If you’ve been watching Utah mortgage rates in 2026, you know the market moves fast. Whether you’re searching for the best mortgage lenders in Utah or exploring Salt Lake City home loans, the right information is your greatest advantage. It also helps you make sense of Utah real estate trends before you commit. This guide covers everything from locking in a low rate to navigating first-time buyer programs.

Utah Home Loans: Rates and What You Need to Know

Finding the best current mortgage rates in Utah starts with comparing your options across multiple Utah mortgage brokers. Rates vary significantly depending on your loan type, credit score, and down payment, so shopping around is essential.

Here’s what to know about loan types currently available in Utah:

- Utah conventional loans are best for buyers with strong credit and at least 5–20% down.

- Utah jumbo loans are designed for higher-priced properties that exceed conforming loan limits.

- Utah fixed-rate mortgages lock in your rate for the life of the loan, ideal if you want payment stability.

- Utah adjustable-rate mortgages (ARMs) typically offer a lower starting rate, but adjust over time.

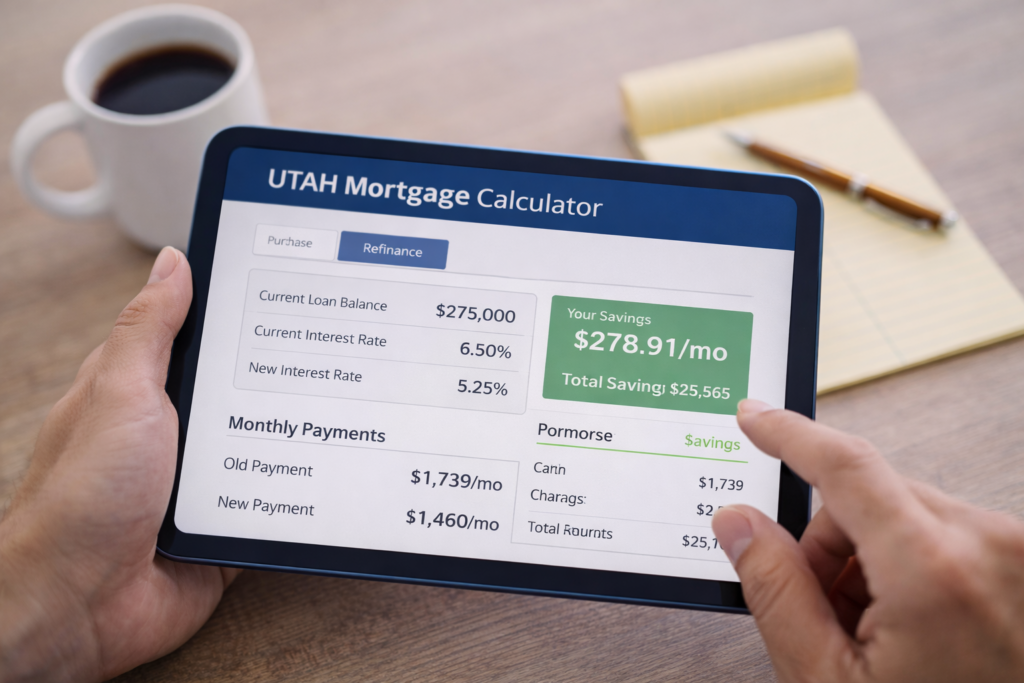

Use a Utah mortgage calculator to model your monthly payment before committing to a loan type. Don’t overlook Utah mortgage closing costs either. They typically range from 2–5% of the loan amount and can affect whether a new loan makes financial sense.

First-Time Home Buyer Utah: Programs and Grants

Many first-time buyers in Utah are surprised to learn they don’t need a 20% down payment. For a first-time home buyer in Utah, several programs can significantly reduce your upfront costs. Utah housing grants through the Utah Housing Corporation (UHC) offer down payment and closing cost assistance. Utah FHA loans require as little as 3.5% down and come with more flexible credit requirements. If you put less than 20% down, lenders will typically require Utah mortgage insurance (PMI). You can remove it once you build sufficient equity.

Understanding Utah mortgage requirements before you apply will put you in a much stronger position. These include debt-to-income ratios, minimum credit scores, and income limits for certain programs. Whether you’re looking at Provo home loans, St. George mortgage rates, or properties along the Wasatch Front, there’s a program designed to help.

Refinancing in Utah for Long-Term Wealth

If you already own a home, refinancing in Utah could be one of the most impactful financial moves you make in 2026. The key is to weigh your potential monthly savings against your Utah mortgage closing costs to determine your break-even point. Many homeowners refinance to switch from a high-rate ARM to a stable Utah fixed-rate mortgage. Others pursue a Utah mortgage refinance simply to lower their monthly payment. Refinancing is also a smart way to access home equity for renovations or education, or to shorten your loan term and build wealth faster.

With rates shifting throughout the year, keeping an eye on Utah mortgage news and acting when rates dip can save tens of thousands of dollars over the life of your loan.

For more information, visit the Current Rates Page or check out National Mortgage News to see how Utah trends compare nationally.