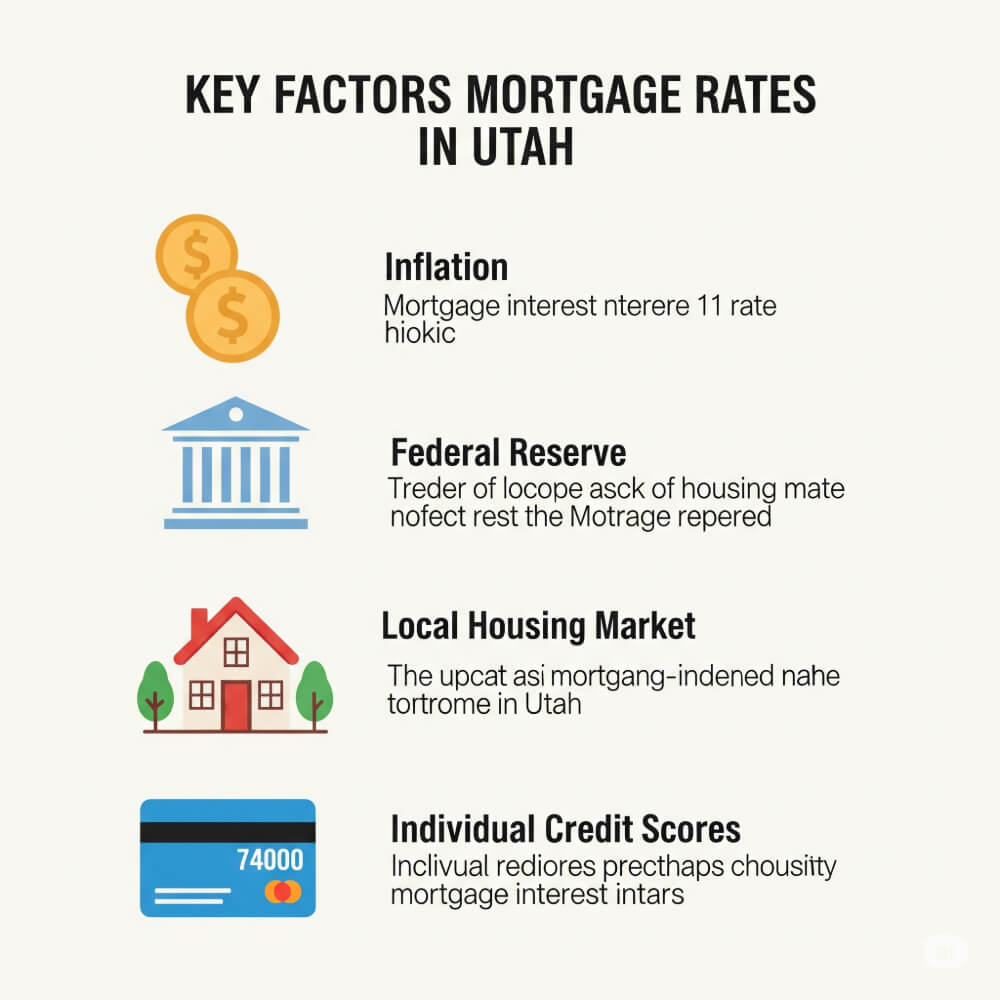

If you’re looking for current mortgage rates in Utah, you’re navigating one of the most challenging interest rate environments in over a decade. With mortgage interest rates today hovering around 6.75% to 7%, understanding today’s market can help you make informed decisions about buying or refinancing your home.

Current Mortgage Interest Rates Today

As of late June 2025, current mortgage interest rates are showing some volatility but remain elevated. Today’s average 30-year fixed-mortgage rate is 6.75%, a decrease of 7 basis points over the last seven days.

Key Rate Highlights:

- 30-year fixed mortgage rates: 6.75% – 6.82%

- 15-year fixed mortgage rates: 5.78% – 5.92%

- Current home mortgage rates in Utah: 6.25% – 6.915%

- Current mortgage refinance rates: 6.75% – 6.82%

The latest mortgage rates reflect ongoing economic uncertainty. By January 2025, the average rate on a 30-year fixed-rate mortgage surpassed 7% for the first time since last May.

30-Year Mortgage Rates in Utah

30-year mortgage rates remain the most popular choice for Utah homebuyers, offering predictable monthly payments. As of June 27, 2025:

- 30-year fixed rate mortgage: 6.25%

- 15-year fixed-rate loan: 5.375%

Utah’s 2025 mortgage rates typically align with national averages, but local lenders may offer competitive options for strong credit profiles.

Best Mortgage Lenders in Utah

Finding the best mortgage lenders in Utah requires comparing rates, fees, and loan programs. Options include national lenders, regional banks, and local credit unions.

Top Utah Mortgage Options:

- Pennymac Home Loans – Leading originator in Utah

- US Bank – Strong local presence with comprehensive programs

- City Creek Mortgage – Utah-based lender with local expertise

- Utah Housing Corporation – Offers down payment assistance

Government-Backed Programs

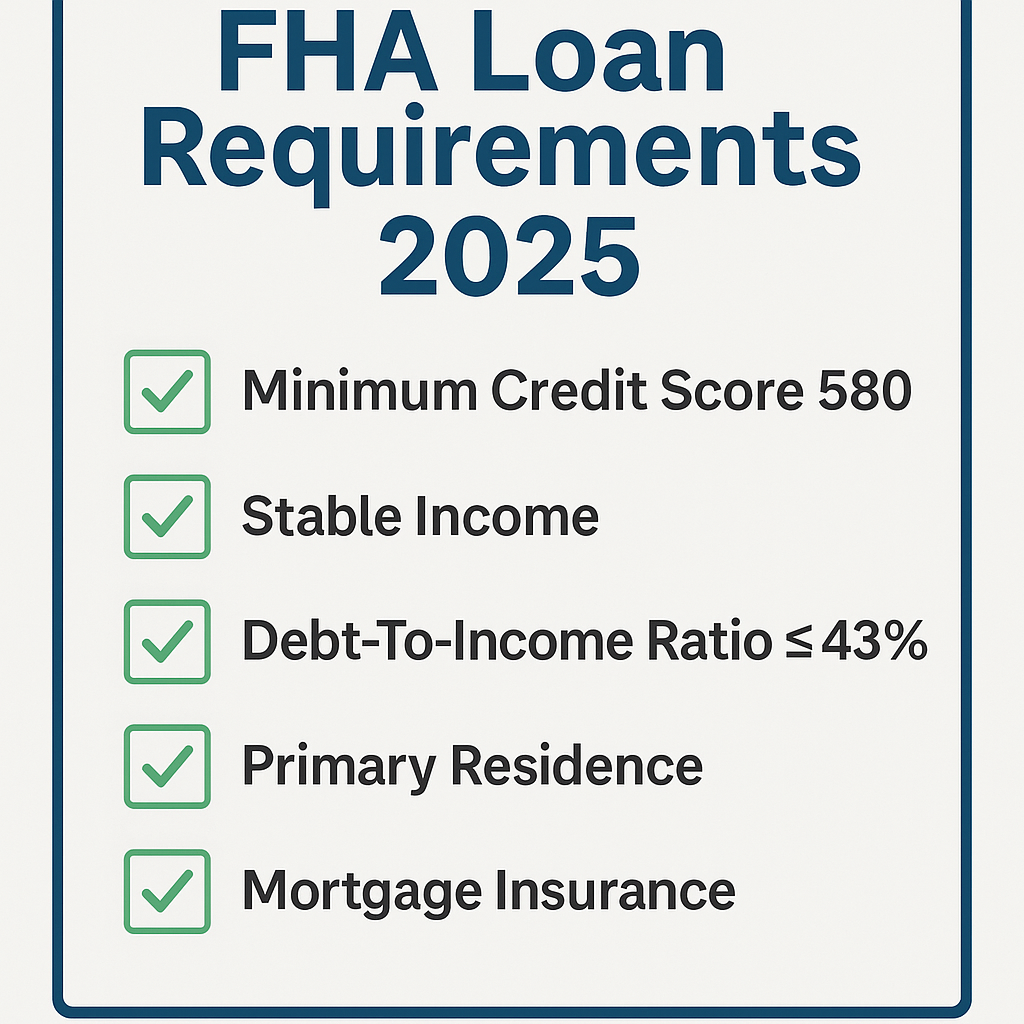

- Utah FHA loan requirements – Lower down payments for qualified buyers

- Utah VA loan eligibility – Benefits for military veterans

- Utah housing down payment assistance – Up to $30,000 in support

Utah Mortgage Calculator and Refinancing

Using a Utah mortgage calculator helps estimate monthly payments based on current fixed mortgage rates. With rates around 6.75%, sample monthly payments are:

Sample Monthly Payments (Principal + Interest):

- $300,000 loan @ 6.75%: $1,946/month

- $400,000 loan @ 6.75%: $2,594/month

- $500,000 loan @ 6.75%: $3,243/month

You’ll pay approximately $648.60 per $100,000 borrowed at 6.75%.

Refinance Rates in Utah

Utah homeowners should closely monitor refinance rates, especially if your mortgage rate is over 7%.

Refinancing makes sense when:

- Your current rate is higher than today’s

- You plan to stay long-term

- You have sufficient equity

- You can recoup closing costs quickly

First-Time Home Buyer Programs in Utah

First-time home buyer Utah programs help buyers overcome high rates and home prices.

Available Assistance Includes:

- Utah housing down payment assistance – Income-based

- Utah FHA loan requirements – 3.5% down payment

- Low-income home loans Utah – Specialized programs

- Mortgage loans for teachers in Utah – Career-specific benefits

- Home loans for nurses Utah – Healthcare worker programs

Utah Housing Market Trends

Utah’s housing market shows unique trends. Notably, 71% of mortgages have rates below 4%, leading to a strong lock-in effect.

Current Market Conditions (as of Jan 2025):

- Median home price: $508,749

- Average days on market: 64

- Homes selling above list price: 21.6%

A rise in rates from 3% to 6% increases monthly payments by 34% – from $1,657 to $2,227.

Getting Approved: Key Questions Answered

To get approved for a mortgage in Utah:

- Best credit score: 620+ for conventional loans

- Average mortgage rate in Utah: 6.25% – 6.915%

- Should I lock my rate today? – Yes, if rates are trending upward

- Compare lenders to secure the best offer

Mortgage approval requires:

- Stable income and job history

- Debt-to-income (DTI) ratio below 43%

- Sufficient down payment

- Solid credit score

Market Timing and Strategy

The best time to buy a home in Utah is typically spring to early fall. But current conditions may shift timing.

Strategy Tips:

- Focus on the right property, not perfect rate timing

- Use pre-approval to strengthen offers

- Consider mortgage options for self-employed

- Compare 30-year rates with other term options

Conclusion

Current mortgage rates in Utah remain high historically, but prepared buyers still have options. Whether you’re a first-time buyer or refinancing, knowing your options helps.

Rates around 6.75% are reasonable by historical standards. Don’t wait for the perfect rate — focus on the right home and loan. Use a Utah mortgage calculator, compare lenders, and explore programs to make a smart purchase in today’s market.