Mortgage Rates in Utah & How to Apply for a Mortgage

Are you preparing to buy a home, invest in rental property, or finance a renovation in Utah? Understanding the mortgage process is key to securing the best rates and successfully navigating from application to closing. Whether you’re researching how to apply for a mortgage or wondering how to increase your credit score for mortgage approval, this guide covers everything you need to know—including current mortgages rates in Utah today and what to expect from conditional mortgage loan approval.

Getting started with a mortgage begins with a clear understanding of your financial standing. Before applying, gather essential documents like proof of income, credit reports, tax returns, and bank statements. Use a mortgage documents checklist to ensure you’re prepared. To apply, start by researching lenders, filling out an application (either online or in person), and authorizing a credit check. Most lenders will use this information to issue a pre-qualification or pre-approval letter. In Utah, local mortgage brokers can offer insights into specific programs or rate advantages based on your location or buyer status.

If you’re wondering how to get mortgage approval, it all starts with financial readiness. Lenders evaluate your debt-to-income ratio, employment history, credit score, and financial reserves. To improve your chances of approval, pay down existing debt, avoid large purchases before applying, maintain consistent income documentation, and review your credit report for errors.

One of the most impactful steps you can take before applying is boosting your credit score. A higher score can lead to lower interest rates and greater loan options. Here’s how to increase credit score for mortgage success: make all credit card payments on time, keep credit utilization below 30%, avoid opening new credit lines shortly before applying, and dispute any incorrect information on your credit report. If you start early, even a modest improvement in your score can have a significant impact on your mortgage terms.

Conditional Mortgage Loan Approval

After applying, you may receive a conditional mortgage loan approval. This means the lender is willing to finance your loan, provided certain conditions are met—usually additional documentation or verification. This step is crucial because it shows you’re nearing full approval, but you’re not quite there yet. Typical conditions include proof of homeowners insurance, updated bank statements, and a final appraisal of the property. Meeting these conditions promptly keeps the process moving smoothly toward closing.

To stay organized during the mortgage process, use a mortgage documents checklist. Common items include a government-issued ID, Social Security number, W-2s and/or 1099s for the last two years, recent pay stubs, bank statements for two to three months, tax returns for two years, proof of additional income if applicable, debt and liability documentation such as student loans and auto loans, and rental history or mortgage payment history if applicable. Having these documents ready will expedite both the pre-approval and final approval processes.

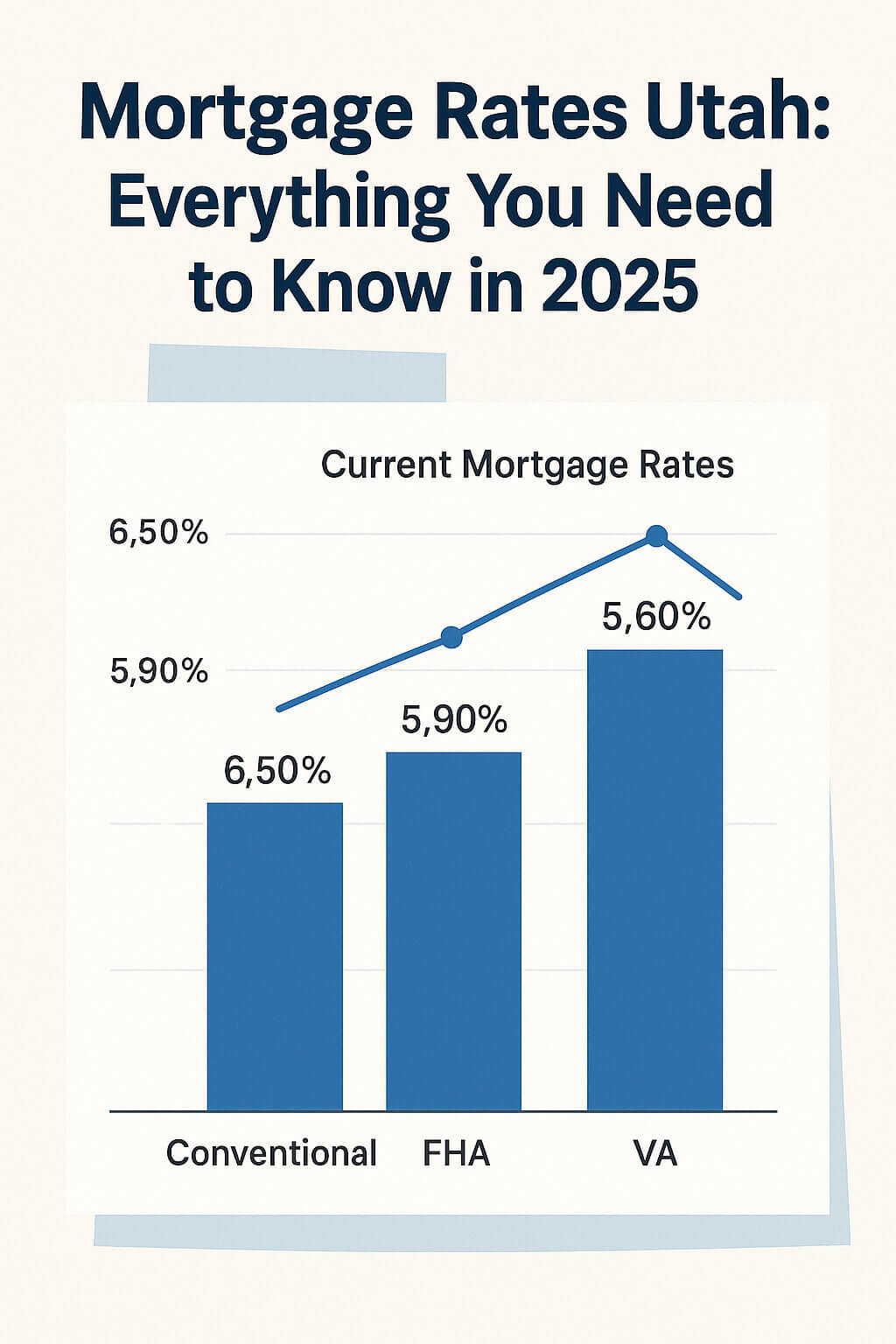

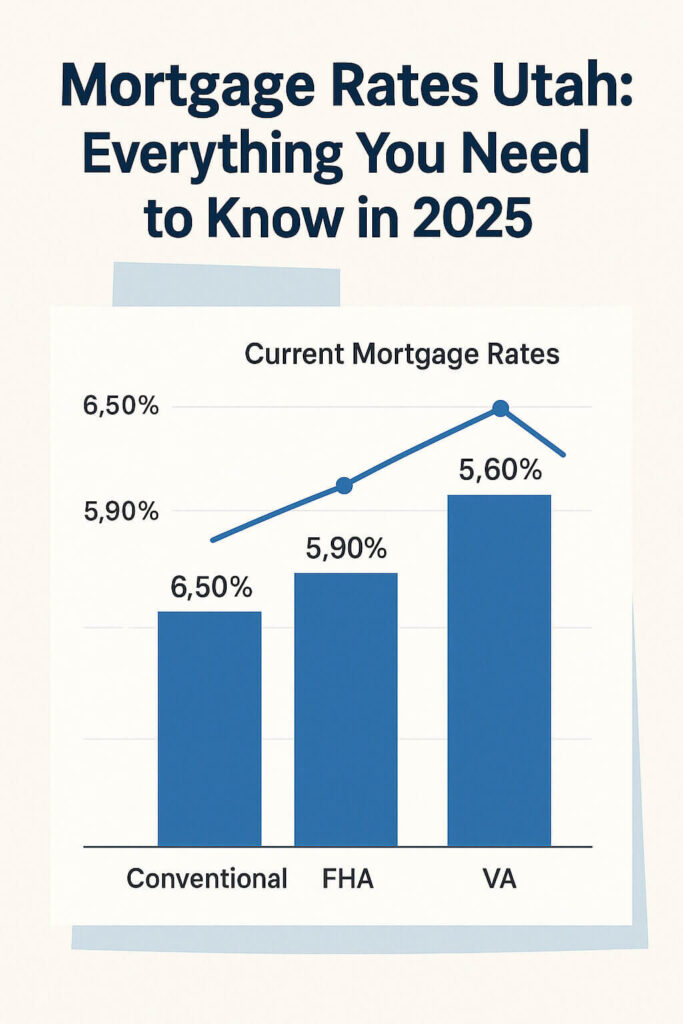

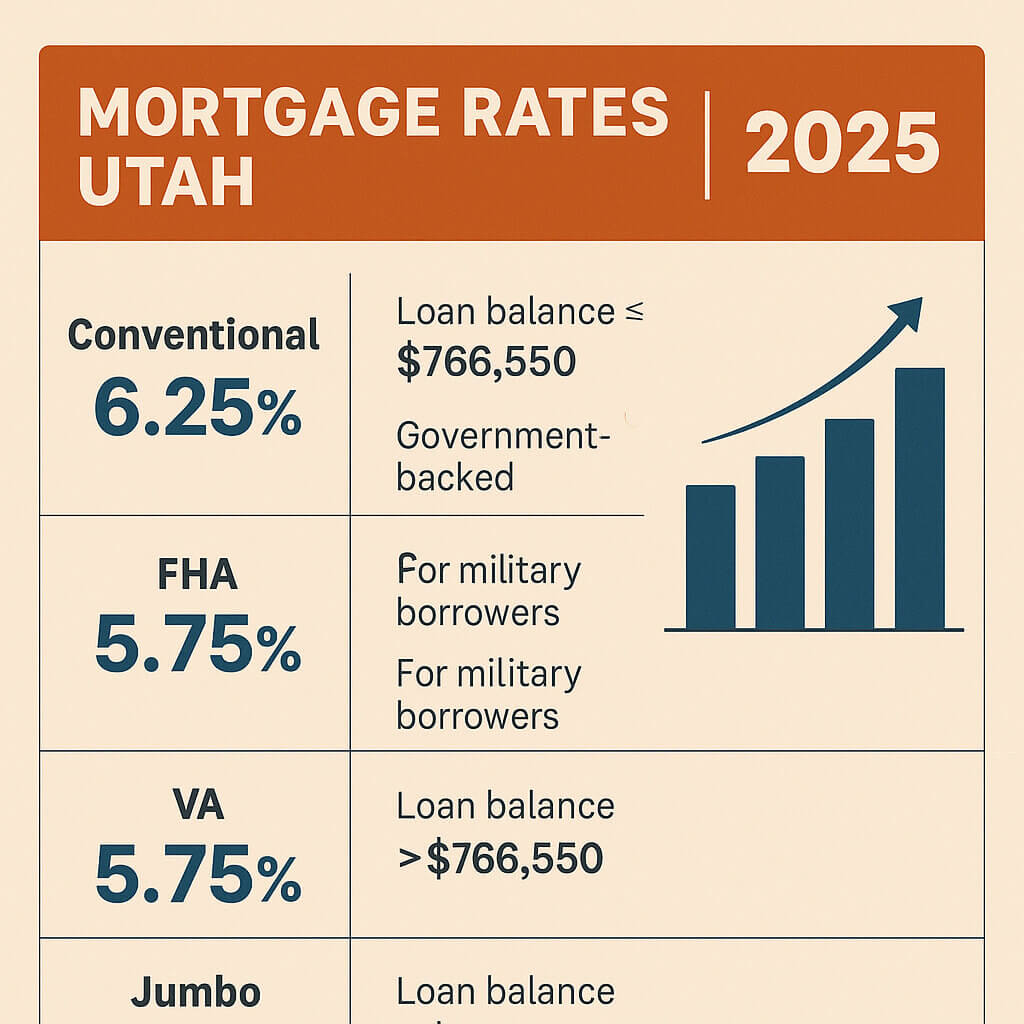

Compare Mortgage Rates in Utah

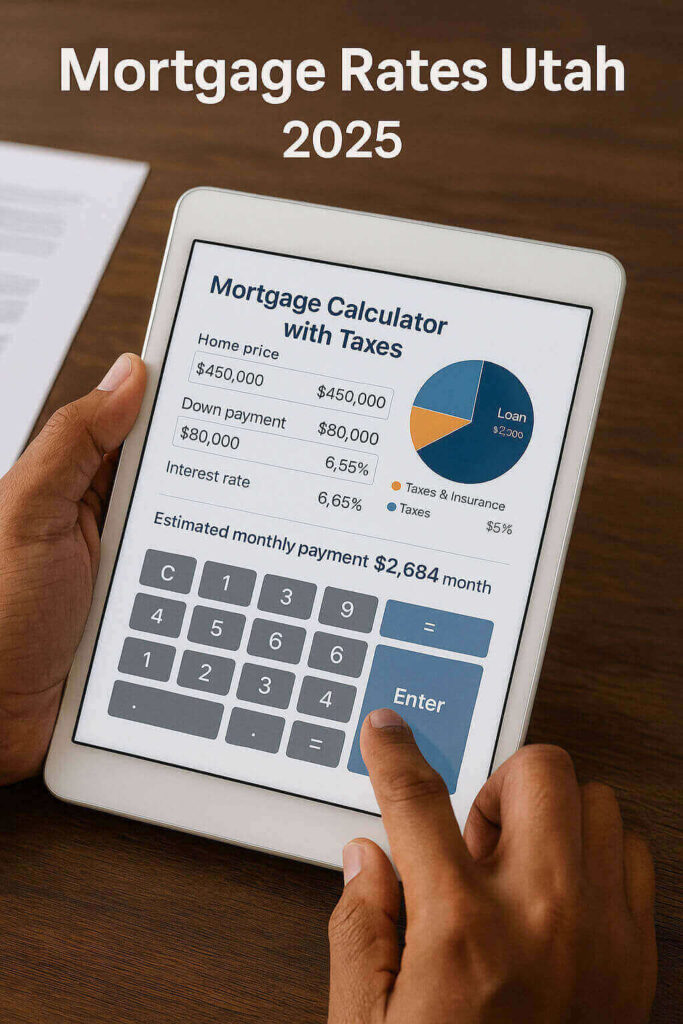

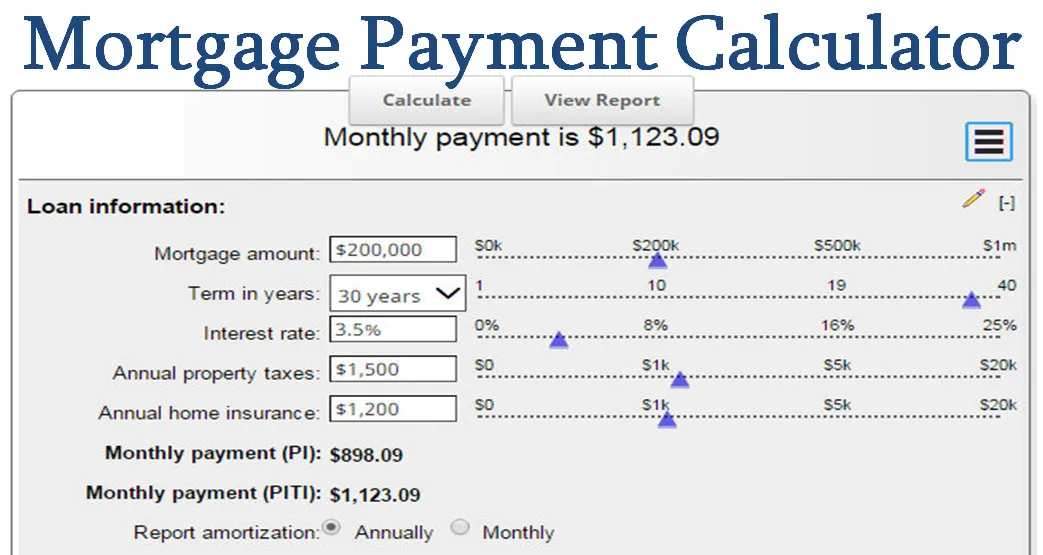

Shopping around is crucial. Interest rates vary by lender, and even a small difference can affect your monthly payment. To compare mortgage rates, use online tools or consult with local lenders in Utah. Ask about fixed versus adjustable rates, loan term options such as 15 versus 30 years, rate lock periods, and estimated closing costs.

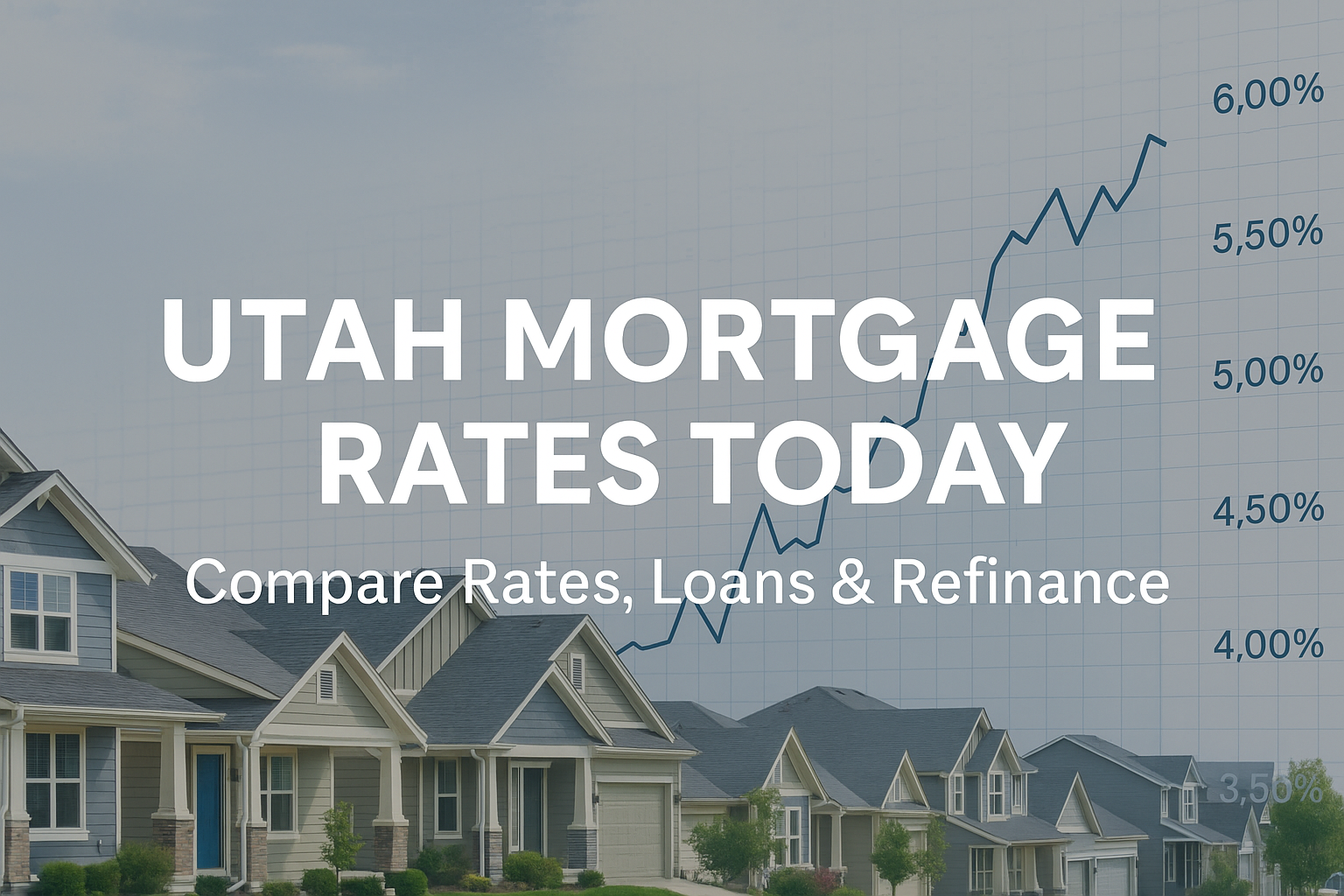

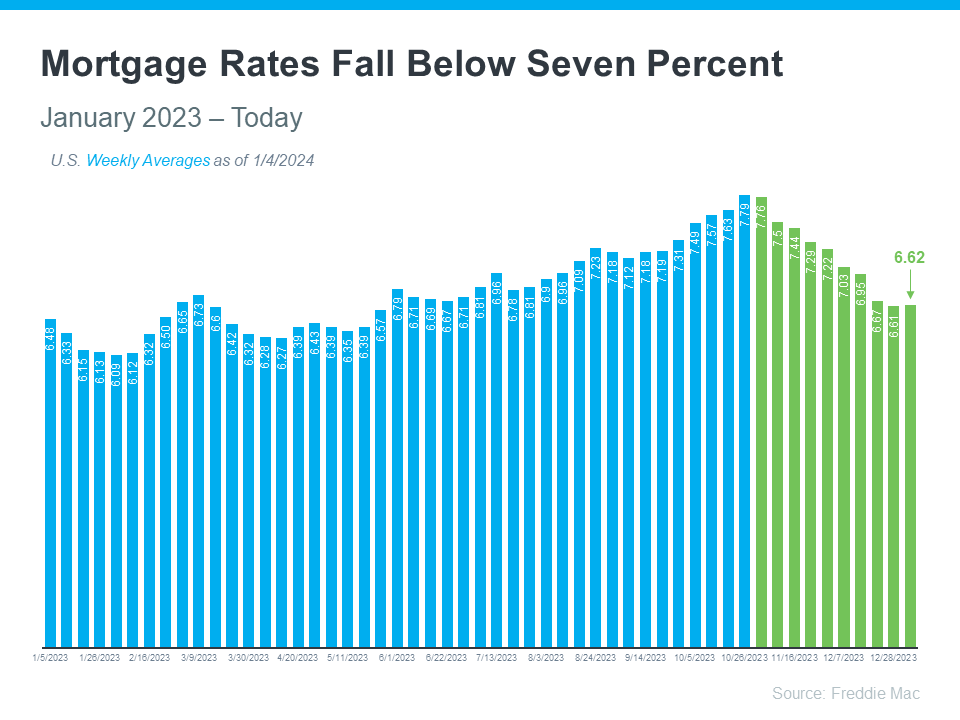

Staying updated on mortgages interest rates today helps you decide when to apply. Rates can fluctuate based on economic trends, Federal Reserve decisions, and housing demand in Utah. As of now, interest rates hover between 6–7% for 30-year fixed mortgages, but exact rates depend on your credit score, down payment, and loan type. Always verify current mortgage interest rates today before locking in your loan.

If you’re looking to renovate your current home, a mortgage for home improvement—such as a cash-out refinance or home equity loan—might be the right solution. These loans allow you to access funds based on your home’s equity, which you can use for repairs, upgrades, or energy-efficient improvements. In Utah, many homeowners use these to add value before resale.

Mortgage Loan for Rental Property

Investing in a rental property? A mortgage loan for rental units typically requires a higher down payment and stricter qualification criteria compared to a primary residence loan. Lenders look for strong credit, solid income, and sometimes even existing landlord experience. Be sure to compare mortgage rates and understand property management responsibilities before moving forward.

Wondering where rates are headed? The mortgage rate forecast for Utah suggests that rates may stabilize or decline slightly in the coming months as inflation cools. However, market volatility makes predictions tricky. If you’re on the fence about locking in a rate, consult with a mortgage advisor to strategize your timing.

Understanding the mortgage process—from how to get mortgage approval to what to expect during conditional mortgage loan approval—can make the difference between a stressful and a smooth homebuying experience. By using tools like a mortgage documents checklist, keeping track of mortgage interest rates today, and improving your credit score, you can secure favorable terms and confidently step into homeownership in Utah.