How to Refinance Your Mortgage in Utah

Refinancing your mortgage means replacing your existing home loan with a new one, ideally one with better terms. But how does refinancing a mortgage work? In short: you apply for a new loan, get approved, and use it to pay off your old loan. The result? New terms that could lower your monthly payment, reduce your mortgage refinance interest rates, or even allow you to tap into your home equity with a cash-out refinance.

Benefits of Refinancing a Mortgage

Why refinance your home loan? Here are the key benefits of refinancing a mortgage:

- Reduce your interest rate through current refinance mortgage rates

- Change loan types (e.g., from an ARM to a fixed-rate mortgage)

- Access cash via a cash-out refinance

- Eliminate PMI or consolidate debt

- Lower your taxes, insurance, and other housing-related costs

Whether you’re looking for no closing cost mortgage refinance options or a faster process like an FHA streamline refinance, refinancing can be a strategic financial move.

Should I Refinance My Mortgage?

If you’re asking, “Should I refinance my mortgage?” consider the following:

- Are mortgage refinance interest rates today lower than your current rate?

- Has your credit score improved since you got your loan?

- Will you stay in your home long enough to break even on closing costs?

If your answer is yes, then it’s likely a smart time to refinance your mortgage.

Current Refinance Mortgage Rates in Utah

Utah homeowners have access to some of the most competitive home mortgage refinance rates in the country. That said, rates vary daily. Be sure to compare current refinance mortgage rates with national averages, and review offerings from both local and online lenders to find the best refinance mortgage rates for your situation.

Find the Best Refinance Mortgage Rates

To get the best mortgage refinance rates today, compare quotes from multiple sources. Top mortgage companies for refinancing often provide customized options based on credit score, equity, and income level. Make sure to ask whether they offer no closing cost mortgage refinance options or rate locks.

Popular Mortgage Refinance Options in Utah

Utah borrowers have several mortgage refinance paths to choose from:

- Rate-and-term refinance: Adjust your loan’s term or interest rate

- Cash-out refinance: Tap into your home’s equity for extra funds

- FHA streamline refinance: Lower your rate with minimal paperwork (Learn more here → HUD FHA Streamline Guidelines)

- No closing cost mortgage refinance: Roll costs into the loan

Each path has unique benefits depending on your financial goals.

How Soon Can You Refinance a Mortgage?

How soon can you refinance a mortgage after purchase or a previous refinance? Some lenders allow it within 6 months; others may require a longer waiting period depending on the loan type and whether it’s a FHA streamline refinance or conventional product.

Special Refinance Scenarios

Not all homeowners have the same needs. Consider these mortgage refinance options:

- Refinance mortgage with bad credit: Government-backed loans like FHA or VA may offer flexibility

- Mortgage refinance for self-employed: Requires tax returns and income documentation

- Mortgage refinance options for seniors: Shorter terms, reverse mortgages, or lower monthly costs

- Refinancing a mortgage after divorce: Remove a former spouse from the mortgage and title

These paths may require additional documentation or underwriting but can be life-changing.

When to Refinance a Mortgage

Knowing when to refinance a mortgage can help you build wealth over time. Consider refinancing:

- When rates fall significantly

- When your home equity has increased

- When your financial or credit situation improves

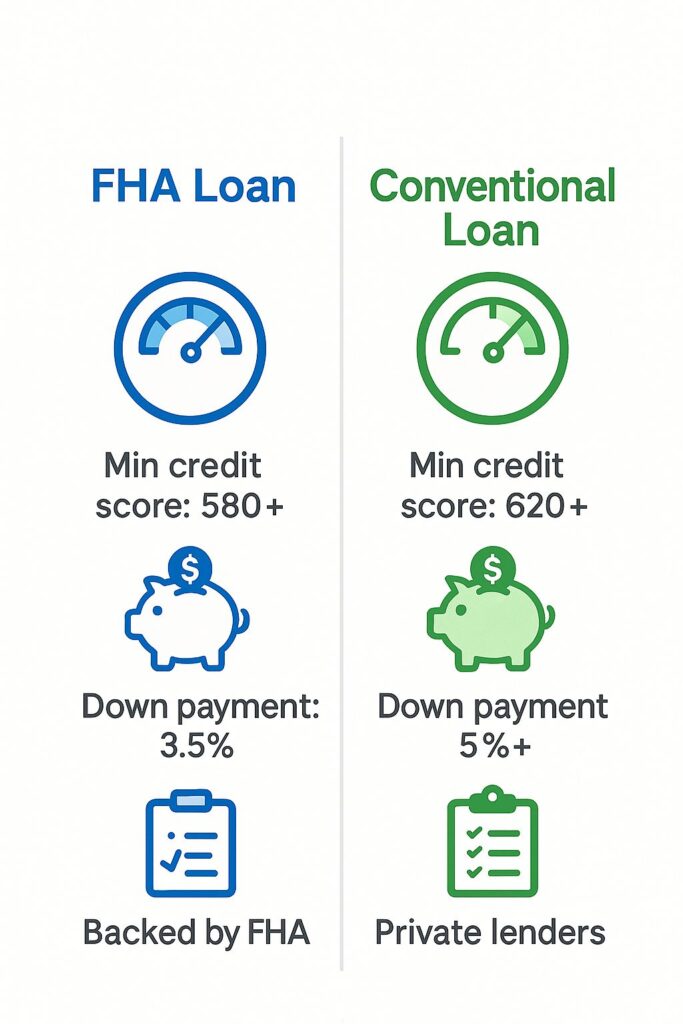

- When switching from an FHA loan to a conventional one to drop PMI

Refinancing at the right moment can lead to major savings.

Refinance Mortgage Calculator with Taxes

Use our refinance mortgage calculator with taxes to get a detailed look at your new monthly payment. Make sure to factor in property taxes, homeowners insurance, and any other fees to get a realistic picture.