First-time home buyer programs help new buyers overcome challenges like high down payments and limited credit history. These first-time buyer home solutions often include down payment assistance, flexible credit requirements, and competitive mortgage rates.

In Utah, the Utah Housing Corporation offers specific 1st time home buyer programs, giving locals an affordable path to homeownership.

A common question is: what is a good mortgage credit score?

FHA loans: 580+

Conventional loans: 620+

USDA/VA: Often 640+

Improving your score boosts your odds of prequalify for mortgage approval. Even if your credit isn’t perfect, first time home buyer loan programs are often flexible.

Mortgage Pre-Approval Requirements in Utah

To apply for a mortgage, you’ll need:

Recent pay stubs, W-2s, and tax returns

Bank statements

Employment and asset verification

This is part of the home loan pre approval process, which shows sellers you’re serious.

Don’t confuse prequalification mortgage (an estimate) with mortgage pre approval requirements (fully reviewed by a lender). Pre-approval is stronger and often necessary for your offer to be accepted.

Step-by-Step: How to Get a Mortgage Loan in Utah

Here’s the path to how to get a mortgage loan in Utah:

Prequalify for a home loan

Work with a trusted local lender

Choose a program (FHA, VA, USDA, etc.)

Complete the apply for home loan steps

Get your offer accepted and close

Knowing how to get a mortgage gives you the power to act quickly when you find your dream home.

For a more information about Mortgages Rates, Lenders and Tools, check out this article.

Mortgage Affordability

Your mortgage home affordability depends on:

Credit score

Debt-to-income ratio

Income and assets

Loan type

If you’re asking “How much mortgage can I qualify for?” try an online mortgage calculator or speak with a lender for a customized estimate.

Apply for a Mortgage Loan: What to Expect

When you’re ready to move forward, it’s time to apply for mortgage loan options with your chosen lender.

Be ready to:

Verify your income

Share employment info

Choose your loan program

Some lenders allow you to apply for a home loan online in just minutes.

Best Mortgage Lenders for First Time Buyers in Utah

Looking for the best mortgage lenders for first time buyers? Look for lenders who:

Offer first time home buyer loans

Are familiar with Utah-specific grants

Provide fast home loan pre-qualification

Walk you through prequalify for mortgage steps

Working with a local lender means personalized service and faster turnaround—essential for first-time buyers in a competitive market.

Conclusion

You don’t need perfect credit or a giant down payment to buy your first home in Utah. With the right first time home owner loan programs, and support from experienced lenders, your path to homeownership is absolutely within reach.

Whether you’re ready to apply for a mortgage, prequalify for a home loan, or just want to understand your options, now is the perfect time to start.

Buying your first home is a milestone, and for most people, it starts with securing the right mortgage. But with so many options out there, it can be difficult to know where to begin. In this guide, we’ll walk you through how to apply for a mortgage as a first-time home buyer, how to compare the best mortgage companies, and how to use tools like a first-time home buyer mortgage calculator to stay on track.

How to Apply for a Mortgage First-Time Home Buyer

The mortgage process can seem intimidating, but the steps are straightforward once you understand them. If you’re wondering how to apply for a mortgage first-time home buyer, it starts with evaluating your financial health—your credit score, income, debt-to-income ratio, and savings.

Once you’re ready, the next step is to find a lender and begin your fha first time home buyer loan application if you qualify. FHA loans are government-backed loans that offer lower credit score requirements and down payments, making them ideal for first-time homebuyers.

Get Pre-Approved for First-Time Home Buyer Loans

Before house hunting, it’s smart to get pre approved for first-time home buyer financing. This shows sellers you’re serious and helps you set a realistic budget. Preapproval involves submitting documentation like pay stubs, tax returns, and bank statements.

You may also choose to prequalify for home loan first-time buyer programs first. This is a softer check that gives you an estimate of what you can borrow without a hard credit pull.

Top Mortgage Lenders for First-Time Home Buyers

Not all lenders are created equal. Finding the best mortgage companies for first-time homebuyers means researching those with competitive rates, strong reputations, and helpful loan officers.

Some of the top mortgage lenders for first-time home buyers offer programs tailored to new buyers, such as:

Flexible credit requirements

Down payment assistance

Education resources

When you compare the best lenders for first-time homebuyers, be sure to evaluate customer reviews, loan offerings, and accessibility—especially if you prefer to get pre approved for a home loan online.

Using a First-Time Home Buyer Mortgage Calculator

A first-time home buyer mortgage calculator is one of the most helpful tools during your home-buying journey. These calculators estimate your monthly payment based on factors like loan amount, interest rate, and term.

Pair this with a first-time home buyer down payment calculator to estimate how much money you’ll need upfront, including taxes, insurance, and closing costs.

Housing Loan Amortization and Early Payoff Tools

Understanding the long-term impact of your mortgage is important. Use a housing loan amortization calculator to break down your loan over time and see how much goes toward principal and interest.

Want to pay off your mortgage sooner? A home loan early payoff calculator and a mortgage amortization schedule with extra payments will show you how even small additional payments can reduce the total interest paid and the life of your loan.

Getting Approved for a Mortgage First-Time Buyer: What You Need

Many ask, “What does it take for getting approved for a mortgage first-time buyer?” The short answer: solid financials, documented income, manageable debt, and a good credit score.

If you’re wondering if you can get a mortgage if you have bad credit, the answer is yes—particularly through FHA or specialized first-time buyer programs. The key is finding a lender willing to work with your situation.

Where to Apply for First-Time Home Buyer Loans

So, where to apply for first-time home buyer loans? You have options:

Traditional banks and credit unions

Online mortgage lenders

Government-backed programs through HUD or FHA

Each has pros and cons. If you prefer a fast, digital process, online lenders let you apply for a mortgage before finding a house and complete most steps from your computer.

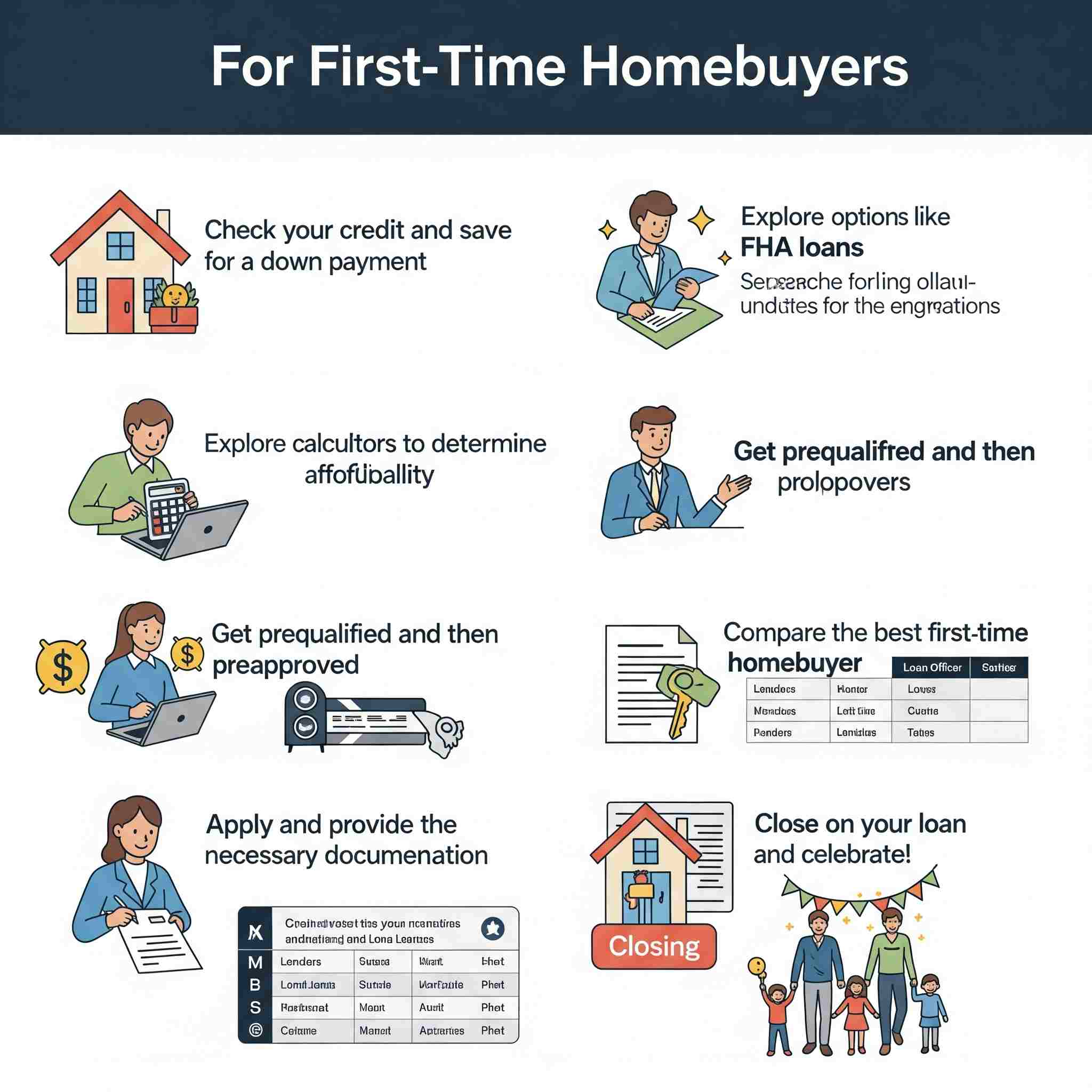

How to Get a Home Loan for the First Time

Still unsure how to get a home loan for the first time? Here’s a quick summary:

Check your credit and save for a down payment.

Explore options like FHA loans.

Use calculators to determine affordability.

Get prequalified and then preapproved.

Compare the best first-time homebuyer lenders.

Apply and provide the necessary documentation.

Close on your loan and celebrate!

When Should I Get Pre-Approved for a Mortgage Loan?

If you’re asking, when should I get pre-approved for a mortgage loan? The answer is simple: before you begin house hunting. Preapproval helps define your price range and makes your offers more attractive to sellers.

Can I Get Pre-Approved for a Home Loan Online?

Absolutely. Many of the best mortgage companies for first-time buyers offer easy online applications. This convenience allows you to compare rates, upload documents, and get results quickly—all from home.

Final Thoughts

Navigating the mortgage process doesn’t have to be overwhelming. From filling out your FHA first-time home buyer loan application to using a first-time home buyer mortgage calculator or finding the best mortgage lenders for first-time buyers, you have a wealth of tools and options available.

Mortgage rates determine how much interest you will pay on a home loan. These rates fluctuate based on economic factors such as inflation, Federal Reserve policies, and local housing market conditions. Whether you’re a first-time homebuyer or a homeowner looking to refinance, understanding current mortgage rates in Utah can help you make informed financial decisions.

Current Mortgage Rate Trends in Utah

Mortgage rates in Utah are affected by market demand, lender competition, and national interest rate policies. As of February 6, 2025, interest rates have been fluctuating due to economic uncertainty and inflation concerns (as seen in the image to the left). For the latest national mortgage rate data, you can refer to Freddie Mac’s Primary Mortgage Market Survey. Homebuyers looking to lock in a mortgage should consider fixed-rate vs. adjustable-rate loans, depending on their long-term financial goals.

Types of Home Loans Available in Utah

Choosing the right mortgage is essential. In Utah, homebuyers can explore options such as:

Conventional Loans –

Best for buyers with strong credit and a solid down payment.

FHA Loans –

Ideal for first-time buyers with lower credit scores and smaller down payments.

VA Loans –

Designed for veterans and active-duty military members with benefits like no down payment.

Jumbo Loans –

Suitable for purchasing high-value homes beyond conventional loan limits.

Not sure which loan is right for you? Our First-Time Homebuyers Guide breaks down everything you need to know about qualifying for a mortgage and choosing the best loan option.

Should You Lock in Your Rate?

Given current volatility, many borrowers are asking: Should I lock in my mortgage rate now?

If rates are expected to rise, locking in a rate now could save money.

If rates may decrease, some lenders offer “float-down” options that allow you to secure a lower rate before closing.

Is Now the Right Time to Refinance?

Refinancing can help homeowners lower their monthly payments or switch to a better loan term. Utah homeowners should monitor interest rates and consider rate-and-term refinancing to reduce costs or cash-out refinancing for home improvement projects.

How to Get the Best Mortgage Rate in Utah

To secure the most competitive mortgage rate, consider:

Improving Your Credit Score –

A higher score qualifies for lower rates.

Comparing Lenders –

Rates and fees vary between banks and mortgage companies.

Locking in Rates at the Right Time –

Interest rates fluctuate, so timing matters.

Final Thoughts & Resources

Navigating mortgage rates and loan options can feel overwhelming, but understanding the basics can empower you to make the best financial decision. Check out ourMortgage Calculator to estimate your monthly payments, or visit this Loan Comparison Calculator to explore different mortgage options. For more expert insights, visitBankrate’s Mortgage Resources for the latest industry updates.

Since the beginning of our country, buying a home has been a staple of what it means to be successful, representing the “American Dream” for many. However, there are quite a few barriers to home buying that may seem daunting for first-time home buyers in Utah. How will I secure the funds for a down payment? How long should I expect to be making payments? What tools are available to guide me along the process? These are but a few of the questions first-time homebuyers in Utah weigh when making this decision, making it difficult to know where to start. In this article, we are going to dig deeper to see if it really is as difficult as they say for young adults to buy their first homes in Utah and what resources they can use to help with the process!

Who is a “First-Time Home buyer” in Utah?

A first-time homebuyer in Utah is someone purchasing a primary residence for the first time or someone who hasn’t owned a home in the past three years. To meet first-time homebuyer Utah qualifications, buyers must typically meet specific income limits and credit requirements, depending on the program they apply for.

Programs like the Utah State First-Time Home Buyer Program and Utah Housing First-Time Home Buyer Grant provide financial assistance and favorable terms for eligible buyers. These programs offer a range of first-time homebuyer Utah benefits, including down payment assistance and lower interest rates.

Common Perceptions About Young First-Time Homebuyers in Utah

Many believe that buying a home in Utah is nearly impossible for young people, especially in competitive markets like Salt Lake City. Many young adults have expressed their worries about ever hoping to buy a home, while older generations question the validity of their complaints. This brings to light a serious question: are the issues with the market or personal issues that are truly affecting the rate at which young people buy their first property?

Are the requirements for first-time home buyers in Utah to secure a first-time mortgage realistic in this economy, or are young home buyers irresponsible with their purchasing habits, leading them to be stuck in these difficult situations?

The Scary Reality of Buying a Home as a First-Time Homebuyer

Recent reports have shown that there is a real challenge for potential young home buyers. The average age of first-time home buyers in Utah has jumped a staggering 10 years since 1991. As of 2024, the median age that a person buys a home for the first time had jumped from 28 to 38, meaning that this person spends a good portion of their early career saving up just to find a home. And with delinquency rates rising for first-time buyers in Utah, it is clear that there are significant strains for first-time home buyers in Utah.

While these challenges may leave you screaming like the man above, the situation isn’t as bleak as it may seem. Many first-time home buyers in Utah are successfully purchasing homes by leveraging first-time home buyer assistance Utah programs, grants, and favorable loan options. These initiatives offer first-time mortgages with competitive first-time homebuyer interest rates and support for covering down payments. Factors like credit scores and income limits can be hurdles, but they are not impossible to overcome. By improving credit, budgeting wisely, and exploring various Utah first-time home buyer help programs, young buyers can find opportunities to purchase homes.

How To Achieve Your Dream of Buying a Home

Here’s a step-by-step guide to help younger buyers navigate the first-time homebuyer tips process in Utah:

Assess Your Finances: Review your credit score and understand the first-time home buyer Utah qualifications. Use a first-time home buyer mortgage calculator to estimate what you can afford.

Explore First-Time Buyer Programs in Utah: Look into the best first-time home buyer programs Utah offers, such as the Utah State First-Time Home Buyer Program and Utah Housing First-Time Home Buyer Grant.

Get Pre-Approved for a Mortgage: Strengthen your offer by getting pre-approved for first-time mortgages. This shows sellers you are serious and financially prepared.

Find a Real Estate Agent: Work with an agent experienced in helping first-time home buyers in Utah. They can guide you through the process and identify properties that meet your needs.

Buying a home in Utah can be challenging for first-time buyers due to rising prices, student debt, and credit requirements, but it is achievable with the right resources. Programs like the Utah State First-Time Home Buyer Program and Utah Housing grants offer financial assistance, down payment support, and lower interest rates. By improving credit, managing budgets, and exploring mortgage options, young buyers can increase their chances of homeownership. Researching grants, getting pre-approved for a loan, and working with a real estate agent can simplify the process. With careful planning and the right support, first-time buyers in Utah can confidently achieve their dream of homeownership.

Mortgage rates are the interest charged on home loans. They significantly affect the total cost of homeownership. These rates frequently fluctuate based on inflation, the Federal Reserve’s policies, and market demand. In Utah, mortgage rates depend on credit scores, loan types, and lender policies. Therefore, understanding these factors helps homebuyers make informed financial decisions when refinancing or purchasing a home.

Current Mortgage Trends in Utah

Recently, Utah’s real estate market has seen rising interest rates, which have affected housing affordability. As a result, homebuyers should actively track mortgage rates and compare adjustable vs. fixed-rate options. Since federal and local factors influence Utah’s home-buying rates, staying informed allows buyers to choose the best loan for their situation.

How Interest Rates in Utah Are Determined

Market conditions, housing supply, and demand primarily determine Utah’s interest rates. Although buyers cannot control these factors, they can improve their credit scores to secure lower rates. Since low credit scores lead to higher interest rates, improving creditworthiness is crucial. Furthermore, comparing mortgage providers is essential, as different lenders offer varying rates. Additionally, researching fees and prepayment penalties before choosing a mortgage can help avoid unexpected costs.

These loans have a stable interest rate throughout the term. As a result, they offer predictable monthly payments, making them ideal for long-term loans (10+ years). However, they typically start with higher rates than ARMs. Moreover, if market rates drop, borrowers cannot adjust their original rate.

Adjustable-Rate Mortgages (ARM)

These loans start with a lower interest rate but adjust based on market conditions. Consequently, they work well for short-term loans or those planning to refinance or sell soon. However, rates can rise over time, leading to unpredictable payments. Therefore, ARMs are riskier for long-term borrowers.

Should You Refinance Your Mortgage?

Refinancing replaces an existing mortgage with a new one. Many homeowners refinance to lower rates, reduce monthly payments, or access home equity. Even a slight rate drop can lead to significant savings. Additionally, refinancing can shorten loan terms or switch an ARM to an FRM for stability.

If you’re a homeowner considering refinance rates in Utah or a first-time homebuyer navigating the mortgage process, it’s important to understand mortgage rates in Utah. Comparing fixed vs. adjustable-rate mortgages, observing current interest rates, and using tools like mortgage calculators can help secure the best possible loan. Advising with local lenders and researching Utah home loan options can offer insights aligned with your financial goals. For more detailed guidance, check out our first-time homebuyer resources and refinancing insights to take the next step toward homeownership.

Buying a home for the first time is an exciting yet complex journey, especially when it comes to securing a mortgage, so If you’re a first-time homebuyer in Utah, navigating the various loan options, understanding mortgage rates, and preparing your finances can feel overwhelming. However, with the right guidance, you can confidently make one of the most important financial decisions of your life.

In this guide, we’ll walk you through everything you need to know about getting a mortgage in Utah as a first-time home buyer. We’ll cover different mortgage types, loan programs available in Utah, how to compare interest rates, and mistakes to avoid. By the end, you’ll have a clear strategy to secure the best possible mortgage and move forward with confidence.

What is a Mortgage and How Does It Work?

Mortgage Basics

A mortgage is a loan used to purchase a home because most buyers don’t have the full purchase price in cash, they borrow money from a lender and agree to repay it over time. That is to say that the home itself acts as collateral, meaning if the borrower fails to make payments, the lender can take possession of the property through foreclosure.

Mortgage payments typically consist of four main components:

Principal – The amount borrowed.

Interest – The lender’s fee for lending money.

Property Taxes – Local taxes based on the home’s value.

Homeowners Insurance – Protection against property damage.

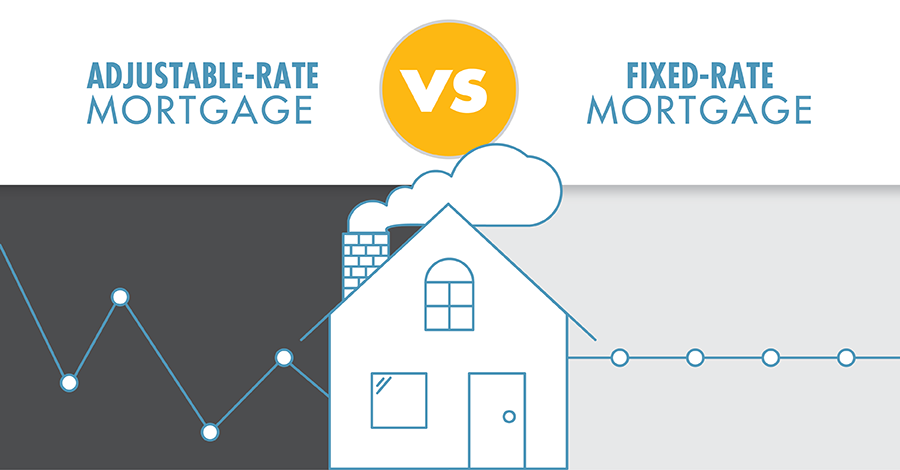

Choosing the right mortgage depends on various factors, including your financial stability, future plans, and current interest rates, so one of the first decisions you’ll make is whether to get a fixed-rate or adjustable-rate mortgage.

Fixed-Rate vs. Adjustable-Rate Mortgages

Fixed-Rate Mortgage (FRM)

The interest rate remains the same throughout the loan term

Monthly payments are predictable, making budgeting easier.

Suitable for long-term home ownership.

Adjustable-Rate Mortgage (ARM)

The interest rate starts lower but adjusts periodically based on market conditions.

Can be beneficial if you plan to sell your home within a few years.

Carries higher financial risk if rates increase.

How to Prepare for Buying Your First Home in Utah

Before applying for a mortgage, first-time homebuyers should take several key steps to ensure they qualify for the best loan terms.

Check and Improve Your Credit Score

Your credit score is a critical factor in determining your mortgage interest rate. Lenders use it to assess your financial reliability.

A FICO score of 740+ qualifies for the lowest interest rates.

If your score is below 620, your mortgage options may be limited, and your interest rate will be higher.

If your score is low, focus on paying down debt, avoiding late payments, and maintaining a low credit utilization ratio before applying for a mortgage.

Save for a Down Payment

In Utah, the average down payment ranges between 5% and 20% of the home’s purchase price.

A higher down payment often means lower monthly payments and interest rates.

Some first-time buyer programs allow down payments as low as 3.5% (FHA loans) or 0% (VA and USDA loans).

Get Pre-Approved for a Mortgage

Mortgage pre-approval helps you understand your budget and strengthens your offer when negotiating with sellers.

Lenders evaluate your income, debt-to-income ratio (DTI), and credit history before approving a loan.

Great Mortgage Options for First-Time Home buyers in Utah

Utah offers several mortgage programs designed to help first-time homebuyers secure an affordable loan.

Housing Corporation Loan Programs

First Home Loan

Designed for low-to-moderate income buyers.

Offers down payment assistance programs.

Score Loan

Requires a credit score of 620+.

Allows for higher debt-to-income ratios compared to traditional loans.

Government-Backed Loans

FHA Loan (Federal Housing Administration Loan)

Minimum 3.5% down payment.

Requires a credit score of 580+.

VA Loan (For Veterans & Active Military)

No down payment required.

No Private Mortgage Insurance (PMI) needed.

USDA Loan (For Rural Areas)

No down payment required for eligible rural homebuyers.

Must meet income eligibility guidelines.

These are some options for Utah Mortgage for first home buyers. If you want to know more detail information, you can click here, UHC site. You can find more deep information about programs.

How to Compare Mortgage Interest Rates in Utah

Finding the Great Mortgage Rates

As of 2024, the average mortgage rate in Utah is around 6.5%.

Rates fluctuate, so checking multiple lenders and comparison sites is crucial.

30-year vs. 15-year mortgages—longer terms often have higher interest rates.

APR (Annual Percentage Rate):

Includes interest rate + additional fees.

Lender Type:

Compare local lenders, banks, and credit unions for the best deal

Common Mistakes First-Time Home buyers Should Avoid

Overextending Your Budget – Buying a home that exceeds your financial capacity can cause stress.

Ignoring Hidden Costs – Consider property taxes, HOA fees, and maintenance costs.

Skipping Mortgage Pre-Approval – Without pre-approval, sellers may not take your offer seriously.

Conclusion

Buying a home in Utah as a first-time homebuyer can be an exciting yet complex process, but with the right preparation and knowledge, you can secure the best mortgage for your needs. Understanding the different loan options, improving your credit score, saving for a down payment, and getting pre-approved are all crucial steps to ensure a smooth home-buying experience. Additionally, comparing mortgage rates from multiple lenders and avoiding common mistakes, such as overextending your budget or neglecting hidden costs, can help you make a financially sound decision. By taking the time to research and plan, you can confidently move forward in purchasing your first home in Utah, knowing that you have chosen the best mortgage option available. If you need further assistance, consulting a mortgage expert can provide valuable insights tailored to your financial situation.

If you want to get more tips for Utah Mortgage, you can click here.

Are you ready to buy your first home? Take our quiz to find out: (Link to internal quiz)

For Sale Real Estate Sign in Front of New House.

Are you a first-time home buyer? Buying a home is one of the largest financial decisions you will ever make! Unless you can pay in cash, you’ll need a mortgage. A mortgage is a loan for purchasing real estate, typically offered by banks with interest rates between 4%-6%. Over 30-year mortgage rates in Utah, these interest rates can significantly increase the cost of your home. The property serves as collateral, meaning if you default on payments, the bank can foreclose and take possession of the home. Understanding the mortgage process can help save time, money, and stress. Learn more about affordability and your rights as a first-time home buyer at: https://www.hud.gov/topics/buying_a_home

The Basics

Principal:

This is the amount of money you borrow. For example, if you buy a home for $450,000 and put down a $90,000 down payment, the mortgage principal will be $360,000. You should put down at least 20% of whatever the total cost of the home is. While you may go as low as 3%, that is not suggested. If you are unable to put down 20%, consider saving a little longer. This website explains FHA loans and how they can help you afford your first home!

Home interest rates in Utah:

This is what the lender charges you for borrowing the money. Local bank mortgage rates can vary based on your credit score, the type of loan, and market conditions. There are many benefits to being a first-time home buyer in Utah, be sure to talk to your bank about opportunities available to you!

Term:

The length of time you must repay the mortgage. Common terms are 15, 20, or 30 years. Now terms go all the way up to 40 years!

Mortgage Insurance Rate:

If your down payment is less than 20%, you may have to pay for private mortgage insurance (PMI). This protects your bank in case you default on your loan.

The Process

There are many different types of loans, and it is important to choose the one that is best for you. As a first-time home buyer, the process can be very overwhelming. If you aren’t sure what is best for you, starthere!

Step 1: Pre-Approval

Before you start shopping for a home, it’s smart to get pre-approved for a mortgage. A pre-approval gives you an idea of how much you can borrow based on your financial situation. The lender will check your credit score, income, assets, and debts to determine how much they’re willing to lend. You can do a less formal version of this here: mortgage calculator.

Step 2: House Hunting and Making an Offer

Once you’re pre-approved, you can begin searching for homes within your budget. A great place to start is Zillow. With Zillow, you are able to view thousands of homes from your phone! When you find a house you love, you’ll make an offer to the seller. If the offer is accepted, the next step is securing your mortgage

Step 3: Apply for the Mortgage

Now it’s time to submit a formal application. Your local bank mortgage rates will affect your monthly payments. Your bank will ask for documentation to verify your income, employment, and assets. They’ll also schedule an appraisal to ensure the home’s value aligns with the loan amount. You should also get your new home inspected through a third party to ensure you know the status of the home before purchasing.

Step 4: Loan Underwriting

This is the behind-the-scenes work where the lender verifies all your information, reviews the appraisal, and assesses the risk of lending to you. This stage can take several weeks and may require additional documentation. But mostly, you can sit back and let the bank do the heavy lifting for you.

Step 5: Closing

Once the loan is approved, you’ll go to a closing meeting where you sign the final paperwork and pay any closing costs, which can include fees for the appraisal, title insurance, and legal services. After this, the mortgage is officially in place, and you are a first-time homebuyer!

Lowest Mortgage Rates in Utah

Mortgages may seem complex at first, but understanding the basics can make the process less intimidating. When comparing options, look for the lowest mortgage rates Utah and consider if your Utah mortgage rate chart aligns with your financial goals. Some banks offer the lowest mortgage rates, especially those with programs aimed at first-time home buyers seeking the best interest rates.

You may also want to explore federal housing association (FHA) rates Utah or (FHA) mortgage rate in Utah, as these can be beneficial for buyers with lower credit scores or smaller down payments. Understanding 30-year mortgage rates in Utah and how mortgage insurance rate impacts your overall costs is key when making such a big decision.

A spacious, modern home with elegant evening lighting. Discover financing options like a Jumbo loan to make this dream home possible.

Utah Mortgage Rates as of September 22, 2024

This past week, we have seen a slight decrease in rate with most of the mortgage types and a slight increase in rates for Conventional 15 Year Fixed Utah Mortgages. By far the most substantial change over the past week is with the fixed Utah FHA mortgage loans which saw a decrease of .54% in the 30 year fixed Utah FHA mortgage rate and a whopping 1.47% decrease in the 15 year fixed Utah FHA mortgage rate. After a bit of a rate hike over the past couple of weeks, it’s nice to see the rates fall a bit, even if it’s not by much. Even though rates have fallen over the past week, I would recommend that most potential Utah home buyers wait another week before checking the rates again. Utah mortgage rates have been steadily decreasing over the past three months but we have seen a spike over the past couple of weeks and we are currently at the peak of the spike. Therefore I recommend waiting to apply for a mortgage for potential Utah home buyers. On the other hand, if the home buyer qualifies for a Utah FHA mortgage loan, then I would recommend they consider applying for a mortgage due to the steep drop the mortgage type experienced. Keep reading if you want to know if you qualify for a Utah FHA mortgage loan, as well as information and directories for all other major mortgage types.

Current Utah Mortgage Rates for Conventional Loans Analysis

If you’re considering a Conventional Home Loan in Utah, it’s essential to understand how the current Utah mortgage rates and Utah interest rates can impact your decision. These loans typically appeal to buyers with a strong credit history and a stable income looking for stability and predictable payments. The current average interest rate for a 30 year fixed Utah conventional mortgage loan is 5.73%, which has dropped by 0.04% in the past week. The average interest rate for a 15 year fixed Utah conventional mortgage loan is 5.12%, which has risen by 0.03% in the past week. While there’s been a slight increase in Utah 15 Year interest rates, the average Utah mortgage rates for conventional loans can vary. With the recent fluctuations, particularly the drop in Utah 30 Year interest rates, now might be a good time to explore your options.

Current Utah Mortgage Rates for VA Loans Analysis

If you served in the military, then you should really consider applying for a VA loan. Utah VA loans come from a mortgage loan program offered by the Department of Veterans Affairs. These loans are exclusively for veterans, service members, and their families in purchasing, refinancing, building, repairing, or improving their home. Private lenders like banks and mortgage companies offer these loans, but those eligible are able to get better loan terms than with a conventional loan since the VA guarantees a portion of the loan. In order to qualify for a VA loan, you have to request a Certificate of Eligibility. This certificate contains information on your service history and duty status. You can find out if you meet the credentials for a Certificate of Eligibility here. The limits for VA home loans are the same as FHFA limits, which are Conforming Loan Limits. The 2024 limits sorted by county can be found on the FHFA website.

The current average interest rate for a 30 year fixed mortgage rate VA loan is 5.48%, which has dropped by 0.06% in the past week. The average interest rate for a 15 year fixed mortgage rate VA loan is 5.38%, which has dropped by 0.03% in the past week. For the most part, these rates are noticeably lower than the other rate options.

To learn more information about VA loans and if it’s the right loan for you, visit this post on our blog dedicated toVA loans.

Current Utah Mortgage Rates for FHA Loans Analysis

For those exploring FHA Loans in Utah, this option is ideal for first-time homebuyers, individuals with limited savings for a down payment, or those with less-than-perfect credit histories. These loans are particularly beneficial for buyers who may struggle to meet the stricter requirements of conventional financing. Recently, we’ve seen a significant drop in the FHA 30 Year Fixed Mortgage Rate, now at 6.27% after a decrease of 0.54%, and the FHA 15 Year Fixed Mortgage Rate has reached 6.18% with an impressive 1.47% decrease—the largest drop among loans. With these favorable rates, now is a great time to consider this route. To learn more about FHA loans and their benefits, check out this blog post all about FHA loans.

Current Utah Mortgage Rates for Jumbo Loans Analysis

If you plan on buying a home for over $766,550, then you need to apply for a jumbo loan. A Utah jumbo loan is a mortgage used to finance properties that financially exceed a conventional conforming loan. In most counties in Utah, the maximum amount for a conforming loan for a single unit house is $766,550. But if you intend to move to Summit or Wasatch county, then the limit is $1,149,825 while the limit in Wayne county is $997,050. You can see jumbo loan limits by Utah county here. Jumbo loan limits are determined by the Federal Housing Finance Agency every year, and also varies by house size (single unit, duplex, etc.) Homes that exceed the local conforming loan limit require a jumbo loan in Utah, and are usually used for high-value properties. Jumbo loans have stricter criteria for borrowers: a higher credit score, larger income/assets, and bigger down payments. Therefore, they can vary significantly based on the borrower’s creditworthiness, income, and overall financial profile.

In the current market, the average 30-year fixed jumbo mortgage APR stands at 6.13%, decreasing 0.09% from the previous week. The 15-year fixed jumbo mortgage rate is slightly higher at 6.37%, which has decreased by 0.6% in the past week.

Final Summary

Make sure to come back next week for updated information and analysis on current Utah mortgage rates. Make sure to regularly visit our blog, where you can find new information about all of the major mortgage types as well as refinancing. Visit our monthly reddit ama on r/Utah where you can ask a Utah mortgage expert any questions you may have about applying for a mortgage in the state. If there is any information you’d like to know that we don’t seem to have, feel free to message us through our contact page.

“VA-Backed Veterans Home Loans.” Department of Veterans Affairs, www.va.gov/housing-assistance/home-loans/#:~:text=VA%20direct%20and%20VA%2Dbacked,programs%E2%80%94and%20how%20to%20apply. Accessed 24 Sept. 2024.

VA Home Loans, Veterans Benefits Administration. Department of Veterans Affairs, www.benefits.va.gov/homeloans/#:~:text=VA%20helps%20Veterans%2C%20Servicemembers%2C%20and,you%20with%20more%20favorable%20terms. Accessed 24 Sept. 2024.

Dehan, Andrew. “What Is a Jumbo Loan?” Bankrate, 2 Apr. 2024, www.bankrate.com/mortgages/what-is-jumbo-mortgage/.

Banton, Caroline. “Underwriting: Definition and How the Various Types Work.” Investopedia, Investopedia, www.investopedia.com/terms/u/underwriting.asp. Accessed 20 Sept. 2024.

“Jumbo Loans: What You Need to Know.” NerdWallet, www.nerdwallet.com/article/mortgages/jumbo-loans-what-you-need-to-know. Accessed 20 Sept. 2024.

Segal, T. (n.d.). Federal Housing Administration (FHA) loan: Requirements, limits, how to qualify. Investopedia. https://www.investopedia.com/terms/f/fhaloan.asp Conventional loans. Consumer Financial Protection Bureau. (n.d.). https://www.consumerfinance.gov/owning-a-home/conventional-loans/

A VA home loan is a mortgage option available to veterans, active-duty military members, and their families, guaranteed by the U.S. Department of Veterans Affairs (VA). In Utah, VA loans provide several key benefits, including no down payment, no private mortgage insurance (PMI), competitive interest rates, and flexible credit requirements. They also limit closing costs and allow veterans to reuse their benefits. To qualify, applicants must meet specific service criteria, such as active duty during wartime, peacetime, or service in the National Guard or Reserves. In Utah’s competitive housing market, particularly in high-cost areas like Salt Lake City, VA loans can help veterans secure homes with more favorable terms. With the state’s growing real estate market, these loans are especially helpful for veterans looking to buy homes in both urban and rural parts of Utah, making them crucial financial tools for those who have served.

Varieties of VA Home Loan Options

When it comes to VA home loans, there are several flexible and unique options available to veterans, active-duty service members, and their families. Each loan type is designed to cater to specific financial needs and goals, making homeownership more accessible and affordable. Whether you’re purchasing a new home, refinancing an existing mortgage, or looking to tap into your home’s equity, VA loans offer competitive rates and favorable terms. Below, we break down the different types of VA home loan options.

VA Purchase Loan

This loan type allows qualified buyers to purchase a home without needing a down payment, and it often comes with lower Utah mortgage rates than conventional loans.

VA Cash-Out Refinance

This option lets you replace your current mortgage with a new VA loan, helping you access cash by tapping into your home’s equity, with the potential to benefit from Utah VA refinancing rates.

VA Interest Rate Reduction Refinance Loan (IRRRL)

Also known as a streamlined refinance, this loan is designed to help reduce your monthly payments by securing a lower VA loan interest rate Utah on an existing VA loan.

VA Home Loan Lenders in Utah

Finding the right VA home loan lender in Utah is essential for veterans, active-duty service members, and their families looking to take advantage of their VA benefits. Utah has a variety of experienced lenders who specialize in VA loans, offering competitive rates and terms tailored to the unique needs of military borrowers. These lenders understand the specific requirements of VA loans, including no down payment options, lower interest rates, and no private mortgage insurance, making home ownership more affordable. For a full list of reputable lenders offering VA and other mortgage options,

Choosing a trusted VA lender ensures you get the support and expertise needed throughout the home-buying process. Ensuring you’re partnering with the right bank is crucial before making an important decision such as a mortgage.

As in other states, Utah military mortgage rates are frequently linked to VA loans, which provide a number of advantages to qualifying spouses, veterans, and active-duty military personnel. Military families find VA loans to be an appealing alternative since they often have lower interest rates than regular mortgages, no down payment requirements, and no private mortgage insurance (PMI). Both home purchases and mortgage refinancing are possible with these specific loans in Utah. VA loan Utah requirements are typically straightforward and designed to meet the financial needs of service people, but VA loan interest rates Utah can vary depending on the lender, the borrower’s credit history, and the state of the market.

Summary:

Guaranteed by the U.S. Department of Veterans Affairs, a VA home loan Utah is a great option for veterans, active-duty members, and their families. In Utah specifically, these loans are especially useful because of the benefits they offer, including lower interest rates, no private mortgage insurance (PMI), and no down payment. Adding to that, they are also extremely flexible and can be tailored specifically to meet diverse financial needs and circumstances. These options not only enhance affordability but also empower veterans to make smart financial decisions while homebuying. Considering Utah’s highly competitive real estate market, these types of loans are especially great for those who are seeking a home.

On the website Mortgagerateutah.com, they provide lists of the best mortgage banks and brokers in Utah. The page is designed to be intuitive and easy to navigate, which can help veterans access VA home loans with ease. The website also offers specific tabs dedicated to VA loans, showing insights into lenders who specialize in the field, along with additional resources to help the navigation/decision process for military families. The variety of options reflects a commitment to helping veterans achieve their dream home-buying experience.

For more details on the benefits and general information on VA loans

Here we highlight the benefits of VA loans, whether you qualify for one, and how to apply.

Other Places to Help:

This subreddit is a community for veterans to navigate their finances after serving our country. The members discuss a wide variety of topics, with VA home loans being a large piece of it, so this subreddit makes sense to attract readers to connect and ask questions with others in similar situations.

When my husband and I purchased our first home in Salt Lake City, Utah, it seemed like there were endless forms to fill out and too many documents to sign, followed by at least an hour of signing more closing document to wrap up the sale. The amount of paperwork involved with buying a home feels endless. However, It’s important to know what documents you’re signing at closing, and why you’re signing them because purchasing a home is a huge investment!

Don’t drown in closing document confusion! Read on for help.

I want to help first-time homebuyers understand what they’ll be reviewing during closing, and/or give experienced homebuyers a friendly reminder. So, below is a list of the most common closing documents you’ll encounter and a brief description of what they entail. Documents are in order alphabetically, by name.

The Affidavit of Title

The Affidavit of Title is a legal document which establishes that the seller holds the title to the property. The new homeowner will sign this document upon taking ownership. Also, it includes any information about liens or other title issues for that property.

The Certificate of Occupancy

The Certificate of Occupancy is a document that’s provided to the homebuyer and contains the address and description of the property. It verifies that it us up to code, which serves as proof that the property is fit to live in and fit for its purpose. This document only applies to new-build homes, therefore anyone closing on an existing home doesn’t need to worry about this one.

The Closing Disclosure

A Closing Disclosure is a form for the new homebuyer which gives the final details of the mortgage loan. It includes the loan terms, projected monthly payments, and how much the new homebuyer will pay in fees and other costs to get the mortgage (closing costs).

The Deed

A Deed is a legal document that transfers ownership of home from the current owner to the new buyer. It also contains a description of the property boundaries and any real property that it contains. Therefore, it is crucial to review this document for accuracy. Every real estate deed must be notarized and filed with the local government in order for the new homebuyer to sell the property, refinance the property, or obtain a line of credit on it. The title insurance company generally performs this task, but it’s important for the homebuyer to verify the process.

The Home Inspection Report is a detailed list of the the condition of the home and its components. It generally includes the following: foundation, exterior, bathroom fixtures, appliances, roof, plumbing, HVAC system, gas system, and electrical system. An inspector will visually examine the home and then provide the report. This is done prior to closing so that the buyer can review the document and request fixes to be made or even change their mind about purchasing the property.

The Homeowners Insurance

Lenders in Utah require homeowners insurance, and will ask for proof of insurance as one of the closing documents. Lenders want proof that their investment is protected.

The Initial Escrow Statement

The Initial Escrow Statement also goes by the name of the “Initial Escrow Disclosure”. This document outlines how the escrow account is set up and what expenses it covers. It covers common elements such as property taxes, mortgage insurance, homeowners association dues, etc.

The Loan Application

The Loan Application is the homebuyer’s acknowledgement that they understand the terms of the loan and their financial obligation to repay it. The new homebuyer will review this document along with the mortgage application. Therefore, it is important to review for accuracy and notify of any changes.

The Mortgage

The mortgage also goes by the name “The Deed of Trust.” This is an agreement between the new homebuyer and a lender that allows the homeowner to borrow money to purchase or refinance a home. The mortgage legally allows the lender to put the home up as collateral for the loan.

The Promissory Note describes the homebuyer’s commitment and responsibility to the mortgage loan. It will state the amount of the loan, the interest rate, repayment schedule and any consequences of defaulting.

The Purchase Agreement

The Purchase Agreement is sometimes called a “Purchase and Sale Agreement” or a “Real Estate Purchase Contract (REPC)”. It is a legally binding document between the buyer and seller for real estate purchases. The Purchase Agreement contains details such as: new homebuyer info, purchase date, purchase price, purchase details (property and any included amenities), how it will be paid for (loan, cash, etc.) It also contains details such as appraisals, conditions of purchase, etc. Utah law requires licensed Real Estate agents to use the REPC form, although the home buyer and home seller can agree to alter or delete its provisions, or to use a different form.

The Sellers Disclosure

The Sellers Disclosure is a document that lists in detail any issues with a home. In the state of Utah, a seller is required by law to disclose material defects and latent defects. Material defects are things you can easily see or find. Latent defects are not easily seen or not obviously apparent.

The Title Document is a list of all previous owners of the home and any liens or other clouds on the title. You’ll need to pay off any additional/existing liens in order to have a free and clear title. It’s important to review this document to prevent delays in the closing process. When you buy a home, you acquire the title, which represents your ownership rights.

The Title Insurance Policy

The Title Insurance Policy is a document that outlines protections for the lender. Hidden title hazards can emerge after purchasing a home, but title insurance can offer protection against them.

The Transfer of Tax Declaration

The Transfer of Tax Declaration is a document that lists the taxes owed for the transfer of the property. Utah does not charge a real estate transfer tax, therefore this is not a concern for Utah homebuyers as it is not a required closing document.

Thanks for Reading!

I hope this article was helpful! Now you’ve seen a quick summary of the closing documents you’ll encounter when buying a home. Also, depending on which state you’re purchasing a home in, there may be more or fewer documents to sign. If you want more details or additional information, then please check out these posts as well!

")

{kind=link}