Buying a home can be one of the most exciting and confusing experiences of your life. Whether you’re trying to figure out how much house you can afford, worried about your credit score, or just wondering if mortgage rates are finally going down, you’re not alone. The good news? You don’t need to be a financial expert to make smart decisions. You just need the right information, and that’s exactly what this guide is here for.

2025 Mortgage Rate Forecast for Home Buyers

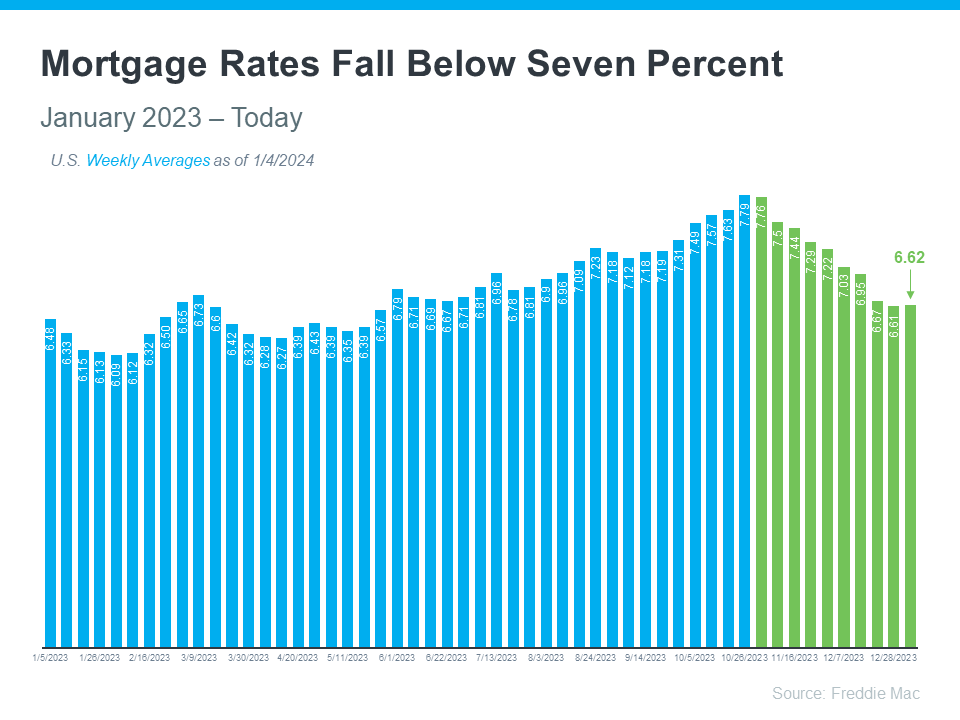

Let’s start with the question on everyone’s mind: “Will mortgage rates drop this year?”

According to expert predictions on mortgage rates for next quarter, we’re seeing some cautious optimism. The 2025 mortgage rate forecast for home buyers suggests that rates may stabilize or slightly decline as inflation slows and the Federal Reserve eases its policies. However, don’t expect a huge drop overnight. The era of ultra-low interest rates is behind us, for now.

Some mortgage lenders may cut interest rates on specific products or for well-qualified buyers. If you’re waiting to “time the market,” it’s smarter to focus on your financial readiness instead. Locking in a rate when you’re prepared to buy, rather than waiting endlessly for the perfect dip, can save you more in the long run.

Getting Prequalified When You’re Self-Employed

Mortgage Rates as a Self-Employed Person

If you’re a freelancer, business owner, or contractor, getting a mortgage loan can feel like a maze. Lenders love consistency, and self-employment income isn’t always straightforward. Still, you absolutely can qualify.

To get started, you’ll need to show:

- Two years of steady income (via tax returns)

- Clear bank statements

- Profit and loss statements

- A reasonable debt-to-income ratio (typically below 43%)

Understanding how the debt-to-income ratio affects mortgage eligibility is critical. It’s one of the main metrics lenders use to evaluate whether you can realistically manage your monthly payments.

Need to improve your standing fast? Learn how to improve your credit score quickly before a mortgage application by paying down credit cards, disputing errors on your report, and avoiding new debt.

Mortgage Loan Options for Buyers with Fair Credit

Can I Get a Mortgage Loan with Fair Credit or Collections?

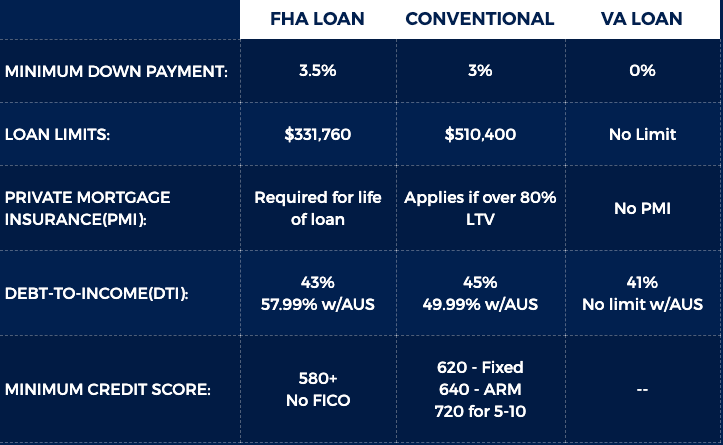

Yes! Many people assume you need a perfect credit score to buy a home, but that’s not true. Plenty of mortgage loan options for buyers with fair credit are available, especially if you explore government-backed programs like FHA, USDA, or VA loans.

Some lenders specialize in working with nontraditional borrowers:

- Mortgage lenders that work with Chapter 13 bankruptcy cases

- Lenders who help people get a mortgage with collections on their credit report

If your score is around 600, don’t panic. You may still qualify with the best mortgage lenders for a 600 credit score with a low down payment, just expect to provide more documentation and possibly pay a slightly higher interest rate.

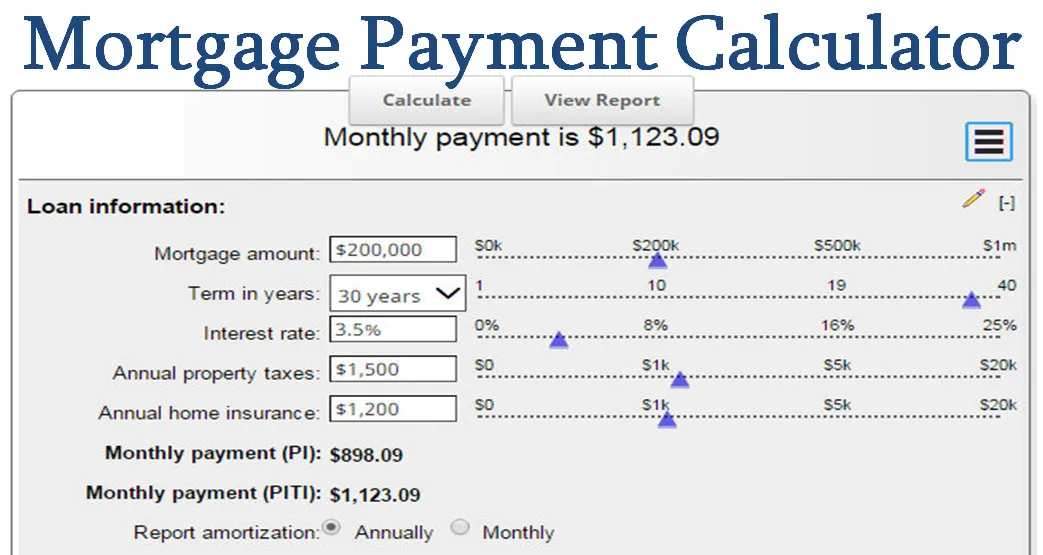

Use the Right Mortgage Calculator

Helpful Tools to Estimate Your Costs

There are a lot of mortgage calculators out there, but not all are created equal.

Start with a mortgage loan calculator for a basic monthly payment estimate based on your loan amount, interest rate, and term.

Then try a mortgage calculator for FHA loans with taxes and insurance to get a clearer picture of what you’d owe every month (including escrows like property tax and homeowners’ insurance). You can also play around with a mortgage estimator with a credit score to get quotes based on your actual profile.

Planning to pay ahead? A mortgage calculator with extra payments can show you how much time and interest you’ll save by adding a little extra each month.

For couples or co-buyers, a mortgage affordability calculator for dual-income households can help you see your full buying power combined.

How Much House Can I Afford?

Income, Debt, and Mortgage Rates

Now let’s get into one of the most common questions: how much house can I afford based on income and debt?

There are two answers: what the lender will approve you for, and what you can comfortably afford. They’re not always the same.

Lenders typically use your gross monthly income and debts to calculate affordability. Tools like a mortgage rate estimator based on income or a mortgage estimator with taxes can help you do this before even talking to a lender.

Not sure whether to focus on savings or debt reduction? Ask yourself: Should I pay off debt or save for a mortgage down payment? Ideally, you’re doing both. But if you must prioritize, eliminate high-interest debt first, then redirect those payments into your savings.

Budgeting for the Hidden Costs

How to Budget for Mortgage Closing Costs and Fees

You’ve saved your down payment. Great! But what about everything else?

When buying a home, you’ll also need to budget for closing costs. These can include:

- Appraisal fees

- Loan origination fees

- Title insurance

- Escrow deposits

- Prepaid taxes and insurance

On average, closing costs run between 2%–5% of the home price. Learning how to budget for mortgage closing costs and fees is just as important as saving for the home itself. A good mortgage estimator with taxes can help you avoid surprises.

What If I’m a First-Time Buyer?

Buying your first home can feel like stepping into the unknown, but don’t worry, you’ve got options.

Programs like FHA, USDA, and VA loans were built to help people just like you. Some of the most helpful mortgage options for first-time home buyers with no down payment come from these federally backed programs. They reduce or eliminate down payments and make qualifications more flexible.

Final Thoughts

Buying a home in 2025 doesn’t have to be overwhelming. Whether you’re exploring mortgage loan rates, figuring out how much you can afford, or using a mortgage calculator with taxes and insurance, there are tools and options to help you every step of the way.

From self-employed buyers to those with fair credit, you’re not alone, and you’re not out of options. Use what you’ve learned here to take the next step, smarter and more confidently.

Start where you are. Use the tools. Ask the questions. And keep going! Your home is closer than you think.