Choosing the Right Mortgage in Utah

When buying a home in Utah, one of the most important decisions you’ll face is choosing

between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). With interest rates

fluctuating and the Utah housing market growing rapidly, understanding the pros and cons of

each can help you make a smart, long-term financial decision.

In this article, we’ll walk through the key differences between fixed and adjustable loans, how

adjustable-rate mortgages work, and whether an ARM might be right for you. Whether you’re a

first-time home buyer or looking to refinance your home loan, we’ll help you decide with

confidence.

What Is an Adjustable-Rate Mortgage (ARM)?

An adjustable-rate mortgage (ARM) is a type of home loan where the interest rate changes over

time. Unlike a fixed-rate mortgage, which keeps the same interest rate for the entire term, ARMs

begin with a low introductory rate for a set period—usually 5, 7, or 10 years—before adjusting

annually based on current mortgage interest rates.

For example, a 5/1 ARM offers a fixed rate for the first five years, then adjusts every year based

on the market. These adjustments are tied to mortgage index rates and can move your monthly

payment up or down.

Why Are ARMs Popular in Utah Right Now?

With mortgage rates today on the rise, many buyers in Salt Lake City, Ogden, and Lehi are turning to ARMs for affordability. The lower introductory rate can make monthly payments more manageable—especially if you plan to move or refinance before the adjustment period.

ARM vs. Fixed-Rate Mortgage: Key Differences

Let’s compare adjustable-rate mortgages with fixed-rate options using some of the most

searched mortgage-related terms:

| Feature | Adjustable-Rate Mortgage (ARM) | Fixed-Rate Mortgage |

| Initial Rate | Lower | Typically higher |

| Monthly Payment | May increase | Stable |

| Rate Stability | Changes after intro period | Constant |

| Best For | Short-term, flexible buyers | Long-term, stable income |

Use a mortgage payment calculator or home loan calculator to estimate how these differences affect your budget.

When to Consider an ARM in Utah

An ARM may be a smart choice if:

- You plan to move or refinance your home loan within 5–7 years.

- You expect mortgage rates to drop or stabilize.

- You need lower monthly payments to qualify for a larger loan.

First-time home buyers in Utah often choose ARMs to lower their initial housing costs. Use a mortgage calculator to compare scenarios.

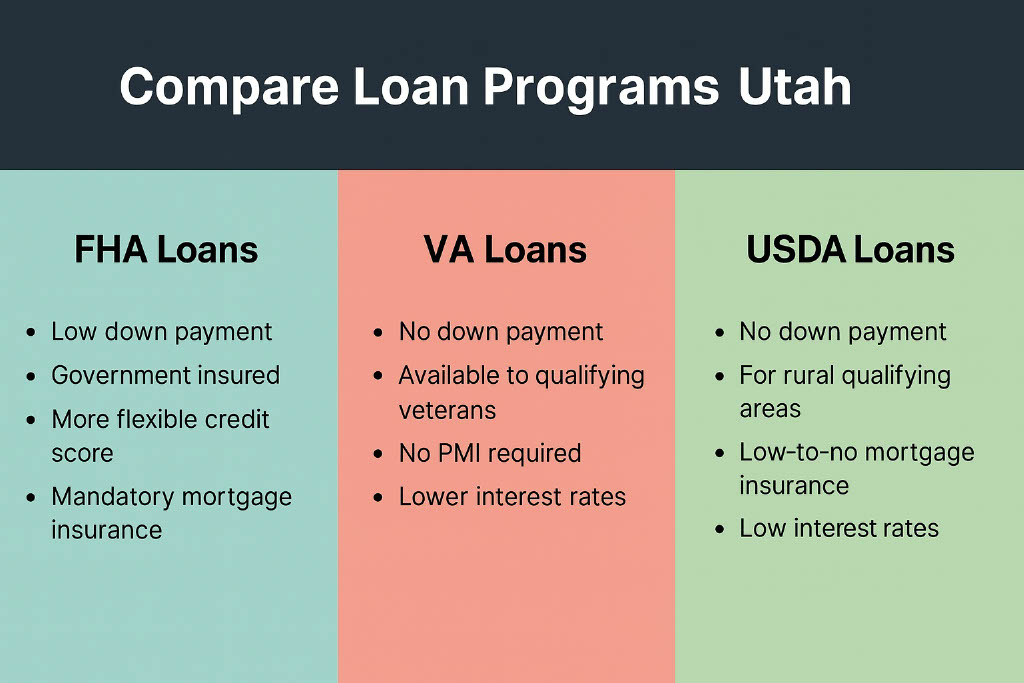

FHA and VA Home Loan Rates in Utah

Many buyers explore FHA mortgage rates and VA home loan rates when considering ARMs. These government-backed loans may allow for lower down payments or easier qualification, especially for first-time home buyer mortgage applicants.

Ask your mortgage broker if an ARM option is available under FHA or VA programs.

Refinancing an ARM Later

An ARM isn’t a lifetime decision. Many Utah homeowners refinance before the adjustment period. Watch refinance mortgage rates, and use a refinance home loan calculator to determine your break-even point. It may be the best time to lock mortgage rates if you’re close to the end of your fixed period.

Final Thoughts – Is an ARM Right for You?

IHere’s a quick checklist:

✔ Do you plan to move or refinance within 5–7 years?

✔ Are you comfortable with potential rate increases?

✔ Do you want to reduce your upfront housing costs?

If yes, an adjustable-rate mortgage in Utah might be a strategic fit.

Ready to Compare Mortgage Rates in Utah?

Before making a final decision, compare mortgage rates side by side and speak with a local mortgage broker. Using tools like a home loan calculator and mortgage pre-approval checklist can help you stay ahead in Utah’s fast-paced housing market.