Welcome to Your Complete Utah Mortgage Guide

Buying a home in Utah or refinancing your current mortgage? You’re in the right place. This comprehensive guide helps you compare Utah mortgage rates, understand your home loan options, find trusted mortgage lenders, and use tools like our mortgage calculator to estimate payments and plan ahead.

Stay informed on the current mortgage rates, explore first-time home buyer programs, or get started with a mortgage preapproval. Whether you’re a seasoned buyer or new to the process, MortgageRateUtah.com is your go-to resource for navigating the path to homeownership.

Check Current Mortgage Rates in Utah

Understanding mortgage rates today is the first step toward smart borrowing. Rates shift daily, influenced by economic conditions, inflation, and Federal Reserve decisions. You can view up-to-date rates directly on our site.

See Today’s Rates

Use our mortgage calculator, home loan calculator, or amortization calculator to project your monthly payments based on real-time rates. Need to see what your VA entitlement qualifies you for? Try our VA loan calculator.

Explore the Best Mortgage Loan Options

At MortgageRateUtah.com, we break down the top lending programs:

1. FHA & Conventional Home Loans

Perfect for new buyers and those with solid credit. Use our FHA loan calculator to evaluate your options.

2. VA Loans for Veterans

Our tools and resources help Utah veterans compare VA home loan rates, VA loan interest rate options, and get pre-approved through our trusted mortgage lenders. Learn more at VA Loans.

3. USDA Home Loans

Live in a rural area? USDA loans may offer 100% financing options.

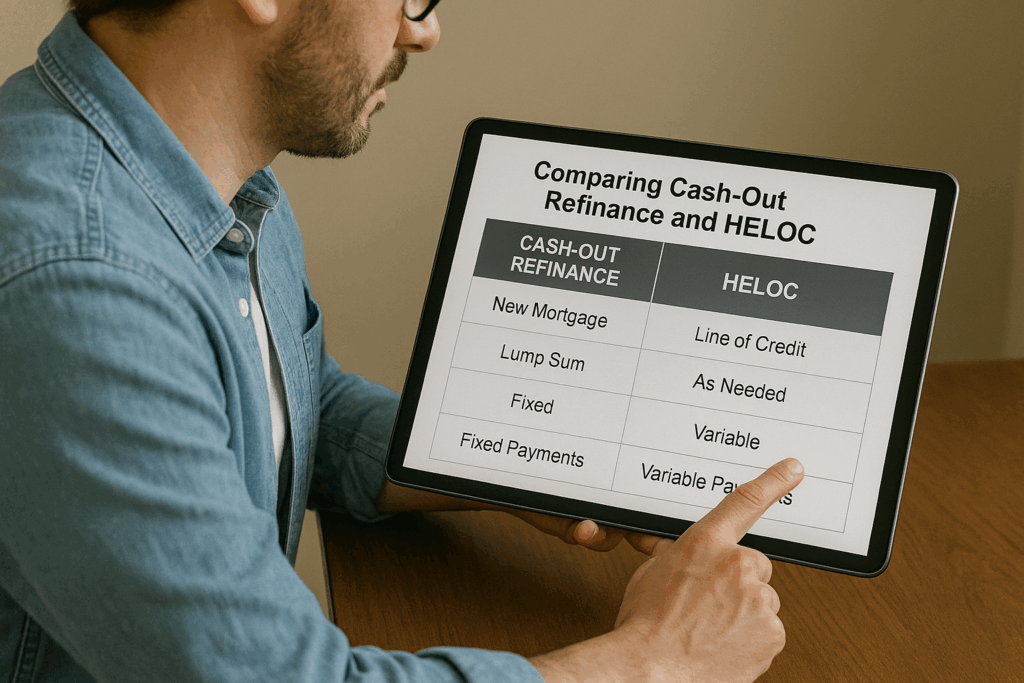

4. Home Equity & HELOC Loans

Need to access home equity? Learn about home equity loans, HELOC, and compare home equity line of credit rates and the best HELOC lenders. Also, consider a cash-out refinance if you want to use your home’s value for major expenses.

Compare Mortgage Companies & Lenders

Looking for the best mortgage companies or a mortgage broker near me in Utah? We help you compare mortgage lenders—from local credit unions to national leaders like:

Our mortgage comparison tool helps you match with the right lender based on your goals, be it a reverse mortgage, second mortgage, or construction loan.

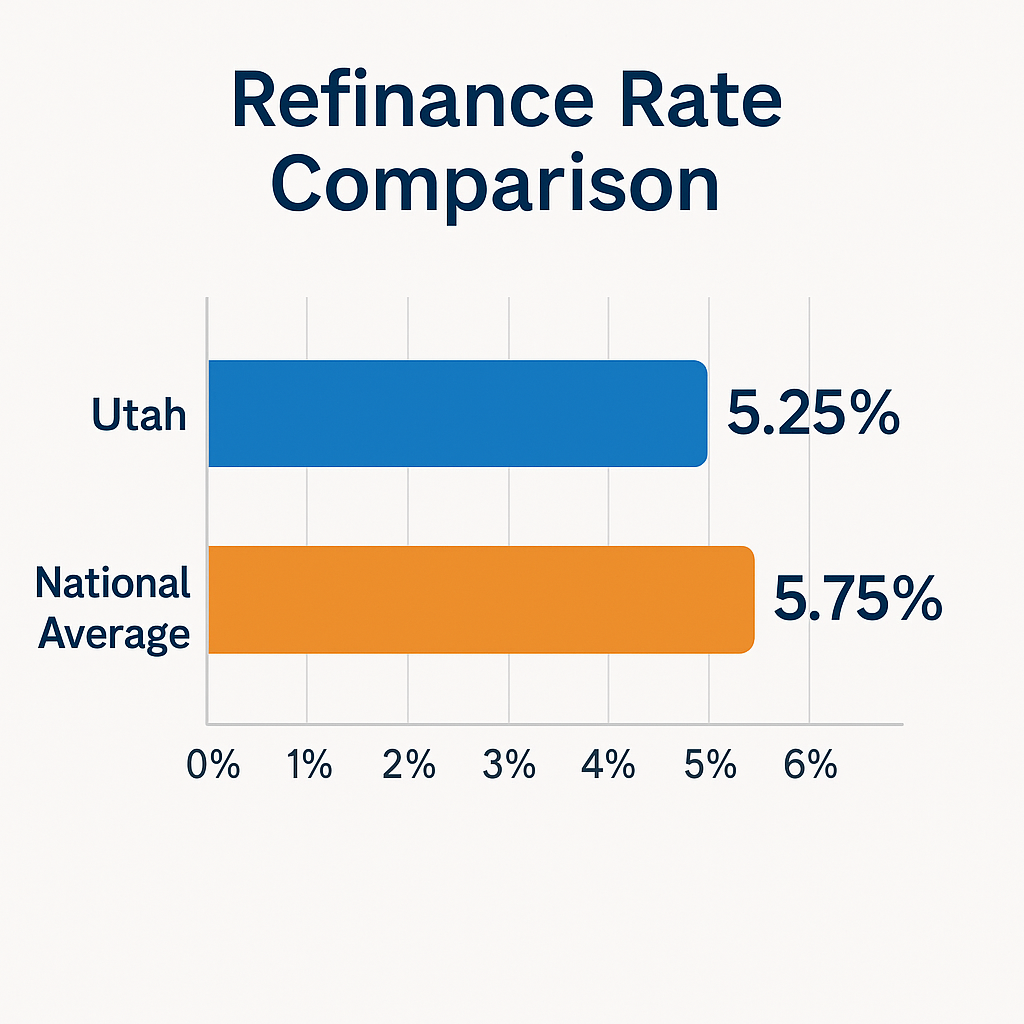

Refinance & Save with Better Rates

Already a homeowner? Explore options to refinance a home loan, lower payments with refinance rates, or unlock equity with a cash-out refinance.

Use our tools:

We’ll help you compare refinance mortgage rates and determine if switching to the lowest mortgage rates can reduce your total loan cost.

First-Time Homebuyer Support in Utah

Utah offers excellent first-time home buyer programs and grants. We also partner with lenders offering first-time home buyer loans with lower down payments, flexible credit requirements, and fast closings.

Helpful Tools & Calculators

We provide powerful calculators to help you plan and budget:

- Mortgage Calculator

- VA Home Loan Calculator

- Reverse Mortgage Calculator

- Mortgage Affordability Calculator

These tools provide peace of mind and financial clarity, whether you’re looking for the best home equity loans, the best HELOCS, or home improvement loans.

Ready to Apply for a Mortgage?

When you’re ready, take the next step. Use our easy online application to apply for a mortgage, get mortgage pre-approval, and request a free mortgage quote from our network of vetted mortgage brokers and mortgage companies.

Conclusion: Your Trusted Utah Mortgage Resource

MortgageRateUtah.com brings you accurate, up-to-date tools and expert content to simplify your homebuying or refinancing experience. From comparing home loan interest rates to calculating VA loan interest rates, equity loan options, or reverse mortgage companies, we’ve got you covered.

Still have questions? Contact our Utah-based experts for a personalized consultation.