If you’re wondering whether it’s the right time to refinance, you’re not alone. Utah refinance mortgage rates are shifting as we move through 2025, making this the ideal moment to evaluate your financial options. Refinancing can reduce monthly payments, shorten loan terms, or unlock equity — but only if you understand how the process works and which programs are best for you.

Current Mortgage Rates in Utah

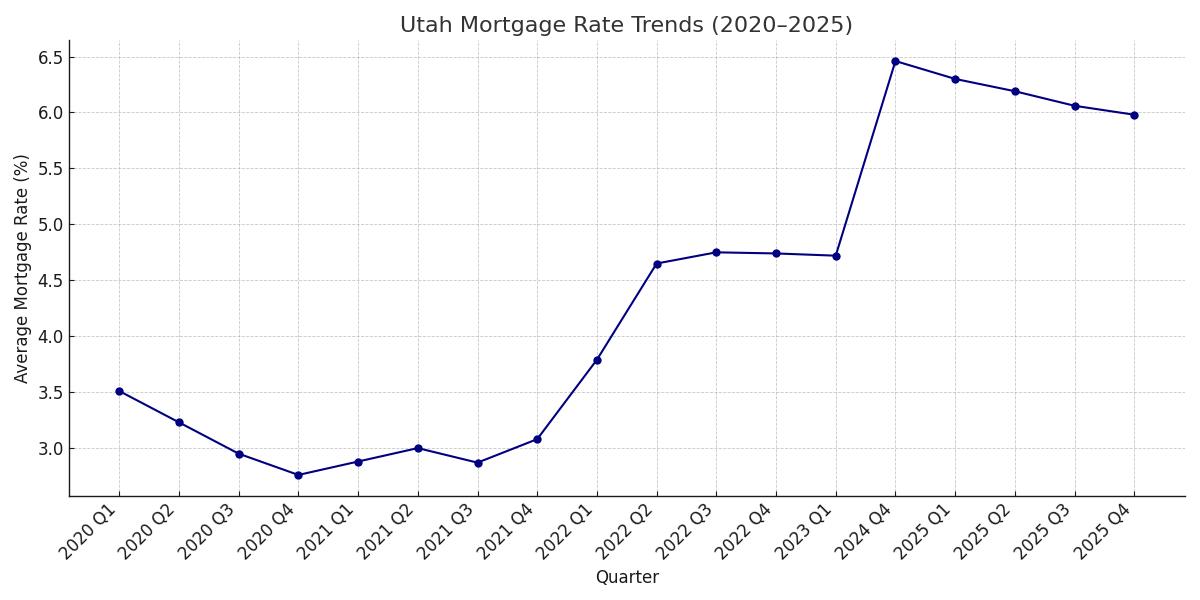

Tracking the current mortgage rates in Utah is essential before making a move. In mid-2025, homeowners are seeing fluctuations in 30-year fixed, 15-year fixed, and adjustable-rate loans, all of which impact refinancing options. Websites like Bankrate and City Creek Mortgage offer live rate data and commentary on Utah mortgage interest rates today.

A line chart showing changing Utah mortgage rates from 2020 to 2025

How to Use a Utah Mortgage Calculator

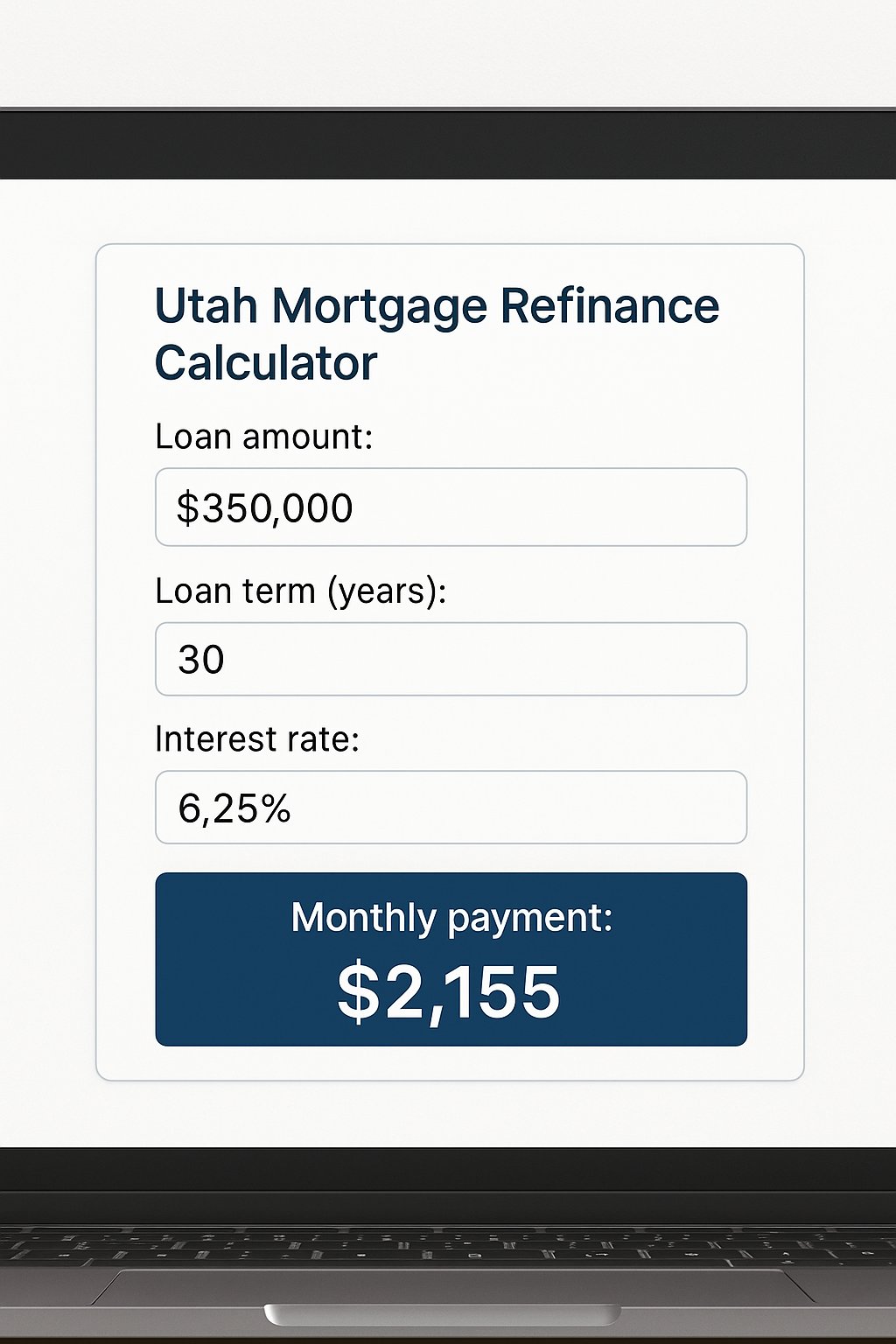

A Utah mortgage calculator can help you estimate new monthly payments based on your balance, term, and interest rate. More advanced tools, like a mortgage payment calculator Utah or mortgage calculator with taxes and insurance Utah, provide a clearer picture by factoring in property taxes, insurance, and HOA fees.

If you’re considering an FHA loan, an FHA mortgage calculator Utah will include mortgage insurance premiums (MIP) specific to that program.

A computer screen displaying a Utah mortgage refinance calculator.

When to Refinance Mortgage in Utah

So when to refinance mortgage in Utah? Ideal timing is usually when you can lower your interest rate by 0.5% or more or switch from an adjustable-rate mortgage to a fixed-rate mortgage. According to the mortgage rates Utah forecast, rates are expected to stay low for the next two quarters — which means acting now could lock in major savings.

Try a mortgage refinance calculator Utah to compare your current loan against a new one. Use it to evaluate how long it will take to recoup closing costs and whether refinancing aligns with your future plans.

Best Mortgage Companies for Refinancing in Utah

Working with the best mortgage refinance companies Utah can make the process smoother and more affordable. Look for top rated mortgage lenders Utah that offer competitive fees, fast processing, and clear communication. Sites like NerdWallet list top picks and customer reviews. You can also explore best local mortgage companies Utah or mortgage companies for bad credit Utah if your financial situation needs more flexibility.

Utah Home Loan Programs for 2025

Homeowners should also explore Utah home loan programs that may enhance refinancing opportunities. For example:

- FHA home loans Utah: Flexible credit requirements and lower down payments.

- VA home loans Utah: Ideal for veterans with no PMI and lower closing costs.

- Home equity loans Utah: Useful for renovations or paying off high-interest debt.

These programs often work in tandem with standard refinancing. If you’re a first-time homeowner, you may also want to look at home loans for first time buyers Utah or home loans with no down payment for purchase options.

A couple reviewing loan documents with a mortgage broker in Utah.

Fixed vs Adjustable Mortgage Rates in Utah

Choosing between Utah fixed vs adjustable mortgage rates is an important part of your refinance decision. Fixed ratesoffer stability and predictability, which is great if you plan to stay in your home long-term. Adjustable rates (ARMs), on the other hand, may offer lower initial rates but can increase after a few years — potentially making them riskier in a volatile market.

Mortgage Trends by County in Utah

It’s also helpful to look at mortgage rates Utah county by county, especially in high-growth areas like Salt Lake County, Utah County, and Davis County. Local lenders may offer better rates and terms due to competition and localized risk evaluation.

Why 2025 Is a Smart Year to Refinance

With the average mortgage rates Utah experiencing mild declines and inflation stabilizing, many Utah homeowners are capitalizing on lower monthly payments, shorter terms, or equity access. If you’re considering a refinance, use tools like a mortgage calculator, compare offers from best mortgage companies near me, and check for mortgage refinancing costs to ensure you’re making a well-informed decision.