Understanding mortgage rates today is essential for anyone considering a home purchase or refinance in Utah. Whether you’re just starting your home search or locking in financing, learning about rate trends, loan types, and pre-approval steps can make a big difference in what you pay over time.

Current Mortgage Rates in Utah

As of June 28, 2025, the average 30-year fixed mortgage in the U.S. is approximately 6.77% (source). Utah typically tracks closely with these national trends. It’s wise to compare mortgage quotes from at least three providers to find the best mortgage rates available for your situation.

Apply for a Mortgage in Utah

Before you apply for a mortgage, gather key documents like pay stubs, tax returns, and bank statements. Most lenders in Utah support secure online portals that simplify the application process. Early in your home search, you should prequalify for mortgage options to estimate how much home you can afford.

Getting mortgage pre approval helps solidify your budget and makes you more attractive to sellers in Utah’s competitive housing market. Need help navigating the process? Talk with a mortgage lender or mortgage broker near me for personalized advice.

Finding the Best Mortgage Lender

Choosing the right mortgage lender or working with a mortgage broker can save you time and money. Brokers have access to multiple loan products and help find the most competitive mortgage rates today. The best mortgage companies combine solid rates with strong customer service and local expertise.

Explore Loan Options: VA and Conventional Loans

If you’re a veteran or service member, a VA home loan may offer no down payment and favorable VA loan rates. Utah lenders frequently support these programs, helping eligible buyers secure more affordable financing.

Not eligible for a VA loan? A conventional loan is still a great option for borrowers with strong credit. Your local mortgage broker can help you evaluate fixed vs. adjustable rates and find the loan product that fits best.

Why You Should Shop Around

Even a 0.5% difference in your mortgage rate could save you tens of thousands of dollars. That’s why comparing lenders is so important. According to Freddie Mac, borrowers who shop for the best mortgage rates can benefit from significant rate dispersion (source).

When buying a home for the first time, your first question should be what kinds of first time home loans exist for you. This guide is crafted to illuminate the process of how to get a mortgage in Utah, specifically tailored for those who are purchasing a home for the first time. We will explore everything from essential loan options to crucial financial aid, offering a clear roadmap of the steps to get a mortgage first time buyer. Our aim is to provide you with the insights needed to navigate this significant investment with confidence.

Key Utah First Time Home Loan Programs

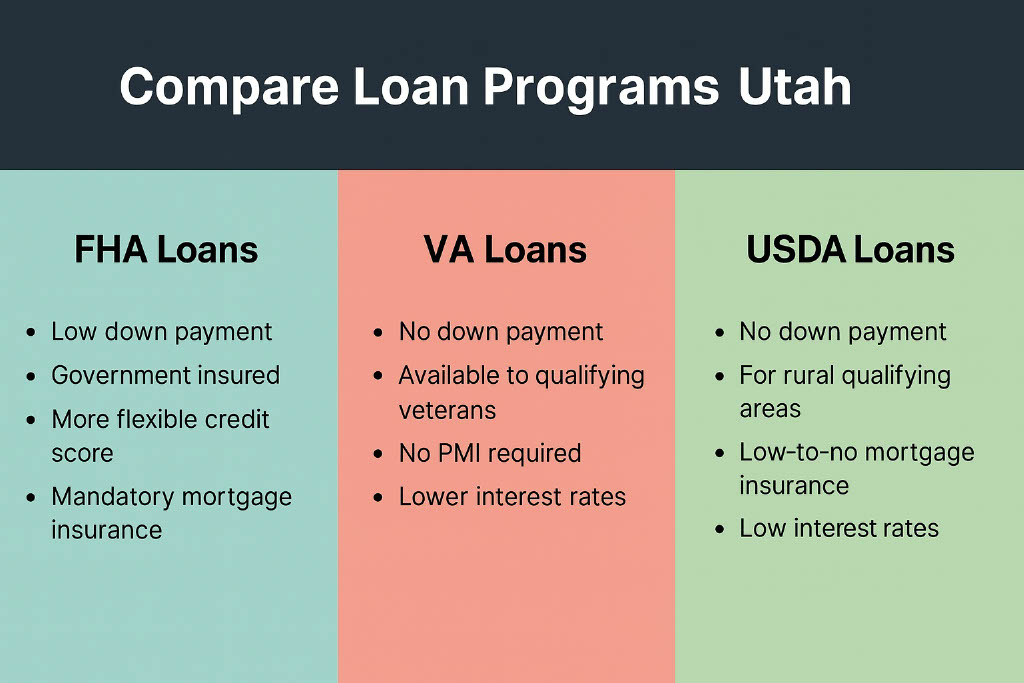

For individuals and families looking to buy their inaugural property, Utah presents a diverse array of financial avenues. These specialized Utah mortgage programs for first-time buyers are meticulously designed to enhance accessibility and alleviate the initial financial burden. Such programs frequently feature appealing terms, reduced down payment stipulations, and occasionally, attractive interest rates. It’s imperative to delve into these options thoroughly before you apply for a mortgage first time buyer. An understanding of loan types, such as FHA, VA, USDA, and various conventional loan products, can shape your experience. Exploring the landscape of first time buyer programs is your initial strategic move.

The question, “can I get a first time home loan even with limited savings for a down payment?” is common. The good news is, absolutely! Several options cater to different financial situations. For instance, FHA loans are popular because they typically require a lower down payment and have more flexible credit requirements. VA loans, exclusive to eligible service members and veterans, can even offer 0% down payment. For those considering homes in designated rural or suburban areas, USDA loans also stand out with their zero-down feature. Grasping the distinctions between these options is a fundamental aspect of getting a first time home loan and setting pragmatic expectations for your property search. Many discover this is truly the best way to get a first time home loan given their circumstances. Similarly, exploring general first time home loan options will reveal a broader landscape of possibilities.

Maximizing Your Potential with Utah Down Payment Assistance Programs

One of the most significant financial considerations for new homeowners often revolves around accumulating sufficient funds for the down payment. Fortunately, Utah residents have access to various Utah down payment assistance programs specifically created to mitigate this challenge. These vital programs manifest in several forms: outright grants (funds that do not require repayment), deferred second mortgages (where repayment is postponed), or even forgivable loans (which are forgiven over time if certain conditions are met).

Utah Statewide First-time Homebuyers Assistance Program

For instance, the statewide First-time Homebuyers Assistance Program offers a compelling opportunity. This program can provide a loan of up to $20,000 with a 0% interest rate and no monthly payment, designed to assist with interest rate buy-downs, down payments, or closing costs. To qualify, individuals generally must not have owned a home in the previous three years, have lived in Utah for at least one year prior to closing, and purchase a new build or never-lived-in home up to a specific price cap (e.g., $450,000).

Local Assistance Programs

Beyond statewide initiatives, many individual cities and counties offer their own unique assistance. In Ogden City, the Own in Ogden program provides loans of up to $10,000 to help with down payments, closing costs, or principal reduction. While not exclusively for first-time buyers, it’s a valuable resource within its jurisdiction. These programs showcase the variety of options available, each with its own eligibility criteria and benefits. Diligent research into these programs can substantially decrease your immediate out-of-pocket expenses when acquiring a home.

Beyond traditional down payment expectations, learning how to apply for first time home buyer incentive programs is a strategic move. These incentives can transform aspirational homeownership into tangible reality. It’s highly advisable to collaborate with a local mortgage professional well-versed in Utah’s specific down payment and buyer incentive programs. These offerings are dynamic and often subject to change, making expert guidance invaluable. Such professionals can help identify the best first time home buyer programs for you.

Demystifying the Mortgage Application and Qualification for First Time Homebuyers

Once you’ve identified suitable loan products and explored down payment assistance, the next crucial phase is the application and qualification. When you’re prepared to apply for first time home buyer mortgage, be ready to compile and submit comprehensive financial documentation. This typically includes recent pay stubs, W-2s or tax returns, bank statements, and a detailed credit report. An organized approach to gathering these documents will ensure a smoother process when applying for first time home loan. Lenders meticulously review this information to evaluate your financial stability and determine your eligibility for financing. For those exploring their options, knowing how to apply for home loan first time buyer through various channels is also beneficial.

How To Qualify?

A frequently asked question is, “how to qualify for a home loan first time buyer?” Lenders primarily assess three pillars: your credit score, your debt-to-income (DTI) ratio, and your employment stability. While there isn’t a universal “perfect” combination, generally, a higher credit score, coupled with a manageable DTI ratio, results in more favorable loan terms. Don’t be discouraged if your initial financial assessment isn’t ideal. Many lenders and housing agencies provide resources and counseling on how to qualify for home loan first time buyer effectively. This might involve strategies like reducing existing debt, correcting inaccuracies on your credit report, or increasing your savings for a larger down payment. Ultimately, mastering the art of getting a first time mortgage involves meticulous preparation.

The preliminary step towards getting approved for a home loan first time buyer often involves securing a pre-approval. A robust pre-approval letter serves as a powerful signal to potential sellers that you are a serious, financially capable buyer. It precisely outlines the maximum loan amount you are eligible to borrow, providing a clear budget for your home search. This initial approval streamlines your property search and strengthens your offers. Remember, the journey to becoming a first time home owners loan recipient is about understanding all available resources.

You can do it!

The path to homeownership as a first time buyer in Utah is entirely achievable with diligent preparation and guidance. Focusing on understanding Utah mortgage programs for first-time buyers, leveraging available Utah down payment assistance programs, and meticulously preparing for the qualification process are your keys to success. Navigating the process of getting a mortgage first time buyer involves more than just rates; it’s about finding the right financial fit for your long-term aspirations. By understanding the nuances of how to get a first time home loan and embracing the best way to get a first time home loan for your unique situation, you can transform the dream of owning a home in Utah into a tangible reality.

Dreaming of owning your first home in the Beehive State? That’s an exciting milestone! First, understanding your first-time homebuyer mortgage in Utah is your most important step. Many potential homeowners start by looking at 30-year mortgage rates. Indeed, this is a common choice for home loans. However, you must learn much more to successfully navigate the Utah housing market. Specifically, consider unique local factors and available programs.

Therefore, this comprehensive guide will walk you through the essential aspects. We’ll cover everything from pre-approval to understanding different loan types. Moreover, we’ll help you navigate final costs. Ultimately, this ensures you’re well-equipped for your homeownership journey in Sandy, Utah, and beyond.

Kickstarting Your First-Time Homebuyer Journey with Utah Mortgage Pre-Approval

One of the very first things you’ll need to do is get pre-approved for a home loan in Utah. Do this even before you browse listings. Simply put, this isn’t just a suggestion; it’s a critical step that empowers you as a buyer. Pre-approval signals to sellers that you’re a serious, qualified candidate. As a result, this gives your offer significant weight in a competitive market.

To prepare, assemble a comprehensive Utah mortgage pre-approval checklist. Typically, this involves gathering recent pay stubs, bank statements, tax returns, and details on any existing debts. To get an early sense of your borrowing capacity, try using a mortgage pre-approval calculator online. Consequently, this can provide a preliminary estimate of what lenders might offer. It helps you set a realistic budget for your new home. For a quick estimate, try our Online Mortgage Calculator!

Exploring Diverse Utah Home Loans and Fulfilling Requirements

Utah offers a diverse landscape of home loans. In fact, each design meets varying financial circumstances and needs. For many embarking on a first-time buyer mortgage journey, government-backed programs often present the most advantageous paths.

You must thoroughly understand FHA loan requirements in Utah 2024. These loans are popular for their lower down payment options and more flexible credit score guidelines. For example, Neighbors Bank typically requires a 3.5% down payment with a 580+ credit score for FHA loans (Neighbors Bank FHA Loan Guide).

Furthermore, if you’re a veteran or active service member, explore Utah VA home loan requirements. These can offer exceptional benefits, including no down payment and competitive interest rates (Veterans United VA Loan Eligibility). Similarly, for those looking in more rural areas, ask “do I qualify for a USDA loan in Utah?” This might lead to another excellent zero-down payment opportunity. Crucially, this program tailors for specific communities.

In summary, each of these programs comes with unique criteria. Therefore, consulting with a knowledgeable local mortgage professional is always recommended. They can help identify the best fit for your situation. Learn more about specific loan types on our Loan Programs Page.

Finding Competitive Rates and the Best Lenders in Utah

Securing your first-time homebuyer mortgage in Utah means more than just getting approved. Instead, it means finding the most favorable terms. To do this, diligently compare mortgage lenders in Utah. Everyone aims for the lowest mortgage rates in Utah today. Currently, 30-year fixed mortgages average around 6.93% as of June 21, 2025 (Bankrate Utah Mortgage Rates). However, you also must consider the lender’s overall service, fees, and reputation.

Don’t solely focus on advertised 30-year mortgage rates. Instead, look at the Annual Percentage Rate (APR). This provides a more complete picture of the loan’s true cost, including various fees. Seeking out Utah mortgage broker reviews can offer invaluable insights. Specifically, these reviews show other borrowers’ experiences. This helps you pinpoint the best mortgage lenders in Utah for first-time buyers who prioritize client satisfaction and transparency. A good mortgage broker can be a significant asset. After all, they often work with multiple lenders. This helps you secure the most competitive terms available.

Demystifying Mortgage Costs with Calculators and Financial Planning

As you move closer to making an offer, clearly understanding your home loan’s financial implications becomes paramount. While a simple mortgage calculator can quickly estimate your principal and interest payments, a more accurate picture requires a Utah mortgage calculator with taxes and insurance. This comprehensive tool factors in your estimated monthly property taxes and homeowner’s insurance premiums. Indeed, these are significant components of your total monthly housing expenses in Utah.

To help set a realistic budget for your home search, a mortgage affordability calculator will assess how much home you can truly afford. It bases this on your income, existing debts, and living expenses. Beyond monthly payments, remember to budget for average closing costs in Utah. These are the various fees associated with finalizing your mortgage and transferring property ownership. They typically range from 2.48% for sellers in Utah (Clever Real Estate Closing Costs) but generally 2-5% for buyers. For instance, these costs cover items like lender fees, title insurance, and appraisal costs. Being prepared for these upfront expenses is key to a smooth closing.

Navigating the Application Process and Future Refinancing Options

The culmination of your planning for a first-time homebuyer mortgage in Utah is the formal application process. Knowing exactly how to apply for a mortgage in Utah streamlines this final stage. This involves submitting all necessary documentation from your Utah mortgage pre-approval checklist. Then, you formally apply for the chosen loan program. Be prepared for a detailed review of your financial history and employment.

Understanding the Utah mortgage timeline from offer to close can help manage expectations. Generally, this period typically ranges from 30 to 60 days. It encompasses appraisals, inspections, and final underwriting.

For existing homeowners in Utah, or those who plan to be homeowners for many years, understanding how to refinance a mortgage in Utah is also valuable knowledge. A mortgage refinance calculator can illustrate potential savings or benefits. This comes from adjusting your current loan terms. Perhaps, you want to lower your interest rate, change your loan term, or access home equity. Options like refinancing a VA home loan in Utah offer specific advantages for eligible veterans. They can leverage their benefits again.

When buying a home or refinancing an existing mortgage, one of the most important decisions you’ll make is choosing the right mortgage length. The term of your loan directly affects your home loan mortgage rates, monthly payments, and how much interest you’ll pay over time. With so many options available—ranging from the well-known 30 year mortgage rates to shorter and less conventional terms like 2 year fixed home loan rates—it’s crucial to understand how each loan length works and how to choose the best fit for your financial situation.

Understanding Home Loan Mortgage Lengths

Home loan mortgage rates refer to the interest rate you pay on the money borrowed from a lender. These rates vary based on multiple factors including the loan term, credit score, market conditions, and whether the rate is fixed or adjustable.

The longer the mortgage term, the higher the interest rate tends to be. However, the monthly payments are usually lower. Shorter-term loans typically come with lower rates but higher monthly payments. Choosing between them depends on your financial goals, income stability, and long-term plans.

Which mortgage length is right for you?

Common Mortgage Lengths

30-Year Mortgage

The 30 year mortgage rates remain the most popular option for homebuyers due to their lower monthly payments. Though you’ll pay more in interest over the life of the loan, this option makes homeownership accessible and manageable for many.

Today’s 30 year mortgage rates and 30 year rates offer stable, predictable payments—perfect for those who plan to stay in their home long-term.

15-Year Mortgage

15 year mortgage rates and 15 year fixed mortgage rates appeal to buyers who want to pay off their loan quickly and save on interest. The trade-off is higher monthly payments, but you’ll build equity faster and pay far less interest over time.

Check 15 year fixed mortgage rates today to see if now is a good time to lock in a low rate. You can also explore your financial outlook using tools like a 15 year fixed mortgage rates calculator or a 15 year mortgage refinance calculator.

If you’re already paying a 30-year loan and can afford higher monthly payments, refinancing into a 15yr mortgage rate may be a financially sound move.

10-Year Mortgage

10 year mortgage rates offer even faster payoff and lower interest rates. These are ideal for buyers who have significant income and want to eliminate debt quickly. You can estimate your savings with a 10 year mortgage rates calculator, which will show how much faster you’ll gain equity and how much less you’ll pay in total interest.

Other Mortgage Lengths: Alternatives to Consider

Not every homeowner fits into the standard 15- or 30-year mold. Fortunately, other terms provide flexibility based on unique needs:

20 year mortgage rates and 20 year fixed mortgage rates strike a balance between the affordability of a 30-year loan and the savings of a 15-year loan.

25 year mortgage rates offer slightly lower monthly payments than 20-year loans but still come with interest savings compared to a 30-year mortgage.

10 year ARM mortgage rates and 10 1 ARM rates today provide low initial interest rates with adjustments later. These are ideal for borrowers planning to move or refinance before the rate resets.

2 year fixed home loan rates and 2 year mortgage rates are short-term loans often used for bridge financing or unique scenarios.

1 year fixed mortgage rates and 1 year mortgage rates are rare but sometimes available in niche financial products.

These less common terms offer specialized benefits but may not be suitable for the average borrower unless paired with a specific financial strategy.

How to Choose the Right Mortgage Length

Choosing the right mortgage length requires a careful look at your financial situation, goals, and risk tolerance. Here are some factors to consider:

1. Monthly Budget

Can you comfortably afford higher monthly payments? If so, a shorter term like 10 or 15 years might make sense.

If you need lower monthly payments, a 30 year mortgage is likely more appropriate.

2. Total Interest Paid

Shorter loans mean less interest overall, even if your monthly payment is higher.

Use tools like a 15 year mortgage refinance calculator or 10 year mortgage rates calculator to see how much you can save.

3. Long-Term Plans

Planning to stay in your home long-term? A fixed-rate mortgage like a 15 year fixed mortgage or 30 year fixed mortgage offers stability.

Planning to sell or refinance in a few years? Consider an ARM product like 10 1 ARM rates today.

4. Current Market Rates

Compare current fixed mortgage rates and current fixed rate mortgage rates across different loan terms.

Rates fluctuate based on market conditions, so it’s important to lock in a favorable rate when you find one.

5. Your Age and Life Stage

Younger buyers may prefer longer terms for affordability.

Older buyers nearing retirement may favor shorter terms to become mortgage-free sooner.

Final Thoughts

Understanding home loan mortgage rates and the variety of available loan terms is key to making a smart home financing decision. While 30 year mortgage rates offer long-term affordability, shorter terms like 15 year mortgage rates, 10 year mortgage rates, and even 20 year mortgage rates provide opportunities for faster payoff and interest savings.

Don’t overlook non-traditional options like 25 year mortgage rates, 2 year mortgage rates, or adjustable-rate loans like 10 year ARM mortgage rates if they align with your financial strategy. Whatever your goals, be sure to explore all the available tools—such as the 15 year fixed mortgage rates calculator—to understand how different terms will affect your budget and long-term wealth.

By evaluating your income, expenses, and future plans, you can choose the mortgage length that best supports your financial success.

For Utah’s veterans and active-duty service members, the dream of homeownership is more than just a dream—it’s a benefit you have earned through your dedicated service. As we navigate the housing market in 2025, the VA home loan stands out as the single most powerful tool for service members looking to purchase a home. This is more than just a mortgage; it’s the definitive veteran home loan, designed to provide a direct and affordable path to your front door.

Many potential buyers feel the biggest hurdle is the upfront cost. But what if we told you there’s a proven path that eliminates that barrier entirely? This guide will show you exactly how to get a VA home loan, transforming a complex process into a clear, actionable plan.

The Unbeatable Benefits of a True No Down Payment Mortgage

The cornerstone of the VA loan program is its most famous feature: it is a true no down payment mortgage. While most loan types require thousands of dollars saved up front, the VA program allows you to finance 100% of the home’s purchase price. This is made possible by a guarantee from the U.S. Department of Veterans Affairs.

This benefit alone can accelerate your homeownership timeline by years. But it doesn’t stop there. Unlike FHA or conventional loans with low down payments, a VA loan with zero down does not require monthly mortgage insurance (PMI). This can easily save you hundreds on your monthly payment. For a complete overview of all the benefits you’ve earned, you can visit the official U.S. Department of Veterans Affairs Home Loan Page.

Understanding Today’s VA Loan Rates

When you begin your research, you’ll naturally focus on interest rates. You will likely see several terms, such as VA mortgage rates or the more general VA loan rates. It’s important to know that the current VA loan rates you see advertised online are benchmarks—the average VA loan rate available on a given day.

Your personal rate will be determined by your unique financial profile, credit history, and the state of the market when you lock. To find out what VA home loan rates you may qualify for, the best course of action is to speak directly with a mortgage professional.

Your Step-by-Step Guide: How to Apply for a VA Home Loan

So, you’re ready to move forward? Here is a clear breakdown of how to apply for a VA home loan and secure your financing.

Step 1: Partner with the Best VA Loan Lenders

Your first and most crucial decision is choosing the right lending partner. The best VA loan lenders are those who specialize in the VA home loan process and can navigate its guidelines with ease. While you may recognize large national companies like Veterans United Home Loan, there is immense value in working with local VA home loan lenders. A Utah-based expert understands the local market and can offer the personalized, hands-on service that makes all the difference.

Step 2: The All-Important Pre-Approval

Before you start scheduling home tours, your top priority is to get pre approved for a VA home loan. A VA home loan pre approval is a formal letter from your lender stating that you are financially qualified for a loan up to a specific amount. This is the document that turns you into a serious buyer, giving you the power to make a confident offer when you find the perfect home. The pre-approval process begins with a simple conversation with a trusted loan officer.

Step 3: The Formal Application

Once you have a home under contract, you will officially apply for VA home loan. This involves completing the formal VA home loan application and providing key documents. Chief among these is your Certificate of Eligibility (COE), which you can typically retrieve instantly through your lender or via the VA’s official eBenefits Portal at va.gov. For a more detailed explanation of the application process, see our previous article, VA Home Loans Made Easy, Your Guide to Buying in Utah.

Budgeting for Your Loan: Costs, Fees, and Calculators

A successful home purchase is all about confident financial planning.

Estimate Your Payments: To get a feel for your budget, it’s wise to use an online calculator. Whether you search for a VA loan calculator, a VA home loan calculator, or a VA mortgage calculator, these tools all provide the same crucial function: estimating your all-in monthly payment. While helpful for estimates, a personalized quote from a loan officer will always be most accurate.

The VA Funding Fee: To keep the program running for future generations, most borrowers will pay a one-time VA Funding Fee. This fee varies and can be rolled into your total loan amount to avoid another out-of-pocket expense. Your loan officer can give you a detailed breakdown of this fee.

Closing Costs: While there’s no down payment, every real estate transaction has VA loan closing costs (#17). These are fees for services like the appraisal and title work. The great news is that the VA limits what lenders can charge veterans and even allows you to negotiate for the seller to pay them on your behalf.

Beyond the Purchase: The Power of a VA Refinance

The VA loan benefit doesn’t end after you buy a home. A VA refinance can be an incredibly powerful tool for current homeowners.

The most popular option is the Interest Rate Reduction Refinance Loan (IRRRL), a streamlined way to lower your interest rate and monthly payment. For those who want to tap into their home’s equity, the VA cash out refinance lets you borrow against your home’s value to get cash for debt consolidation, home improvements, or other major life expenses. Your loan officer can walk you through the specifics of each refinance option to see if one is right for you.

Your VA home loan benefit is a testament to your service. It is a powerful key to unlocking the door to homeownership in Utah. To get started, connect with a dedicated loan officer today.

Discover the best first-time home buyer programs in Utah, including FHA, VA, and USDA loan options. Learn how to get pre-approved, compare rates, and calculate what you can afford.

Utah FHA Loan Requirements

One of the most popular choices for new buyers is an FHA loan. These government-backed loans come with lower down payment requirements and more flexible credit standards. If you’re a first-time buyer with limited savings or lower credit, you’ll want to understand the **Utah FHA loan requirements**.

To qualify, you’ll typically need: – A **minimum credit score for Utah** FHA loans of 580 (or 500 with a larger down payment) – A debt-to-income ratio below 43% – Proof of steady income and employment

Utah VA Loan Rates and Benefits

If you’re a veteran, active-duty military member, or eligible spouse, you might qualify for a VA loan. **Utah VA loan rates** are often lower than conventional loans, and you won’t need to pay private mortgage insurance (PMI).

VA loans also require no down payment in most cases—making it one of the best programs for eligible first-time buyers.

Utah USDA Home Loans for Rural Buyers

Looking outside the city? **Utah USDA home loans** are designed to support buyers in rural areas. They offer 100% financing (no down payment) and reduced mortgage insurance.

To qualify, the home must be in a USDA-eligible area, and your income must fall below local limits.

Compare Mortgage Rates Utah

Don’t just settle for the first lender you find—**compare mortgage rates Utah** to find the best deal. Rates vary daily, so keep an eye on: – **Mortgage rates today** – **Mortgage rates in Utah today** – **HELOC rates Utah** if you’re considering a home equity line

Use a **mortgage calculator Utah** or **refinance calculator Utah** to estimate your monthly payments and compare loan scenarios.

Pre Approval Mortgage vs Prequalified

Before house hunting, get a **pre approval mortgage** to show sellers you’re serious. But what about being **prequalified**?

Here’s the difference: – **Prequalified** = rough estimate based on unverified data – **Preapproved** = verified loan offer based on your financial info and credit

How Much House Can I Afford Utah?

Use tools like a **mortgage calculator Utah** to answer: **how much house can I afford Utah**? Most lenders recommend your housing costs stay under 28% of gross income.

Should I Refinance My Mortgage in Utah?

Even first-time buyers should think long-term. If rates drop later, consider: – **Best refinance rates Utah** – **Refinance calculator Utah** – **Should I refinance my mortgage in Utah**

Refinancing can lower your monthly payment or change your loan type from **fixed vs variable mortgage Utah**.

Jumbo Loan Rates Utah

For high-priced homes, consider **jumbo loan rates Utah**. These loans may require a higher **minimum credit score for Utah** and a bigger down payment.

Best Time to Buy a House in Utah

Timing your purchase can save you thousands. The **best time to buy a house in Utah** is typically fall or winter, when there’s less competition and sellers are more motivated.

Final Thoughts

Buying a home in Utah for the first time can be exciting and affordable with the right tools. Whether you’re checking **equity loan rates**, comparing **HELOC rates today**, or browsing the **best mortgage lenders in Utah**, preparation is everything.

Talk to a trusted **mortgage broker Salt Lake City**, get **pre approval mortgage**, and take the first confident step toward your new home.

Best Mortgage Options for First-Time Home Buyers: How to Choose the Right Loan for Your Situation

Buying your first home is one of the most important financial milestones you will ever reach. While it can be exciting, it can also feel stressful and overwhelming. The good news is there are many options to help you find the best first-time home buyer mortgage, whether you have perfect credit or you need extra support to get started. This guide will walk you through the most common loans and programs, and help you feel more confident choosing the right option for your needs.

FHA Loan for First Time Buyers

One of the most popular choices is an fha loan for first-time buyers, which is backed by the Federal Housing Administration. These loans have flexible requirements and low down payment options, making them ideal for first-time borrowers who may have a limited savings history or a lower first-time home buyer credit score. FHA loans often allow down payments as low as 3.5%, helping more people buy a home without waiting years to save. They also allow more flexible debt-to-income ratios, which can make it easier for you to qualify even if you have student loans or other debt.

How to Get a Mortgage as a First Time Buyer

Understanding how to get a mortgage as a first-time buyer can save you stress and money. Start by checking your credit score and pulling your credit report for free. Many lenders will want to see at least a 620 score, but some programs accept lower scores. Next, gather your financial paperwork, including income statements, tax returns, and other document requirements for first-time buyer loans. Securing pre approval for first-time buyer mortgages is a smart way to show sellers you are serious and ready to close.

Make sure you compare lenders. Some of the best banks for first-time buyer loans offer unique programs, while credit unions or online lenders may have better rates. Always check the current first-time home buyer interest rates, since even a half-percent difference can change your payment dramatically over time.

Step-by-Step Mortgage Checklist

First Time Buyer Loan Checklist

1.) Understand the first-time buyer loan requirements for each type of mortgage 2.) Explore down payment assistance for first-time buyer grants or programs 3.) Ask about afirst-time home buyer mortgage program options through your state or city 4.) Budget for first-time home buyer closing cost, typically 2%–5% of the home’s price 5.) Research first-time buyer mortgage low income programs if your income is modest 6.) Decide if a first-time home buyer fixed rate mortgage is better than an adjustable-rate 7.) Learn how to apply for a first home loan and what paperwork is needed

Following these steps makes the entire first time home buyer loan process easier, giving you peace of mind.

VA and USDA Loans for First Time Buyers

A VA loan for first-time buyers is one of the best benefits for veterans, active-duty military, and eligible family members. These loans do not require a downpayment and have no private mortgage insurance, making home ownership more affordable. If you live in a rural or eligible suburban area, a usda loan for first-time buyers could be an amazing choice. USDA loans also offer no down payment, but do have income restrictions and property location rules. These programs can open the door to buying a home for many families who thought it was out of reach.

First Time Buyer Choosing a Mortgage: Mistakes to Avoid

Choosing a mortgage can feel complicated, but avoiding these mistakes will help you succeed. First, don’t rush through the process without researching rates. Always check first-time home buyer interest rates with multiple lenders and compare them carefully. Second, never skip the home inspection, even if the market is hot. Skipping inspections can lead to costly surprises later.

Don’t overextend your budget by taking the largest loan you qualify for. Instead, calculate how much a first-time buyer can borrow but only spend what you can truly afford. Check the details of how to qualify for first-time buyer program incentives that could lower your payment. Finally, work only with best lenders for first-time home buyers who understand your needs and will communicate clearly.

Ready to Start?

If you’re feeling ready to move forward, take the next steps now. Compare rates, apply for pre approval for first-time buyer programs, and research first time home buyer mortgage program options that match your financial picture. Use a reliable mortgage calculator to see how rates and fees affect your payment.

Ask questions about first-time buyer loan requirements, gather your paperwork, and start conversations with trusted lenders. With the right plan, you can confidently move through the first-time home buyer loan process and make your dream a reality. The best mortgage for first-time home buyers is achievable if you stay organized, get expert advice, and understand your options. For additional resources, visit the HUD First-Time Buyer Resourcespage.

Whether you’re a first-time buyer or looking for a fresh start, understanding FHA loan requirements in Utah is the first step toward homeownership. From checking your credit and saving for a down payment, to comparing FHA loan limits and choosing the right lender, this guide will help you navigate the FHA mortgage process in Utah with confidence.

Know What FHA Lenders Want

Understanding basic requirements for an FHA loan is essential. These are some of the requirements:

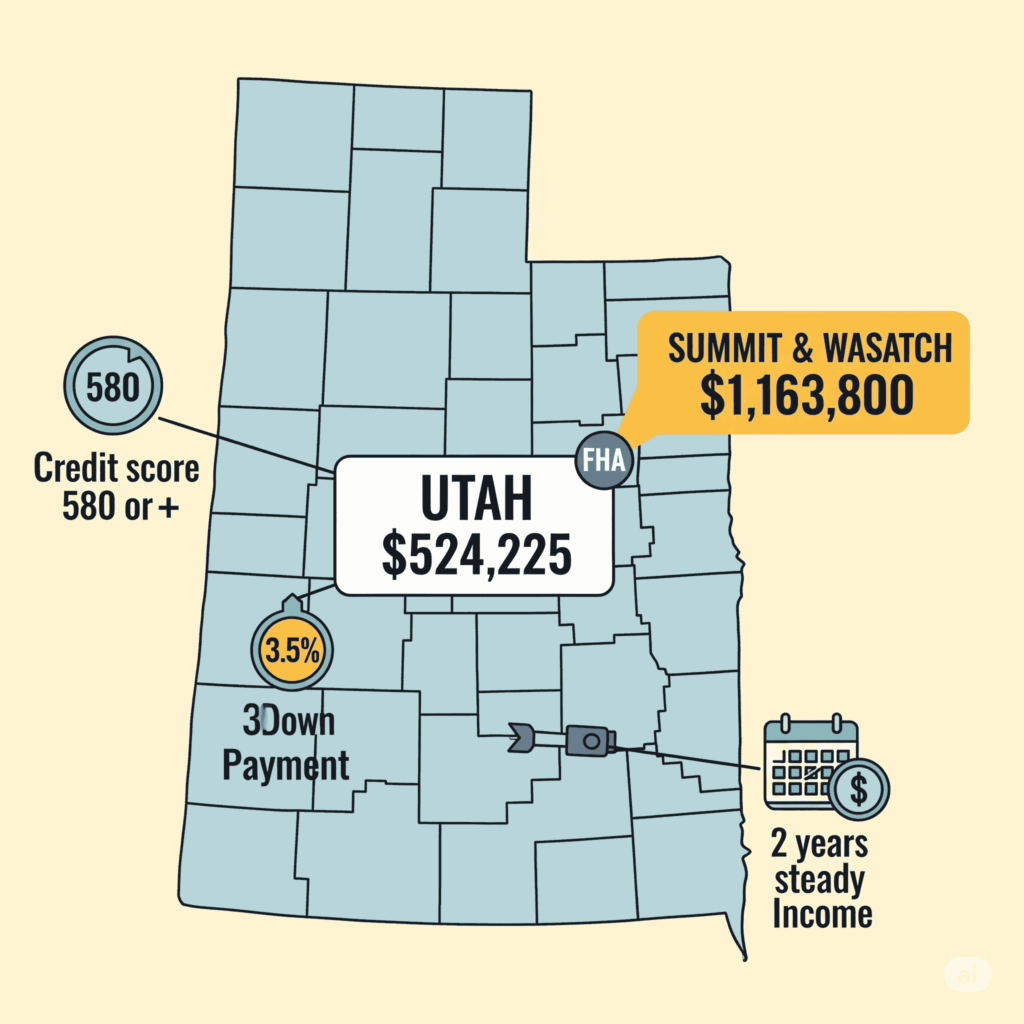

Credit Scores: 580+ for 3.5% down: 500-579 requires 10% down.

Income: At least 2 years of steady employment rates.

Debt-to-Income: Usually 43% or less.

Residence: This must be your primary residence.

Mortgage Insurance: This is an upfront premium and annual MIP apply.

FHA Loan Limits You Should Know About

FHA loans are county-specific and have maximum loan amounts that you can borrow. Knowing you FHA loan local limits is essential in avoiding unwanted surprises:

Most Utah counties have a limit around $524,225 for single-families.

High-counties like Summit and Wasatch County allow uo to $1,163,800

Check the current limits on the HUD website or with your lender.

Getting Pre-Approved For FHA Loans

Getting pre-approved is a crucial step that tells sellers you’re a serious buyer. This also helps you understand your borrowing power before you go house hunting.

Make sure to submit your financial documents online.

Establish a buget amount and receive a loan amount.

By completing these steps this will accelerate your buying process once you find the right home for you.

Calculating Your Payments for FHA Loans

It is essential to use an FHA mortgage calculator to estimate your monthly payments. This also includes the principal, interest, taxes, insurance, and mortgage insurance premiums. This will help you budget realistically to find your dream home!

City Creek Mortgage Utah FHA Calculator:

Allows you to customize for 15, 20, or 30-year terms and has detail reports for county-specific loan limits

NerdWallet Utah Mortgage Calculator:

Allows you to get a breakdown of estimated payments and see what the annual amortization rates are for Utah homes.

Zillow Mortgage Calculator:

Quickly estimates what the potential prinicpal, interest, taxes, and insurance is depending on your location.

Comparing Lenders & Rates for FHA Loans

It is important to look around and find the best options for FHA mortgage rates and credible lenders with experience in Utah that align with your options. Local lenders also might offer special programs and perks based on certain requirements. Make sure to look for good customer reviews about FHA expertise and choosing Utah-specific lenders may provide faster service or benefits.

Lower Credit Score?

If your credit score is below 580, don’t fret, there are still options for FHA loans. However, here are some things you might be to do to compensate:

Consider putting down 10% if your credit score is lower.

Make sure to check your credit report for any errors and pay any debts.

Avoid any new credit inquiries before applying for an FHA loan.

Game Plan for First-Time Homebuyers

To conclude, make sure to follow these steps to stay organize and help maximize your chances for being approved for a FHA loan:

Get pre-approved for your loan early.

Verify the county FHA loan limit for where you are looking to buy.

Compare different rates from potential lenders.

Utilize FHA loan calculators to estimate payments.

Prepare all of the necessary financial documents.

Work on improving your credit score if needed.

Securing an FHA loan in Utah is an achievable thing for all first-time buyers or those with a less-than-perfect credit score. By understanding what lenders are looking for, checking local limits, getting pre-approved, comparing rates, and calculating potential payments, you’ll be prepared to make confident decision to lead you to becoming a homebuyer!

VA Home Loans: Your Simple Guide to Getting a Home

For millions of people who served in the military, owning a home can become a reality much more easily thanks to VA home loans. These special home loans are backed by the U.S. Department of Veterans Affairs. They offer big advantages to help military families buy homes, showing our country’s appreciation for their service. Unlike regular home loans, a veteran home loan ismade available only to those who served, making it a key benefit for eligible service members. Unlike most traditional loan options military home loans allow eligible buyers to purchase a home without any down payment and no private mortgage insurance, make it an amazing option for members of the Veteran community. This guide to VA home loans will walk you through everything you need to know about getting a VA mortgage, from figuring out if you qualify, to applying for the loan, checking out ways to refinance, and understanding the costs.

Who Can Get a VA Home Loan and What Are the Benefits?

Starting your path to a VA home loan means first understanding VA home loan eligibility – basically, who can get one. Generally, if you’re on active duty, a veteran, a National Guard member, or a reservist, you may qualify. In some cases, certain surviving spouses can too. The exact rules depend on when and how long you served, and your discharge status. Your first important step is getting a Certificate of Eligibility (COE) from the VA. This paper proves to lenders that you meet the VA’s service requirements. Once you qualify, the VA home loan benefits are fantastic. The biggest plus is often the VA loan no down payment option. This means you can borrow the full price of the home, and don’t need to save up a large sum of money upfront. This can be a huge help, especially when homes are expensive and saving for a down payment is tough. Also, VA loans don’t require Private Mortgage Insurance (PMI). Regular loans usually make you pay PMI if you put less than 20% down. Getting rid of this monthly cost makes owning a home cheaper over time.

Even though there’s no PMI, you should be aware of the VA funding fee. This is a one-time fee paid to the VA that helps cover the cost of the loan program. How much you pay depends on things like your service type, the type of loan, and if it’s your first time using this benefit. Besides these money-saving perks, VA loans often have easier credit rules than regular loans. Lenders will still check your credit, but the rules can be more flexible. VA loans also offer competitive VA loan rates, which we’ll talk about next. This makes the overall cost of borrowing less expensive for service members and veterans. For more details on who qualifies and what you get, visit the official VA Home Loans website. The support from the Department of Veterans Affairs home loan program is there to help those who served reach their dream of owning a home with less hassle and fewer money worries.

How VA Loan Rates Work and How to Apply

When thinking about a VA mortgage knowing about and keeping up with current VA loan rates is important. These rates are usually very good, and often lower than rates for regular loans, because the VA guarantees part of the loan to the lenders. The rates do change with the market so in order to make sure you’re getting the best rate shop around and compare offers from different lenders. Besides rates, the process to apply for VA loan is pretty straightforward. You’ll need to gather financial papers like proof of income, job history, and bank statements, just like with other home loans. But with a VA loan, you’ll also give your COE to your chosen lender.

The application usually kicks off with a VA loan pre-approval or VA mortgage prequalification. Pre-approval is a more thorough check of your finances by a lender, giving you a better idea of how much you can borrow. This will allow you to set your budget and help the process move faster once you find a home. Picking the right VA mortgage lenders is also key. Not all lenders specialize in VA loans, so in order for things to run smoothly it’s important to find one with experience, who knows all the ins and outs of the program. Once you send in your application and all your documents, the lender will work towards your VA loan approval. They’ll get an appraisal to make sure the home meets VA rules, and check your finances to ensure you meet all the VA loan requirements. For more on how to apply and pick a lender, helpful sites like USAA offer good advice.

Handling Your VA Mortgage: Refinancing and Other Costs

If you already have a VA mortgage, and are looking to refinance there are several ways to do so. A VA cash-out refinance allows you to take money out of your home’s value. You can use this cash for things like home improvements, paying off other debts, or other big expenses. This loan replaces your current mortgage with a new VA loan, possibly with new terms. Another popular choice is the VA streamline refinance, also known as an Interest Rate Reduction Refinance Loan (IRRRL). A VA IRRRL is designed to help you get a lower interest rate or change from a changing (adjustable) rate to a steady (fixed) rate with very little paperwork. It usually doesn’t need an appraisal, proof of income, or a full credit check, making it a fast and easy way to cut your monthly payments or lock in your interest rate. This makes the VA streamline refinance a very appealing choice for many.

Besides refinancing, it’s good to understand the VA loan closing costs. While VA loans skip PMI and often the down payment, you’ll still have some costs when the loan closes. These can include appraisal fees, title insurance, recording fees, and sometimes points if you pay extra to get a lower interest rate. The VA has specific rules about which fees you can pay. Sometimes, the seller can also pay some of these costs, which can save you money upfront. To help figure out these costs and what your monthly payments might be, you can use a VA mortgage calculator. These online calculators let you put in your loan amount, interest rate, and how long you’ll pay, to get an estimate of your monthly principal and interest payment. Lastly, know about VA loan limits. These are the highest loan amounts the VA will guarantee without needing a down payment for eligible borrowers who have their full entitlement. While many areas don’t have a specific limit, some expensive areas might. So, it’s smart to check the current VA loan limits for where you want to buy, on the VA’s official website.

In short, the VA home loan program is an amazing benefit. It offers big financial advantages and an easier way to own a home for qualified service members and veterans. From special perks like no down payment and no PMI, to easy refinancing and good rates, these loans are made to honor service by giving you a real, lasting asset. By understanding your VA home loan eligibility, going through the application steps, and managing your loan smartly, you can really make the most of this valuable benefit from the Department of Veterans Affairs. If you’re ready for the next step, you might want to read more detailed articles on specific topics like “Understanding the VA Funding Fee” or “Comparing VA Streamline vs. Cash-Out Refinance Options” to learn even more. For up-to-date rates and extra info, you can always visit The Military Wallet.

Navigating the mortgage landscape can be overwhelming, especially with so many loan types, lenders, and rate options. Whether you’re a first-time homebuyer, a low-income applicant, or someone searching for the best mortgage loans in Utah, understanding your options is key to securing your dream home. This guide walks you through loan types, where to find them, and how to choose the right fit for your financial situation.

Understanding the Types of Mortgage Loans

Before diving into specific programs, it’s essential to understand the various mortgage loan types. The most common include:

These types of mortgage loans serve a variety of borrowers, from those with excellent credit to those with non-traditional income sources.

Low Interest Mortgage Loans: A Smart Financial Move

Low interest mortgage loans can save you thousands over time. They’re especially beneficial when rates are low. If you’re asking, “When will mortgage rates go down?” monitor the market closely and lock in rates during dips. Credit union mortgage loans often come with lower interest than traditional bank loans, making them a smart alternative.

Best Mortgage Loans for First-Time Buyers

First time mortgage loans help ease the financial pressure for new homeowners. Many Utah programs offer 0 down and low income mortgage loansto support first-time buyers. These easy mortgage loans are often backed by state or federal programs, reducing risk for lenders and improving access for borrowers.

No Income and Bank Statement Mortgage Loans

For self-employed individuals or those with variable income, traditional mortgage applications can be difficult. This is where bank statement mortgage loans and no income mortgage loans come into play. These options allow you to qualify based on your financial history rather than your W-2 or tax returns.

Guaranteed and Reverse Mortgage Loans

Guaranteed mortgage loans, such as those backed by FHA or VA programs, offer added security. For older homeowners, the best reverse mortgage loans let you access home equity without moving. This option can support retirees who need extra income.

Different Mortgage Loans for Unique Needs

Every borrower is different, which is why different types of mortgage loans exist. From cheap mortgage loans to applying for multiple mortgage loans at once, having choices ensures you find a loan tailored to your situation. For example, some may benefit more from low interest rate mortgage loans, while others seek easy to get mortgage loans with minimal paperwork.

Finding the Best Mortgage Loans Near Me

When searching for the best mortgage loans near me, consider working with top lenders for mortgage loans in Utah. These include national banks, local credit unions, and specialized mortgage companies. Some of the best companies for home mortgage loans have robust online platforms, transparent terms, and personalized service.

Best Way to Apply for Mortgage Loans

The best way to apply for mortgage loans is by preparing your financial documents in advance, comparing loan products, and getting pre-approved. Many online platforms make it easy to apply, while local mortgage brokers can offer tailored advice. Applying for multiple mortgage loans can also help you compare offers and choose the most favorable terms.

Compare Top Utah Lenders

Top Utah mortgage lenders offer competitive rates and strong customer service. Look for lenders with great reviews, responsive loan officers, and a variety of options like low income, first-time buyer, and 0 down mortgage loans. You can explore options via Utah Housing Corporation and local credit unions like Mountain America Credit Union.

Mortgage for Bad Credit: Is It Possible?

Yes, you can still qualify for a mortgage for bad credit. Many lenders offer programs specifically designed for those with credit challenges, including FHA and subprime loans. These easy to get mortgage loans typically come with higher interest rates, but they provide a pathway to homeownership while rebuilding your credit.

Monitoring Rates: When Will Mortgage Rates Go Down?

One of the most frequently asked questions is, “when will mortgage rates go down?” While no one can predict the market perfectly, keeping an eye on economic indicators, inflation data, and Federal Reserve decisions can help you time your application for the most favorable outcome.

Conclusion: Your Roadmap to the Best Mortgage Loans

From low interest mortgage loans to bank statement mortgage loans and everything in between, the Utah mortgage market offers a wealth of options. By understanding the different mortgage loans available and aligning them with your financial needs, you can secure the best mortgage loans for your situation. Whether you’re searching for mortgage loans near me, applying for multiple mortgage loans, or seeking mortgage for bad credit, being informed is your best asset.

Explore your options, connect with top lenders for mortgage loans, and take the next step toward homeownership today.