Wasatch Front Mortgage Rates: A City-by-City Guide to Utah Mortgage Lenders and Home Loans

Wasatch Front mortgage rates don’t change much from one city to the next — a 30-year fixed quote in Provo and the same quote in …

Wasatch Front mortgage rates don’t change much from one city to the next — a 30-year fixed quote in Provo and the same quote in …

Buying a home can be more complicated when you are self-employed, but it is absolutely possible. A self employed mortgage is designed for borrowers whose …

Mortgage Pre Approval Process in Utah: Requirements, Steps, and What to Expect. Buying a home in the state of Utah starts way before you actually …

Mortgage Rates Today Mortgage rates today can have a major impact on how much homebuyers pay each month and over the life of a loan. …

Buying a home in Utah is exciting, but before you start touring houses or making offers, one of the smartest first steps is mortgage pre …

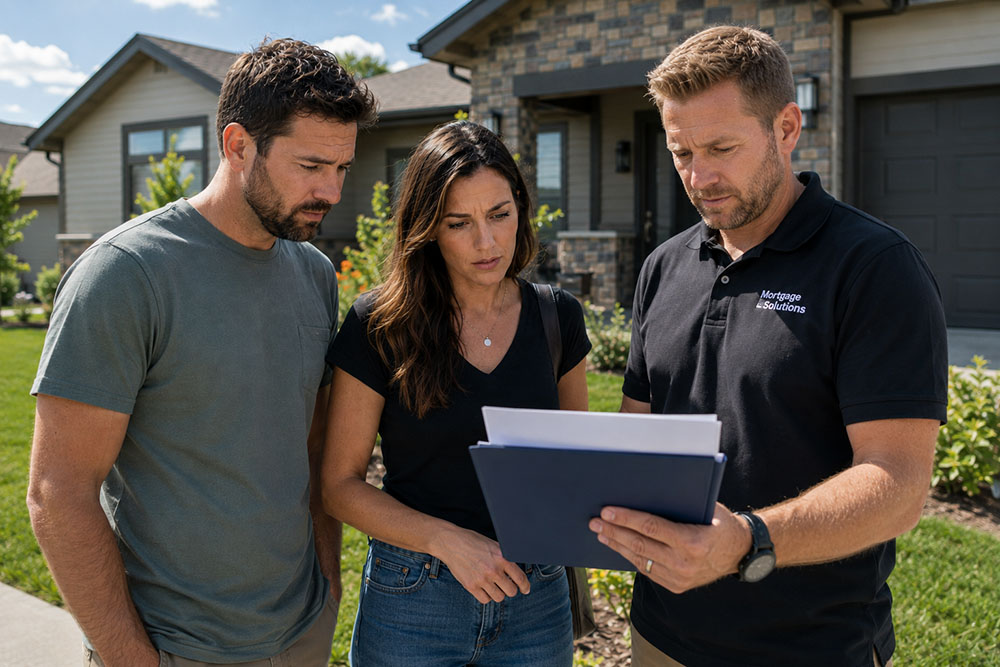

Choosing the right mortgage lender Salt Lake City homebuyers can trust is one of the most important decisions you’ll make when purchasing your first home. …

Buying a home in Utah moves fast, and getting a mortgage pre approval Utah lenders will stand behind is the step that lets you compete. …

Buying your first home is exciting, but it can also feel like a lot all at once. Between loan options, interest rates, credit requirements, and …

After more than two decades working in Utah’s mortgage industry, I’ve learned that the buyers who do well here aren’t the ones who time the …

When buyers search for interest rates today, they are usually looking for more than just a number. They want to know whether buying a home …