Owning rental property offers numerous tax benefits of owning a rental property that can significantly boost your financial success as an investor. By understanding and utilizing strategies such as depreciation on rental property, effectively managing capital gains tax on investment property, and implementing smart real estate tax strategies, landlords and investors can minimize their tax burden while maximizing profits.

Maximizing Rental Property Tax Deductions and Depreciation Benefits

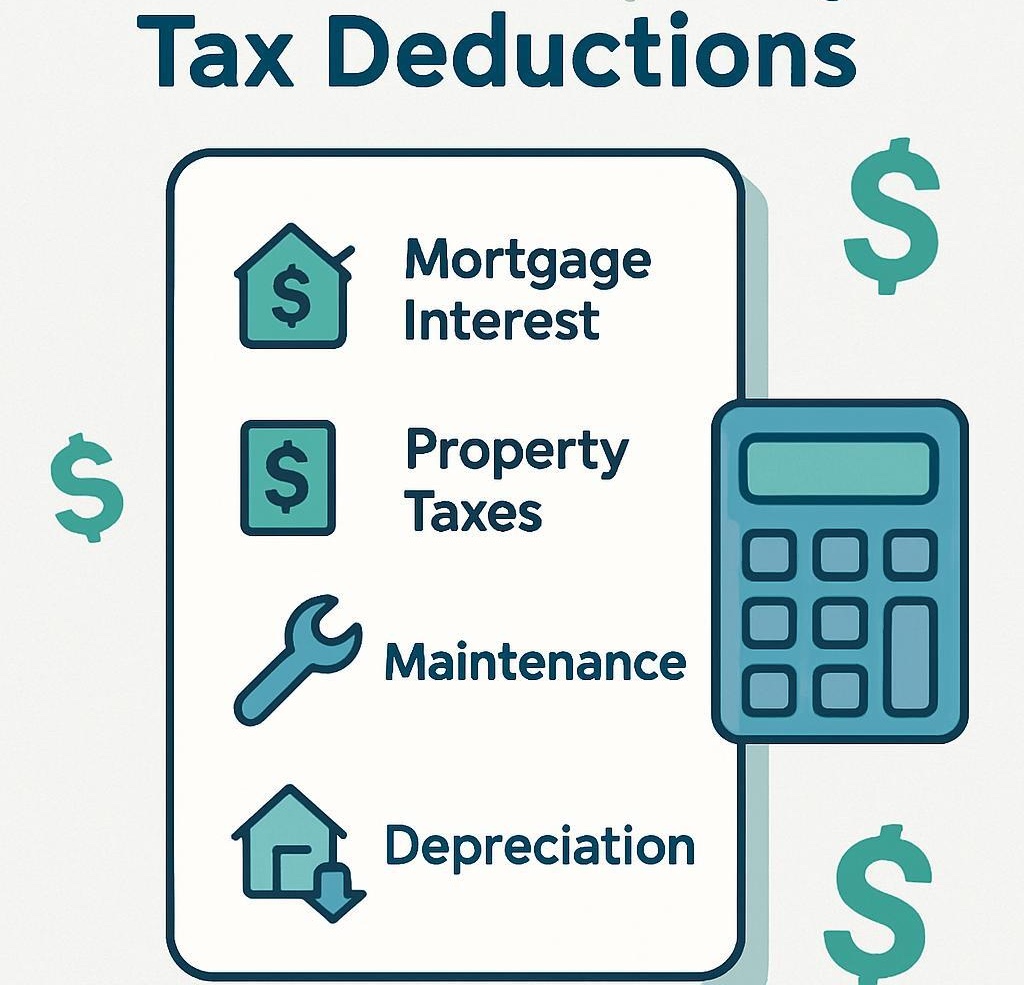

One of the most valuable tax benefits of owning a rental property is the ability to claim deductions including depreciation on rental property, which allows you to deduct the cost of the property over time. In addition to depreciation, a comprehensive rental property tax deductions checklist covers mortgage interest, maintenance, and property taxes deduction limits. However, it is important to be aware of real estate depreciation recapture, which can impact taxes when selling the property.

Capital Gains Tax Insights and Utilizing 1031 Exchange Rules

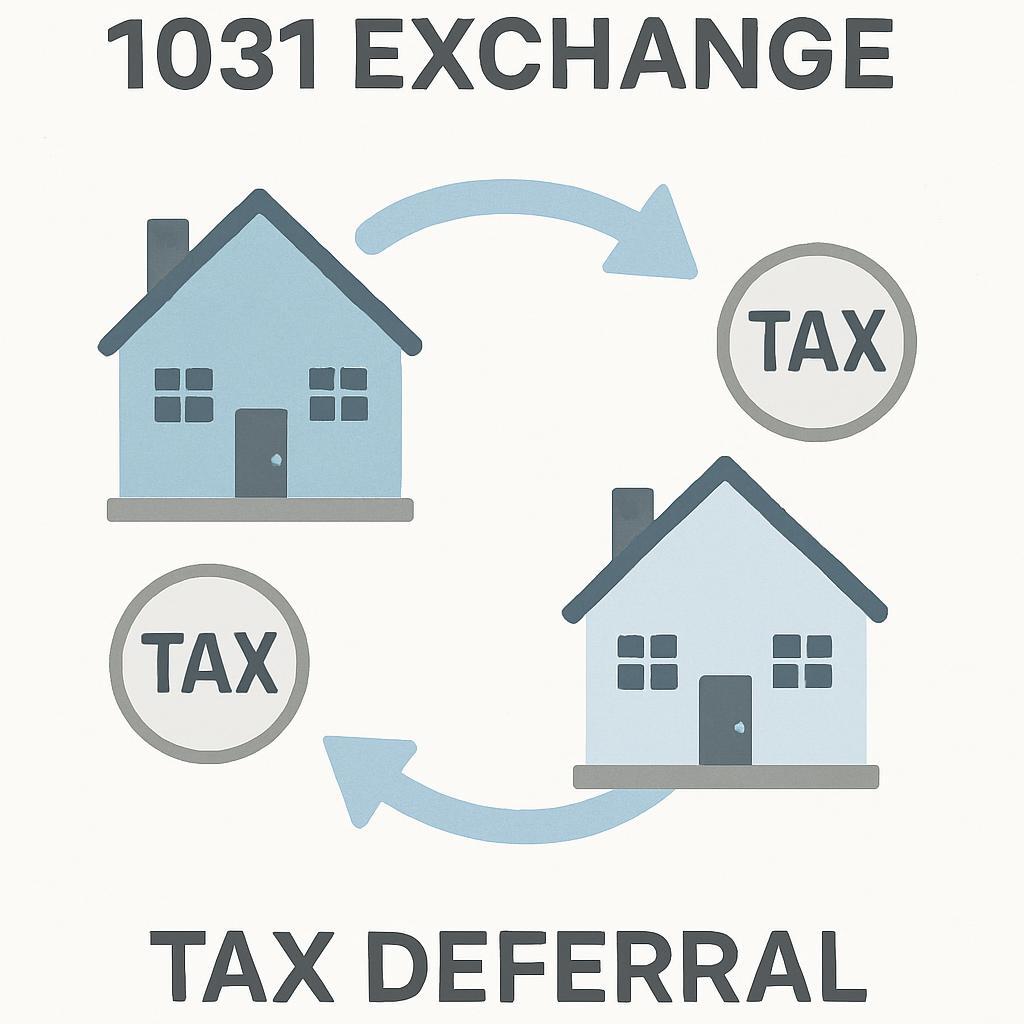

When selling an investment property, understanding capital gains tax on investment property is essential. Tax rates vary between short-term capital gains real estate and long-term capital gains real estate, affecting your overall tax liability. Smart investors utilize 1031 exchange rules to defer these taxes by reinvesting in like-kind properties. Incorporating tax planning for real estate investors can help navigate these rules effectively and avoid surprises such as how to avoid capital gains tax on home sale.

Sophisticated Real Estate Tax Strategies for Investors and Landlords

Beyond deductions, advanced investors apply various real estate tax strategies like leveraging the mortgage interest deduction rental property and the qualified business income deduction real estate. Utilizing cost segregation study benefits can accelerate depreciation, while tax loss harvesting real estate can offset capital gains. Understanding how to minimize real estate taxes legally, as well as capitalizing on tax breaks for landlords and tax credits for energy efficient rental property, further improves investment outcomes.

Additional Tax Considerations and Benefits for Real Estate Professionals

Qualifying for real estate professional tax status offers significant tax advantages, enhancing deduction possibilities and income classification. Knowing the tax implications of selling a rental property and applying proven real estate investment tax tips can protect your profits. Furthermore, understanding passive income real estate tax rules ensures your investments remain tax-efficient and compliant with IRS guidelines.

Conclusion

Mastering the tax benefits of owning a rental property empowers investors and landlords to build lasting wealth through intelligent tax planning and strategic investment. By leveraging these insights, you can maximize your real estate returns while minimizing tax liabilities.

Why Utah Mortgage Rates Today Matter More Than Ever.

In today’s competitive housing market, understanding Utah mortgage interest rates for first-time home buyers is essential for making informed decisions and securing favorable loan terms.. Whether you’re a seasoned homeowner or a first-time buyer, staying current with Utah mortgage interest rates today empowers you to lock in favorable financing terms.

Mortgage rates fluctuate based on a range of economic factors, including inflation trends, Federal Reserve policy, and lender risk assessments. While national averages provide a benchmark, Utah mortgage interest rates can vary significantly across lenders. Comparing current mortgage rates, 30-year fixed and mortgage rates today, FHA at the local level helps ensure that you secure a rate tailored to your needs.

Utah Mortgage Interest Rates Trends and 2025 Forecasts

As mortgage professionals, we are often asked: What are the projections for Utah home loan rates forecast for 2025? Based on market analysis, we anticipate relative rate stability in 2025, following the fluctuations seen throughout 2024. Prospective buyers and homeowners should closely monitor Utah mortgage interest rate trends this week via trusted sources like Freddie Mac’s PMMS and Utah-based lenders such as City Creek Mortgage. Utilizing tools like a Utah mortgage refinance calculator allows you to forecast payment scenarios and assess refinancing potential as market conditions evolve.

The Best Mortgage Lenders in Utah 2025: FHA, VA, and Jumbo Loans.

Navigating mortgage products can be complex, but understanding the nuances of each option is key. When researching the best mortgage lenders in Utah 2025, consider how your financial goals align with the following programs:

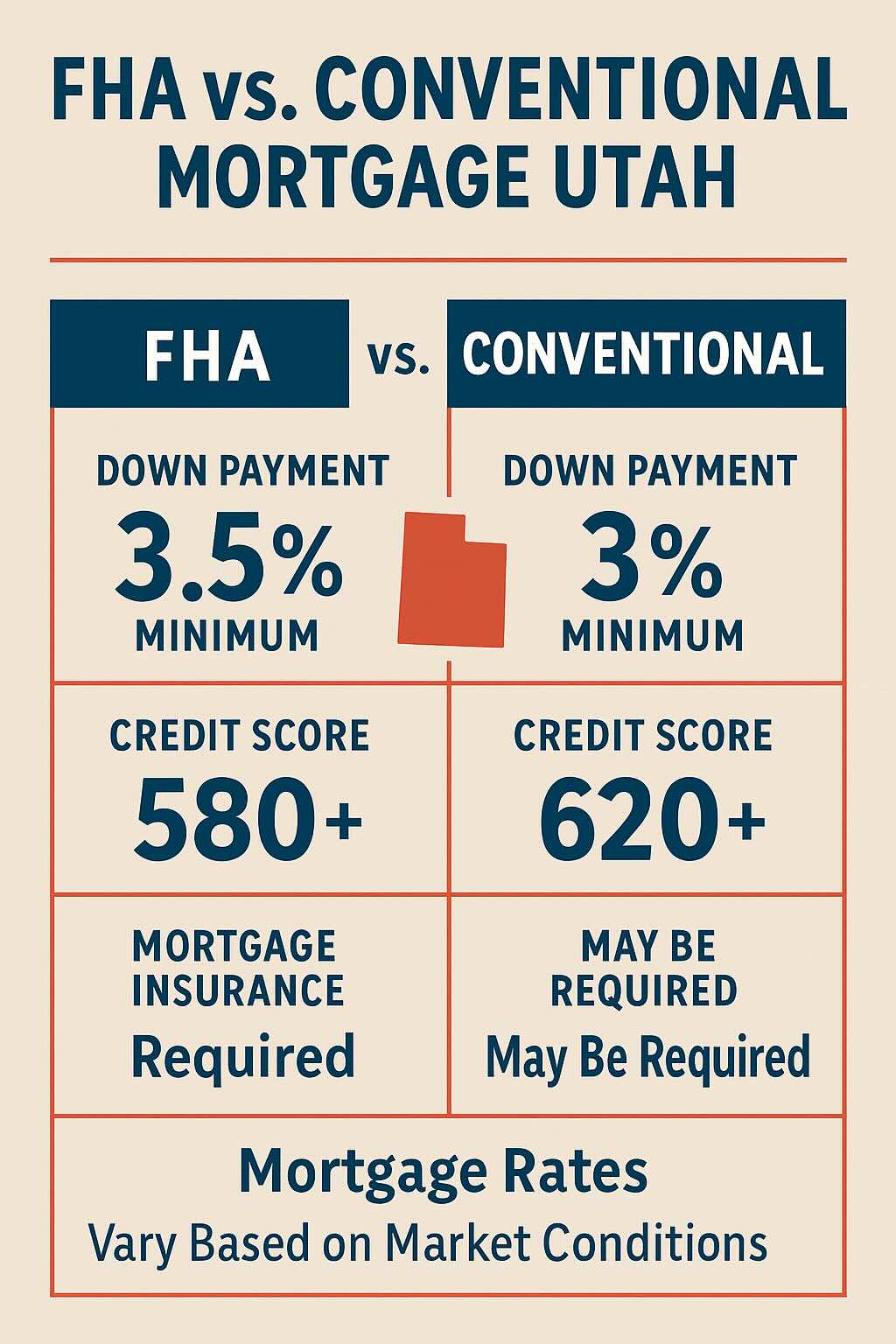

Utah FHA loan limits for 2025 have increased, allowing greater access for buyers using FHA-backed financing.

VA mortgage rates in Utah today remain a strong option for qualifying veterans, often featuring lower interest rates and no down payment.

Jumbo mortgage Utah requirements continue to evolve, with lenders requiring higher credit scores and thorough income documentation.

Those weighing FHA vs conventional mortgage Utah options should factor in long-term cost savings and qualification thresholds. For those with limited funds, programs offering Utah FHA down payment assistance provide critical support toward homeownership.

Getting Approved and Refinancing at Today’s Utah Mortgage Interest Rates

Knowing how to get approved for a mortgage in Utah includes maintaining a healthy credit profile, managing debt-to-income ratios, and collecting financial documentation early.

Homeowners evaluating mortgage rates refinance options should assess both cash out refinance Utah rates and traditional term refinancing. Not sure if it’s the right time? A Utah mortgage refinance calculator and platforms like FHA.com help clarify when to refinance mortgage Utah based on both market rates and your financial objectives.

Utah Mortgage Tools: Use These Calculators Before You Buy Before starting the home search, utilize tools that help shape your financial expectations.

A mortgage payment calculator Utah estimates your monthly obligation, while a home affordability calculator Utah factors in income, debt, and projected interest rates.

These resources are especially valuable if you’re exploring home equity loan interest rates or considering a move into Utah’s housing market for the first time.

FAQ – Utah Mortgage Interest Rates

Q: What are the current Utah mortgage rates for first-time buyers? A: Rates vary based on credit score, loan type, and market conditions. First-time buyers may qualify for competitive FHA and VA rates.

Q: Are Utah mortgage rates expected to drop in 2025? A: Based on current forecasts, experts anticipate a stable or slightly declining trend in interest rates through mid-2025.

Buying a home is one of the biggest financial decisions you’ll ever make and understanding how the application for a mortgage is the first step in making it happen. Whether you’re a first-time buyer or looking to refinance or expand your investment portfolio with a commercial mortgage, this guide is tailored to help Utah residents navigate the home loan process.

We’ll walk you through key considerations, calculators, and strategies for finding the best mortgage rates and lenders. From application tips to mortgage calculators, this comprehensive resource covers it all.

Before you get started, it’s important to understand some basic terminology and what the process looks like for different types of borrowers.

What Is a Mortgage and How Does It Work?

A mortgage is a loan used to purchase property. You borrow money from a lender and agree to repay it over time, usually with interest. Mortgages come in many forms, including fixed rate mortgage and commercial mortgage options, depending on your goals.

Check Current Mortgage Interest Rates Before You Apply

Knowing the current mortgage interest rates is crucial before you commit. Rates fluctuate daily, and even a small percentage point difference can cost or save you thousands over the life of your loan. Many buyers seek the lowest mortgage rates or cheapest mortgage rates, but those rates are often reserved for borrowers with strong credit and a solid financial profile.

You can also check out 30 year mortgage rates today to compare longer-term options, which are among the most popular mortgage terms for homeowners.

How to Find the Best Mortgage Companies in Utah

Finding the best mortgage companies in Utah can help you secure better terms and a smoother process. Compare lender reputations, rates, and fees. Don’t hesitate to get multiple offers so you can choose the best mortgage rates available to you.

If you’re a veteran, consider a VA mortgage, which offers more favorable terms like lower interest rates and no down payment requirements.

Use Mortgage Calculators to Estimate Your Budget

Before you apply for a mortgage, it’s smart to assess what you can realistically afford. Use tools like:

Mortgage payment calculator

Monthly mortgage calculator

Home affordability calculator

Mortgage estimator

These calculators help you estimate your monthly payments, how much you can borrow, and how various down payments affect your financial picture.

You can also try a bankrate mortgage calculator or free mortgage calculator for different scenarios.

Prequalify for Mortgage: What You Need to Know

Getting prequalified for mortgage gives you a sense of what a lender might offer you based on basic financial information. This is a key step before house hunting and signals to sellers that you’re a serious buyer.Lenders will review your income, credit score, debts, and assets. From there, they may issue a mortgage approval calculator result or a prequalification letter.

How to Apply for a Mortgage in Utah: Step-by-Step

When you’re ready to apply for a mortgage, be prepared with documentation like pay stubs, tax returns, and bank statements. The mortgage application process can vary slightly by lender, but generally follows these steps:

Fill out the official loan application.

Submit all required documents.

Wait for the lender to underwrite your application.

Receive a loan estimate and closing disclosure.

Close the loan.

If you’re a first-time buyer, ask questions about each step. Many lenders offer special first time buyer mortgage programs with lower interest rates, flexible terms, or reduced down payment requirements.

Considering a Commercial Mortgage? Here’s What to Know

If you’re planning to invest in property or start a business, you’ll likely need a commercial mortgage. These differ from residential mortgages in structure, repayment terms, and qualifications. Use a commercial mortgage calculator to determine what type of loan fits your business model.

Review the Average Mortgage Rate and Loan Details

It’s not just about the rate. Pay attention to loan fees, private mortgage insurance (PMI), and any terms that could impact your monthly payments or total loan cost. Check what the average mortgage rate is nationally and locally to compare.

Also, consider whether a fixed rate mortgage works better for your situation than an adjustable-rate mortgage, especially if you plan to stay in your home long-term.

Final Thoughts: Get Started with a Home Mortgage in Utah

Whether you’re exploring options for a home mortgage, investing in real estate, or looking for the best mortgage companies in Utah, being informed is your best tool. Use every resource at your disposal—from calculators and comparison tools to expert advice—to make the best decision.

Understanding how to get a mortgage is a crucial life skill. With the right guidance and preparation, you’ll not only find the best mortgage rates but also gain financial confidence in your decision.If you’re ready to begin your journey, try a mortgage estimator or get in touch with a Utah-based lender today to prequalify for mortgage and take the first step toward homeownership.

If you’re planning to buy a home in Utah, getting mortgage pre-approval is one of the smartest first steps you can take. Whether you’re a first-time homebuyer or just looking to better understand the process, this guide will walk you through everything from the mortgage approval process to an actionable application checklist. We’ll also cover FHA loan requirements, down payment assistance programs, and how to apply for a mortgage the right way.

Why Pre-Approval Matters

A mortgage pre-approval is more than just a helpful estimate—it’s a green light that shows sellers and agents you’re serious and financially ready. It also helps you understand how much home you can afford, what your mortgage interest rate might be, and which mortgage lenders or brokers near you are best for your situation.

Mortgage Pre-Approval Checklist

Before applying for pre-approval, gather the following documents and information:

Proof of income (pay stubs, W-2s, tax returns for 2 years)

Bank statements (checking, savings, investment accounts)

Employment verification (current and past employer details)

Credit score and history

Photo ID

List of debts (student loans, credit cards, auto loans)

Down payment amount and source

If you’re self-employed, you’ll likely need to provide:

Two years of personal and business tax returns

Profit and loss statements

1099 forms or bank deposits as proof of income

Pro tip: Lenders may also ask for explanations of large deposits or credit inquiries, so keep records handy.

Understanding the Mortgage Approval Process

Here’s a quick look at the typical mortgage approval timeline in Utah:

Pre-Qualification (Optional): A soft look at your finances, often done online using a mortgage calculator or by submitting estimated income and credit score.

Pre-Approval: A more thorough process involving document review and a credit check.

Loan Estimate Issued: You’ll receive details about estimated interest rate, monthly payments, and closing costs.

Underwriting: A formal risk analysis by the lender that verifies income, employment, credit, and assets.

Final Approval & Closing: Once underwriting is complete, the lender issues final approval and you move to closing.

Choosing the Right Mortgage Lender or Broker in Utah

When shopping for a home loan, it’s smart to compare offers from different lenders. Use tools to get a mortgage quote, but make sure you understand what’s behind the numbers. Ask each lender about:

Current interest rates

Whether the loan is fixed or variable

Points or fees to buy down your rate

Whether they offer FHA, VA, or USDA loans

Utah-specific grants or down payment assistance programs

Keyword tip: Searching “mortgage broker near me” can help you find local professionals who know Utah’s market best.

FHA, VA & First-Time Homebuyer Options in Utah

Many Utah buyers, especially first-timers, qualify for government-backed loans with lower down payment requirements. Here’s a quick breakdown:

Utah Housing Corporation offers grants and second loans for down payments UHC – Utah Housing Corp

Other programs provide first-time homebuyer grants or closing cost assistance

Look into local city or county programs (e.g., Salt Lake City DPA program)

Mortgage Rate Tip: Quote vs Pre-Approval

There’s a difference between getting a mortgage quote and being pre-approved. A quote gives you an estimate based on general info. Pre-approval confirms what you’re actually eligible to borrow after document review.

Want the best of both worlds? Shop for quotes from multiple mortgage lenders—then get pre-approved with your top choice

Common Questions

How do I apply for a mortgage in Utah?

Start by gathering documents listed above, checking your credit, and comparing quotes. You can apply online, in person, or through a broker.

What credit score do I need?

Most lenders require at least a 620 score for conventional loans, but FHA allows for scores as low as 580 with 3.5% down.

Can I buy a home with bad credit?

Yes—home loans for bad credit are available through FHA programs and some local lenders. Expect higher rates and stricter terms.

What if I’m self-employed?

You’ll need at least 2 years of consistent income and detailed documentation. Many lenders offer mortgages for self-employed borrowers.

Ready to Get Pre-Approved?

The mortgage pre-approval process in Utah doesn’t have to be overwhelming. With the right checklist, knowledge of available programs like FHA loan requirements and down payment assistance, and a solid lender or broker on your side, you’ll be positioned to make confident, competitive offers on your dream home.

Use our free mortgage calculator to estimate your payments, then contact one of our trusted Utah lenders for a fast pre-approval. Whether you’re a first-time buyer, self-employed, or exploring options like VA home loans, we’re here to help.

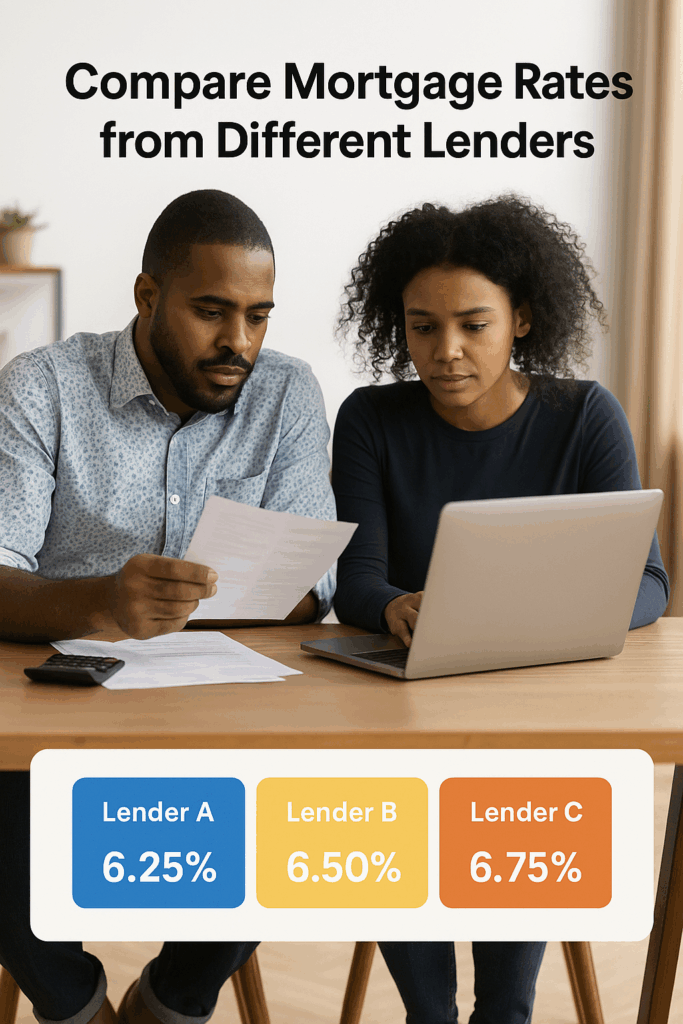

When shopping for a home in Utah, understanding mortgage rates Utah is the key to making a smart, long-term financial decision. With rising home prices and fluctuating interest rates, comparing loan types and using mortgage calculators with extra payments can help you find the best path forward.

Compare Mortgage Rates to Save on Your Loan

Utah’s real estate market moves fast, and staying informed about mortgage rates today gives you a competitive advantage. Whether you’re in Salt Lake City or Provo, using a mortgage rates calculator or working with a mortgage advisor can help you compare options and get preapproved with confidence.

Make sure to gather all documents needed for mortgage approval early on. These often include W-2s, pay stubs, tax returns, and bank statements—standard items in the mortgage approval process.

Explore Home Loans Utah Residents Trust

Utah homeowners have access to various loan types designed to meet their individual needs:

FHA loan – Great for first-time homebuyers with lower credit scores.

USDA loan – Offers 0% down for qualifying rural buyers.

Jumbo loan – For homes exceeding standard loan limits.

Arm Loan – Adjustable rates for those planning to move or refinance.

First time home buyer loan – Often paired with financial assistance programs.

For a side-by-side comparison, try a mortgage payment calculator or a mortgage loan calculator with extra payments to model different monthly scenarios.

Mortgage Calculator With Extra Payments = Major Savings

Did you know that small extra payments can lead to huge interest savings? A mortgage calculator with extra payments helps you see how quickly you could pay off your home.

Other helpful tools include:

Mortgage payment calculator with extra payments

Extra payment calculator

Mortgage calculator with extra payments and amortization

Mortgage calculator with extra payments and lump sum

Mortgage payoff calculator with extra principal payment

These calculators give you a visual breakdown of amortization, interest reduction, and timeline acceleration.

Use Early Payoff Calculators to Plan Smarter

Tools like the early payoff calculator and home loan early payoff calculator are ideal for people who want to own their home sooner. If you plan on making additional monthly or biweekly payments, tools such as:

Amortization schedule with extra payments

Biweekly mortgage calculator with extra payments

Amortization calculator with extra payments

Mortgage calculator with multiple extra payments

…can give you accurate, flexible forecasts for your strategy.

Work With a Mortgage Lender in SLC

If you’re ready to take the next step, a mortgage lender in SLC can walk you through every stage—from loan application to closing. Whether you’re refinancing or buying your first home, working with a local expert ensures you’re getting tailored advice.

They’ll help you compare home loans rates, explore heloc rates Utah, and even advise on whether a mortgage with extra payments strategy fits your goals.

Conclusion

You don’t need to be a financial wizard to make smart mortgage decisions. From understanding mortgage rates today to leveraging tools like a mortgage x extra payment calculator, Utah homeowners have more options than ever to take control of their financial future.

Want to get started? Check out our full library of mortgage calculators and connect with a licensed loan officer today.

This could be you! Read our Ultimate Guide to Tiny Home Mortgages to see how you can get your own Tiny House mortgage.

Everything You Need to Know About Tiny Home Loans in 2025

Are you ready to downsize, live more sustainably, or simplify your budget?

A tiny house mortgage can help. Lenders now offer several loan products for this growing market. Whether you plan to buy a finished home or order a custom build, you must understand each financing path.

Understanding Your Tiny House Financing Options

Tiny homes rarely fit the rules for a standard mortgage, so you need alternatives.

First, check banks, credit unions, and online lenders that market “tiny house loans.”

Next, compare personal loans; they fund quickly, yet their rates run higher.

Finally, look into tiny-house credit-union programs. These often feature lower fees and flexible terms.

One increasingly common route is to go through tiny house credit union mortgage programs, which may offer better terms, lower closing costs, and more flexibility than traditional banks. If your home is built on a permanent foundation, you may be able to apply for a fixed-rate mortgage, while those with mobile or on-wheels homes may need to consider a chattel loan for manufactured home.

Fixed-Rate vs. Chattel Loans

If your home sits on a permanent foundation, you can request a fixed-rate mortgage. Homes on wheels usually require a chattel loan, which treats the structure as personal property rather than real estate.

A chattel loan is a type of loan used to finance the purchase of movable personal property, often referred to as chattel, such as manufactured homes, vehicles, or equipment. It differs from a traditional mortgage, which is used for real estate, as chattel loans specifically target assets that are not permanently attached to land.

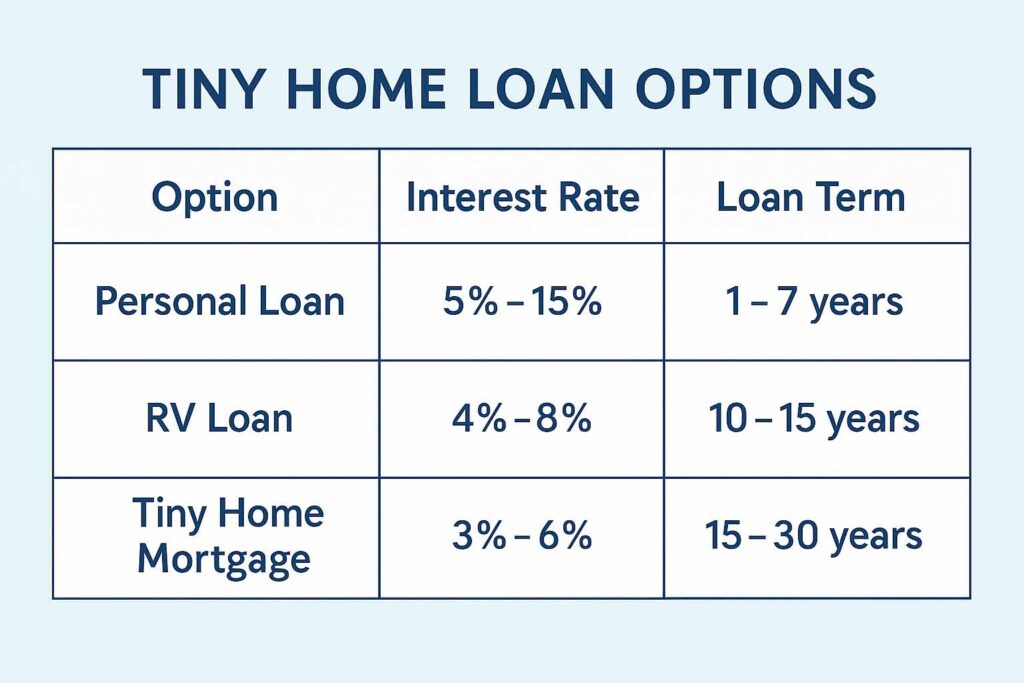

OPTION

INTEREST RATE

LOAN TERM

Personal Loan

5 – 15%

1 – 7 years

RV Loan

4 – 8%

10 – 15 years

Tiny Home Mortgage

3 – 6%

15 – 30 years

As you can see, there are a number of financing options depending on how long of long term you are interested in, each with different common interest rates. Check with a local credit union or bank for accurate mortgage rate information.

The smaller the house, the larger the life.” – Unknown

Are You Eligible for a FHA Manufactured Home Loan for your Tiny Home Mortgage?

Many first-time buyers are surprised to learn that government-backed programs such as the FHA manufactured home loan or VA manufactured home loan can apply to tiny or manufactured homes, especially if they meet certain size and foundation requirements. You’ll need to meet credit and loan requirements, and the home often must be permanently affixed to owned land.

If you qualify for a USDA manufactured home loan, you could benefit from zero down payment and low-interest terms, especially in rural areas. These programs are ideal for people who want to keep monthly payments manageable.

Planning Your Down Payment for a Tiny Home Mortgage

Most lenders want a 3 – 20% down payment. Your credit score drives that figure. Therefore, raise your score before you apply, and the lender may lower both the down payment and the mortgage-insurance premium. Use an online calculator to test payment scenarios, including taxes and escrow.

Use a mortgage calculator to estimate your monthly payments based on your interest rate, loan type, and loan estimate. Don’t forget to factor in property taxes, mortgage insurance, and escrow account costs. Check out our article on Mortgage Pre-Approval.

Modular Home vs. Tiny Home: A Quick Comparison

If you’re not 100% set on a tiny home, you might want to compare it to a modular home mortgage or manufactured home financing.

Modular homes are built in sections at a factory and later assembled on-site. They give you more space and, often, a smoother underwriting path. Rates can run a bit lower than tiny-home loans, yet zoning laws for modular builds stay strict. Consequently, verify local codes before you decide.

Interest rates and modular home loan rates are often slightly better than those for tiny homes. That said, modular home lenders still may require stricter building codes and zoning compliance.

The Role of Your Real Estate Agent and Lender

A knowledgeable real estate agent familiar with alternative housing is a must. They can help you find properties zoned for tiny homes and even connect you to manufactured home lenders or best manufactured home lenders who offer competitive rates.

Working with a mortgage broker or mortgage lender who understands tiny homes will make a big difference in navigating approval hurdles. Ask your broker to break down terms between an adjustable-rate mortgage and fixed-rate mortgage so you can decide what works best for your long-term goals.

Final Thoughts: Is a Tiny Home Right for You?

The home buying process for a tiny house may involve a few more hoops than a traditional purchase—but the rewards are worth it. Lower debt-to-income ratio requirements, smaller closing costs, and reduced monthly obligations make it an appealing choice for many modern buyers.

Whether you’re a minimalist, a first-time buyer, or simply ready for a change, a tiny house mortgage could be the start of your next great adventure.

This could be you! We hope you enjoyed learning about how you can get your own Tiny House mortgage.

External Links for More Information about Tiny Home Mortgages and Tiny House Mortgages

Cole Preece is an MBA and MSIS student at the University of Utah graduating in December 2025. Cole is a Utah local who enjoys exploring the mountains, forests, and beaches in the Rocky Mountains and Pacific Northwest.

Homeownership is possible—even on a limited income. You don’t need a perfect credit score or massive savings to buy a home in Utah. Whether you’re applying for your first loan or looking to refinance, this guide will walk you through how to qualify for a mortgage with low income, explore government loan programs, and compare key options like fixed vs adjustable-rate mortgages.

Best Mortgage Rates for First-Time Home Buyers

If you’re buying your first home, you may qualify for some of the best mortgage rates for first time home buyers through FHA, VA, or USDA programs. These government-backed loans often offer:

Lower down payments

Reduced credit score requirements

Flexible income limits

To get the best deal, always compare mortgage rates from different lenders. Shopping around can save you thousands in interest over time.

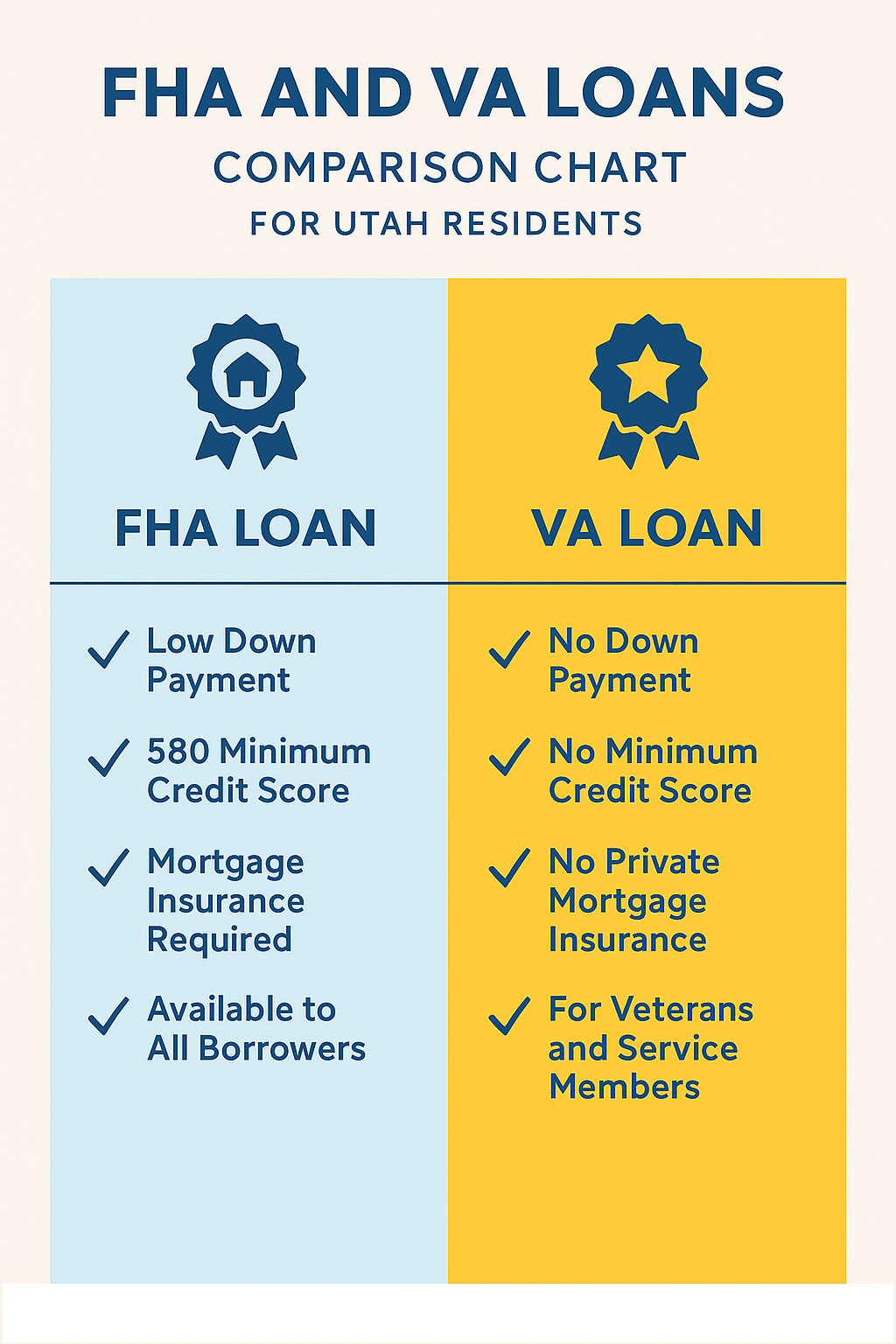

FHA and VA Loan Requirements in Utah

If you’re low on savings or have a lower credit score, FHA loan requirements in Utah may make homeownership accessible:

3.5% minimum down payment

Credit scores starting at 580

Backed by the Federal Housing Administration

FHA loans are designed specifically for first-time and low-income buyers, making them one of the most popular options in Utah.

Current VA Mortgage Rates in Utah

If you’re a veteran, active-duty military member, or eligible spouse, current VA mortgage rates in Utah could be your lowest-cost path to homeownership. VA loans offer:

0% down payment

No private mortgage insurance

Competitive interest rates

To get started, learn how to apply for a VA home loan step by step, including obtaining your Certificate of Eligibility (COE) and finding a VA-approved lender.

with a lower income or limited savings.

How to Refinance Your Mortgage With Bad Credit

Yes, it’s possible to refinance with bad credit. Programs like the FHA Streamline Refinance allow current homeowners to lower interest rates without needing a new appraisal or full credit check.

Other strategies include:

Working with a mortgage broker in Salt Lake City Utah who understands local lending options

Improving your debt-to-income ratio (DTI)

Making on-time payments for 6–12 months before applying

Fixed vs Adjustable-Rate Mortgage: Pros and Cons

When choosing a mortgage, it’s important to weigh the fixed vs adjustable rate mortgage pros and cons:

Mortgage Type

Pros

Cons

Fixed-Rate

Consistent monthly payments, stability

May have a higher initial rate

Adjustable-Rate (ARM)

Lower starting rates, short-term savings

Rate can rise over time, increasing payment risk

If your income is tight or unpredictable, fixed-rate loans usually offer safer long-term budgeting.

Mortgage Pre-Approval vs Pre-Qualification

Before shopping for a home, get pre-approved—not just pre-qualified. Pre-approval shows sellers and lenders that you’re serious and gives you a more accurate budget range.

Pre-Qualification

Pre-Approval

Soft check, quick estimate

Hard credit pull, verified documentation

Not binding

Increases purchase credibility

Utah Mortgage Lender Reviews

Reading reviews of Utah mortgage lenders helps you find the best match. Look for:

Specialization in FHA or VA loans

Experience with first-time buyers

Responsive customer service

Some local credit unions and community banks offer more flexible terms for low-income applicants than large national lenders.

Work With a Mortgage Broker in Salt Lake City Utah

A local mortgage broker in Salt Lake City Utah can help you:

Understand your best loan options

Apply for low-income or special program loans

Navigate local banks and credit unions

Brokers often have access to exclusive rates and understand Utah’s unique housing landscape better than large national lenders.

HELOC vs Home Equity Loan Comparison

If you already own a home and want to access its equity:

A HELOC (Home Equity Line of Credit) works like a credit card. You borrow as needed.

A Home Equity Loan gives you a lump sum with a fixed rate.

Both can help with renovations or debt consolidation—even with moderate credit.

Best Bank for Home Equity Loans in Utah

When comparing Utah banks, look at:

Interest rates

Fee transparency

Customer reviews

Flexibility on credit requirements

Credit unions often provide more competitive terms to Utah residents.

How Mortgage Interest Rates Are Determined

Mortgage rates are influenced by:

Federal Reserve interest rate policies

Economic trends

Your credit profile and DTI ratio

Loan type (FHA, VA, fixed, ARM)

Stay informed and try to lock your rate when market trends are favorable.

Best Online Mortgage Calculators for First-Time Buyers

Use these tools to estimate:

Monthly payments

Interest costs over the life of your loan

Affordability based on income

A few great free tools include:

NerdWallet Mortgage Calculator

Bankrate’s Affordability Estimator

Utah Housing Corporation calculators

Final Thoughts

Homeownership is within reach—even on a limited income. With the right preparation, smart comparisons, and loan program choices, you can qualify for a mortgage in Utah and start building equity and stability for your future.

Have questions or need help getting started? Contact a local mortgage advisor today.

When exploring mortgage rates 2025, it’s crucial to understand your options for home mortgage loans, refinancing, and government programs. Whether you’re starting a loan application or considering mortgage refinancing, this guide covers everything from using a mortgage calculator to choosing the best mortgage broker for your needs.

How to Qualify for a Mortgage Loan in 2025

If you’re planning to buy a home, knowing how to qualify for a mortgage loan is essential. Lenders look closely at your:

Credit score

Debt-to-income ratio

Employment history

Savings and assets finance

Using a mortgage calculator helps you determine what monthly payment you can comfortably afford. For buyers asking, is 7% interest rate too high?, the answer depends on your financial situation and housing market trends. Some borrowers lock in rates now to avoid further increases, while others wait for rates to drop.

What Is the Best Type of Loan to Get for a House?

Many wonder, what is the best type of loan to get for a house? Options include:

Conventional loans: Ideal for good credit and bigger down payments

VA loans: No down payment for those who qualify to VA loans

Jumbo loans: Required for amounts exceeding the mortgage jumbo loan limit

Even a mortgage on $250,000 loan varies in cost depending on loan type and rate. For second homes, keep an eye on second home financing rates, which are usually higher than primary residence rates.

Mortgage and Refinance Interest Rates Today

Checking mortgage and refinance interest rates today helps you plan. Experts predict fluctuations in mortgage rates 2025 due to economic changes, inflation, and Fed policies. If you’re refinancing, be aware that the market can feel mortgage refinancing unsteady, but opportunities still exist. Always ask lenders.

What is the interest rate on a mortgage loan?

What’s the process for an interest rate and rate lock?

Are there prepayment penalties?

Sometimes homeowners explore how to change mortgage companies to find better terms, but it usually requires a new loan application.

Exploring Government Loans or Grants

If you’re researching how to get a government loan or grant, consider these programs:

HUD for first-time buyers

USDA loans for rural properties

State housing grants

Even when applying for grants, your financial profile — including your assets finance — plays a role.

Options for Homeowners with Bad Credit

If your credit isn’t perfect, there are still paths forward. Mortgages for bad credit and unconventional mortgage loans with bad credit (also called non-QM loans) help borrowers who don’t fit traditional guidelines. Non-QM lenders may consider:

Bank statements instead of tax returns

Higher debt-to-income ratios

Alternative income sources

Before applying, follow a home loan pre-approval checklist to gather documents like pay stubs, W-2s, tax returns, and bank statements.

Using Technology and Brokers to Simplify Your Mortgage

Digital tools like Rocket Mortgage home equity loans make the process faster. But working with the best mortgage broker can help you navigate loan products, interest rates, and closing costs more effectively.

Are you considering mortgage refinancing in Utah this year? With interest rates shifting and housing values stabilizing, 2025 could be the perfect time to refinance your home loan. Whether you’re looking to reduce your monthly payment, access equity, or shorten your loan term, understanding current refinance rates is essential.

Refinance my home to save on interest? Yes, please. From analyzing 15 year fixed refinance rates to locking in the best home refinance rates, this guide will help Utah homeowners make confident, informed decisions. The key is not just finding a lower rate but choosing the loan structure that best supports your long-term financial goals.

Refinance home loan: Why 2025 Might Be the Right Time

The decision to refinance home loan terms typically revolves around saving money, lowering monthly payments, or adjusting the loan duration. Homeowners across Utah are taking advantage of the stability in current refinance rates to improve their financial outlook.

Options like the 30 year mortgage refinance rates or 15 year mortgage refinance rates each serve different goals. If you’re staying long-term, 30 year mortgage refinance rates may offer manageable monthly payments. But if you want to pay off your loan faster, lower refinance interest rates on a 15-year term might be a better fit.

Some Utah residents are also considering cash-out refinances, using the equity in their homes for debt consolidation, home renovations, or investment opportunities. As equity builds, refinancing becomes not just a financial move but a wealth-building strategy.

Refinance rates today: What Utah Borrowers Should Expect

Keeping track of refinance rates today gives borrowers the leverage to lock in better terms. Current refinance mortgage rates vary daily based on market conditions, and Utah is seeing a competitive spread across local lenders and credit unions.

You should also compare refinance interest rates today for both 15 and 30-year options. Make sure to request a Loan Estimate from at least three lenders and review not just the rate, but the full APR, fees, and loan structure.

Many borrowers are surprised to learn that their existing lender isn’t always the best option. Exploring credit unions, regional banks, and online lenders can reveal more attractive refinance mortgage rates with lower closing costs and faster approval times.

Home refinance rates vs. refinance mortgage rates: Is There a Difference?

In general, home refinance rates and refinance mortgage rates today are used interchangeably. However, the term mortgage loan refinance often includes more detailed considerations like your credit score, loan-to-value ratio, and debt-to-income ratio.

As of this month, home refinance rates 30 year fixed are trending lower in Utah than the national average. This gives local borrowers a real opportunity to benefit from the lowest refinance rates in years.

If you’re refinancing a government-backed loan, like an FHA or VA loan, make sure to ask about streamline refinance options, which require less paperwork and may offer quicker processing than a standard mortgage loan refinance.

Best home refinance rates: How to Secure Them

To get the best home refinance rates, consider the following:

• Boost your credit score before applying • Avoid cash-out refinancing unless necessary • Maintain consistent income and employment history • Consider locking in when refinance rates today 30 year fixed drop below your current rate

Even small reductions in refinance interest rates can lead to significant long-term savings.

Another tip: some Utah lenders offer lower refinance rates for borrowers who set up automatic payments from a checking account or who agree to keep multiple accounts with the institution.

Refinance my home: Should I Do It in 2025?

If you’re wondering whether to refinance my home in Utah, start by calculating your break-even point. This is the time it takes for the monthly savings to offset the refinancing costs. If you plan to stay in your home longer than that, refinancing could be a smart move.

With the availability of both current home refinance rates and custom loan options from Utah lenders, there’s never been a better time to explore your refinancing choices.

Also consider your life stage. If retirement is in your near future, shortening your term using today’s refinance interest rates could help you enter retirement debt-free.

Current refinance rates 30 year fixed vs. 15 year fixed refinance rates

A side-by-side comparison:

• 30 year mortgage refinance rates: Lower monthly payments, higher total interest paid • 15 year fixed refinance rates: Higher monthly payments, but lower total interest and faster equity growth

Choosing the right term depends on your financial goals, risk tolerance, and how long you plan to stay in your home.

For homeowners planning to sell or relocate within the next 5–7 years, it may not be worth it to pay higher monthly payments for a 15-year loan. Instead, consider hybrid ARM options with an initial fixed term and lower introductory refinance rates.

Lowest refinance rates in Utah: What Impacts Your Rate?

Your interest rate is affected by several factors:

• Credit score • Debt-to-income ratio • Loan-to-value ratio • Type of property (primary home vs. rental)

If your financial profile is strong, lenders may offer some of the lowest refinance rates available, particularly on mortgage refinance rates today for qualified borrowers.

To improve your loan profile before applying, pay down high-interest debt, avoid opening new credit accounts, and provide clear, organized documentation of your income and assets.

Refinance your Home: Key Takeaways Before You Apply

Before you refinance, make sure to:

• Review your credit and debt levels • Research refinance rates • Gather financial documents: W-2s, tax returns, pay stubs • Shop for multiple quotes from Utah lenders

Whether you’re interested in a simple rate-and-term refinance or exploring cash-out options, understanding refinance rates today and current mortgage refinance rates 30 year fixed is the first step toward saving money and building wealth through your home.