first time home buyer

• best mortgage companies for first time homebuyers

• best home loan companies for first time buyers

• best mortgage loan company first time home buyer

• best lending companies for first time home buyers

Each offers slightly different benefits—some specialize in digital tools, while others prioritize hands-on service. Read reviews, compare APRs, and ask about closing timelines. The right choice depends on your needs and goals.

Final Steps Toward Homeownership

The road to homeownership includes many steps, but with proper planning, it doesn’t have to be difficult. Knowing how to get approved for a first time home loan, using a first time home buyer down payment calculator, and comparing the best mortgage lenders for first time home buyers will prepare you for success.

Whether you’re applying through the best mortgage company for first time home buyer or relying on first time home buyer programs with bad credit, the tools and resources are out there—and now you know how to use them.