Understanding 30-Year Fixed-Rate Mortgages in Utah

A 30-year fixed mortgage rate may seem daunting, but it doesn’t always have to be. Many issues can stem from just not fully understanding the process. By breaking it down into easier steps such as advantages, factors influencing fixed rates, and how long your loan should be, you will leave feeling confident in your knowledge of mortgage rates within Utah.

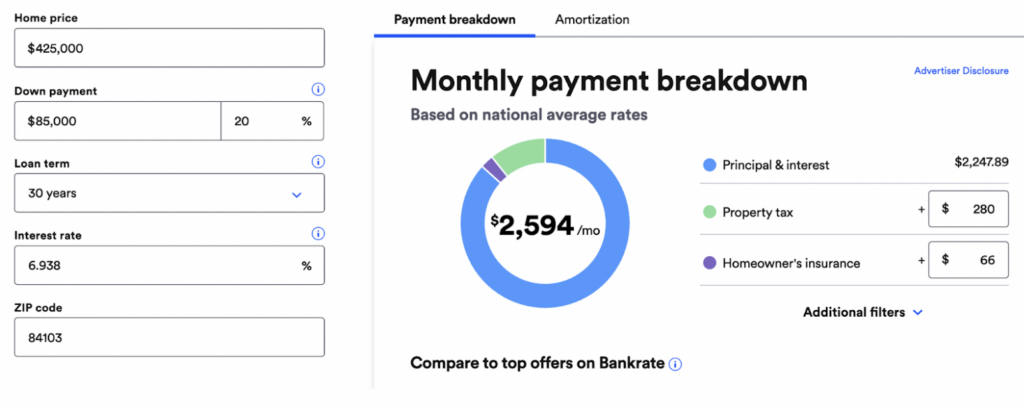

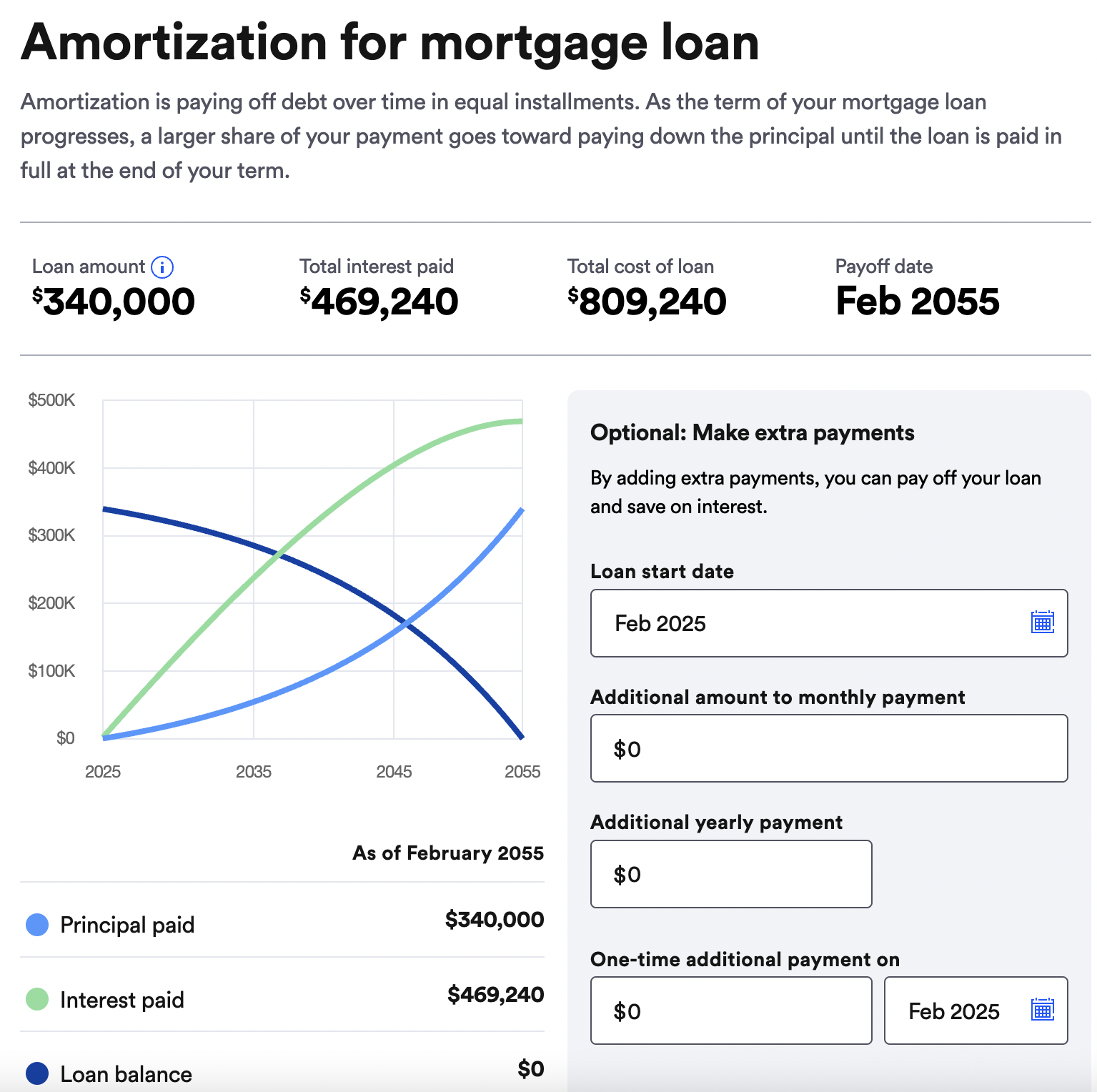

A 30-year fixed-rate mortgage is the most popular loan length allowing homeowners to purchase property by paying the balance over 30 years through fixed interest rates. The loan features predictable monthly payments as payments stay unchanged throughout the loan period. This length choice stands out as the most popular selection for first-time homebuyers as monthly payments are lower than what borrowers would pay with shorter mortgage terms. Residents of Utah frequently choose this type as it helps them purchase homes in an ever-changing market by providing steady payment amounts.

Advantages of a 30-Year Fixed-Rate Mortgage

There are several benefits to a 30-year fixed mortgage rate. Borrowers with mortgage rates such as these benefit from consistent monthly payments that remain lower than those for 15-year mortgage loans. When choosing this payment plan, homeowners can extend their financial resources ultimately leading them to purchase their dream homes, staying far away from compromise. Fixed interest rates also protect borrowers from market rate increases, establishing a constant payment amount for future periods. Because of its stable payment plan, Utah families can more confidently plan their future while living in this constantly evolving housing market.

Factors Influencing 30-Year Mortgage Rates in Utah

A variety of factors affect the rates of 30-year mortgages in Utah. Some significant economic factors that usually play a part can include inflation, employment rates, and the country’s general economic well-being. Monetary policies of the Federal Reserve can also affect mortgage rates indirectly. For instance, when the Federal Reserve raises interest rates, banks are forced to increase the rates at which they borrow money leading to higher costs for consumers. Locally, mortgage rates within Utah are influenced by the market demand for housing and property values as lenders change their interest rates according to market trends.

As of 2025, the 30-year fixed rate mortgage in Utah sits at 6.56%, which is only slightly below the current national average. This is possible due to Utah having a strong economy, with a prosperous and overall healthy housing market to follow. As a result, rates are relatively stable compared to other states. It is predicted that mortgage rates in Utah will stay between 6.0% and 6.9% throughout 2025. For potential homebuyers, any rate changes will be accompanied by changes in their monthly payments and the overall total amount paid toward the loan.

30-Year vs. 15-Year Fixed Rate Mortgages

You may be wondering, why choose a 30-year over a 15-year mortgage? The major disadvantage of a 15-year mortgage is the higher and more frequent monthly payments that accompany it. Alternatively, the main advantage is that homeowners can make fewer payments, overall paying less in interest over the life of the loan. This option is quite popular in Utah for buyers who want to build equity quickly or be mortgage-free as soon as possible. The choice between a 30-year and 15-year mortgage ultimately boils down to the personal financial objectives, income stability, and personal preference of each individual homeowner.

Take-Aways

In conclusion In Utah, many homebuyers prefer a 30-year fixed-rate mortgage as it offers affordability and financial planning advantages. Understanding the advantages and disadvantages of each available option helps individuals select the correct mortgage term for their circumstances. However, It is crucial to make sure to evaluate your own financial goals before making a final decision. Our website https://www.mortgagerateutah.com/ features additional resources about Utah mortgages and current rate information. Additional resources include the Utah Department of Financial Institutions and City Creek Mortgage which can help you discover more detailed and specific loan options.

")

{kind=link}