Buying your first home is one of the biggest financial decisions you will ever make. Naturally, most buyers start by asking: What credit score is required to buy a house for the first time? The good news is that you do not need perfect credit. Whether you are exploring a mortgage with a 580 credit score, a mortgage with a 600 credit score, or a mortgage with a 620 credit score, there are real options available in Utah.

FHA Loan Credit Score Requirements for First-Time Buyers

One of the most popular programs for new buyers is the FHA loan. The official fha loan credit score requirements typically allow scores as low as 580 with a 3.5% down payment. For buyers with slightly stronger credit, comparing an FHA vs conventional loan can help determine which offers better long-term savings. If your credit is stronger — for example, qualifying for mortgage rates for a 700 credit score — you may benefit from lower interest rates and reduced monthly payments. If you are worried about qualifying for a home loan with bad credit or finding the best Mortgage for fair credit, FHA programs often provide the most flexibility. External Resource Example: For national FHA guidelines, see: https://www.hud.gov

How Much House Can I Afford on a 70,000 Salary?

Credit is only part of the equation. Lenders also look at income and debt. Many Utah buyers ask, how much house can I afford on 70000 salary? The answer depends on your debt-to-income ratio. Even if you have a mortgage with a high debt-to-income ratio, you may still qualify depending on compensating factors. Another common question is what income do you need to buy a house? In reality, income requirements vary based on price point, interest rate, and debt obligations. If you are unsure where you stand, learning how to get prequalified for a home loan without affecting your credit can give you clarity before formally applying.

Steps to Get a Mortgage and What to Expect

Understanding the steps to get a mortgage makes the process less stressful.

Prequalification

Application

Underwriting

Appraisal

Closing Many borrowers ask how long mortgage approval takes. In Utah, timelines typically range from 21–30 days, depending on documentation and appraisal speed. You will need several documents for a mortgage, including: ● Pay stubs ● Bank statements ● Tax returns (unless applying for alternative documentation) After approval, buyers often ask what happens after mortgage pre-approval. This is when you begin shopping confidently, submit offers, and lock in your rate once under contract.

Mortgage Options for Self-Employed and Alternative Income Borrowers

If you are self-employed, traditional guidelines may not reflect your true income. A mortgage for self-employed borrowers may allow flexibility. Some borrowers explore bank statement loan requirements instead of tax returns. In certain situations, a mortgage without tax returns may be available. If purchasing a condo, understanding condo mortgage requirements is also essential, as the HOA approval and project eligibility can impact financing.

Choosing the Best Mortgage Lenders for First Time Buyers

Not all lenders are equal. Many buyers research the best mortgage lenders for the first time buyers, compare the best mortgage companies, and evaluate the best mortgage lenders overall. Working with a local Utah expert provides advantages: ● Faster communication ● Knowledge of local appraisal trends ● Personalized rate strategy ● Guidance on fixed vs adjustable rate mortgage decisions Internal Link Example: Learn more about Utah loan programs here: https://www.mortgagerateutah.com/loan-programs

When Is the Best Time to Refinance?

Even after purchasing, many homeowners later evaluate the best time to refinance to reduce their rate, eliminate mortgage insurance, or change loan terms.

Final Thoughts

Understanding the credit score to buy a house first time is just the beginning. Whether you qualify for a mortgage with a 580 credit score or are optimizing for mortgage rates for 700 credit score, the key is working with a knowledgeable local lender. If you are ready to explore your options, get prequalified today and discover how affordable homeownership in Utah can be.

If you’re thinking about buying a home in Utah, one of the smartest first steps you can take is using a mortgage calculator. A mortgage calculator Utah buyers rely on lets you plug in your loan amount, interest rate, and down payment to get a realistic picture of what your monthly payments might look like — before you ever set foot in a lender’s office. Understanding mortgage rates today makes those estimates even more accurate and helps you plan with confidence.

One of the most common questions among first-time buyers is, “How much home can I afford in Utah?” The answer depends on more than just your income. When you combine a mortgage calculator with a mortgage pre-approval, you get a much clearer financial picture. Lenders will look at your income, your debt-to-income ratio, and your credit history before issuing a pre-approval letter, and knowing those numbers ahead of time puts you in a stronger position from the start.

When running your numbers, make sure your calculations go beyond just the principal and interest. Mortgage closing costs in Utah, property taxes, homeowner’s insurance, and PMI — if your down payment is less than 20% — can all add meaningfully to your monthly expenses. For buyers exploring programs like FHA loans, Utah’s requirements may allow for a lower down payment, which will shift those estimates and open up options that might otherwise seem out of reach.

The type of loan you choose also plays a major role in what you’ll pay each month. A 30-year fixed mortgage gives you the stability of a consistent payment over the life of the loan. VA loan rates in Utah can offer significant savings for eligible veterans and service members. And for buyers looking outside of major metro areas, USDA loan eligibility in Utah can make rural homeownership much more accessible.

Using a mortgage calculator before you apply for a loan isn’t just a helpful exercise — it’s a way to avoid surprises during underwriting and walk into the process knowing exactly what you’re working with.

For borrowers with a 700 credit score, mortgage qualification becomes significantly more favorable compared to lower credit tiers. While a 700 score is generally considered “good,” approval still depends on more than just credit. Lenders evaluate income stability, debt obligations, employment history, and overall financial risk before determining how much mortgage you can qualify for.

Understanding how a mortgage with 700 credit score is evaluated helps borrowers prepare beyond simply checking their credit report.

What Does a 700 Credit Score Mean for Mortgage Approval?

A mortgage with 700 credit score typically qualifies borrowers for conventional loan programs with competitive interest rates. Compared to lower credit ranges, a 700 score often results in:

More favorable interest rates

Lower private mortgage insurance (PMI) costs

Stronger approval likelihood

Greater flexibility in down payment requirements

However, lenders still calculate your debt to income ratio for mortgage approval to ensure total monthly obligations remain within acceptable limits. A strong credit score improves eligibility, but excessive debt can reduce approval amounts.

This reinforces an important principle: credit score alone does not determine approval. Overall financial stability carries equal weight in the underwriting process.

Income and Debt Still Determine How Much You Can Qualify For

Even with solid credit, lenders analyze:

Gross monthly income

Total recurring debts

Employment consistency

Minimum income for mortgage approval standards

Your overall debt-to-income ratio

Borrowers often use tools like a mortgage calculator with down payment or a 30 year fixed mortgage calculator to estimate monthly obligations before formally applying. These tools provide a realistic payment expectation but do not replace full lender evaluation.

Ultimately, how much mortgage you can qualify for depends on the relationship between income, debt, and long-term repayment capacity.

Down Payment Strategy and Loan Structure

Down payment size also influences approval and loan terms. A larger down payment can:

Reduce monthly payment obligations

Lower PMI requirements

Strengthen underwriting confidence

Improve long-term affordability

First-time buyers may compare options using a mortgage calculator first time buyer bad credit tool to understand how interest rates shift across different credit brackets.

Even with a 700 score, optimizing down payment strategy can improve loan performance and financial flexibility.

What Else Affects Mortgage Affordability?

Beyond credit score, lenders consider:

Length of credit history

Recent credit activity

Existing loan balances

Stability of employment

Overall financial behavior

These factors collectively determine approval risk and influence final loan structure. Understanding what affects mortgage affordability allows borrowers with a 700 credit score to strengthen weak areas before applying.

Final Thoughts

A mortgage with 700 credit score provides access to strong lending opportunities, but it represents only one component of mortgage qualification. Income consistency, debt management, down payment size, and loan selection all influence final approval outcomes.

Borrowers who evaluate their full financial profile instead of relying solely on credit score position themselves for stronger long term affordability and sustainable homeownership.

Utah Mortgage Rates Today If you are searching for the best mortgage rates in Utah, it is important to understand how Utah mortgage rates today are determined. Rates change daily based on market conditions, credit score, loan type, and down payment amount. The 30 year fixed mortgage rates Utah option remains the most popular choice because it offers stable monthly payments and long-term predictability. When comparing offers, borrowers should also review mortgage closing costs Utah in addition to the interest rate. First Time Home Buyer Mortgage Utah Programs Utah offers several programs designed to help first-time buyers enter the market. A first time home buyer mortgage Utah program may include down payment assistance or flexible credit guidelines. Getting mortgage pre approval Utah early in the process helps buyers understand how much home can I afford Utah before making an offer. Sellers are also more likely to accept offers from pre-approved buyers. FHA, VA, and USDA Loan Options Government-backed loans provide flexible alternatives: FHA loan Utah requirements allow lower credit scores and smaller down payments. VA loan rates Utah offer competitive terms for eligible veterans and active military. USDA loan Utah eligibility supports buyers purchasing homes in qualified rural areas. Each option has unique qualification standards, so comparing lenders is important. HELOC Requirements and Home Equity Options Homeowners looking to access equity should understand HELOC requirements before applying. A home equity line of credit vs home equity loan comparison helps determine which option fits long-term financial goals. HELOC rates Utah and repayment structures vary by lender, so borrowers should review terms carefully.

Buying a home starts with one essential question: how much mortgage can I afford? While many buyers begin with a mortgage calculator with taxes and PMI or a mortgage calculator with down payment, lenders evaluate so much more than a simple monthly payment estimate. Income, debt obligations, credit score, and loan structure all determine your final approval amount.

Understanding the difference between how much mortgage can I get approved for and how much mortgage can I qualify for is critical. Approval depends on verified income, employment stability, credit history, and your debt-to-income ratio for mortgage approval.

Income-Based Mortgage Affordability

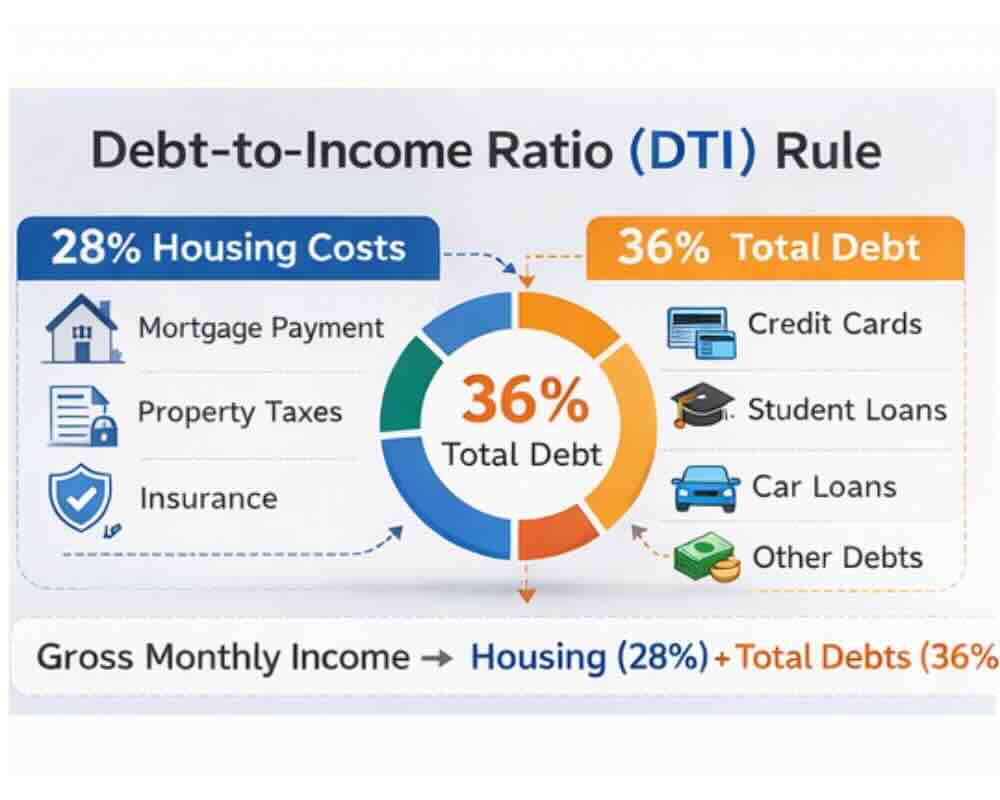

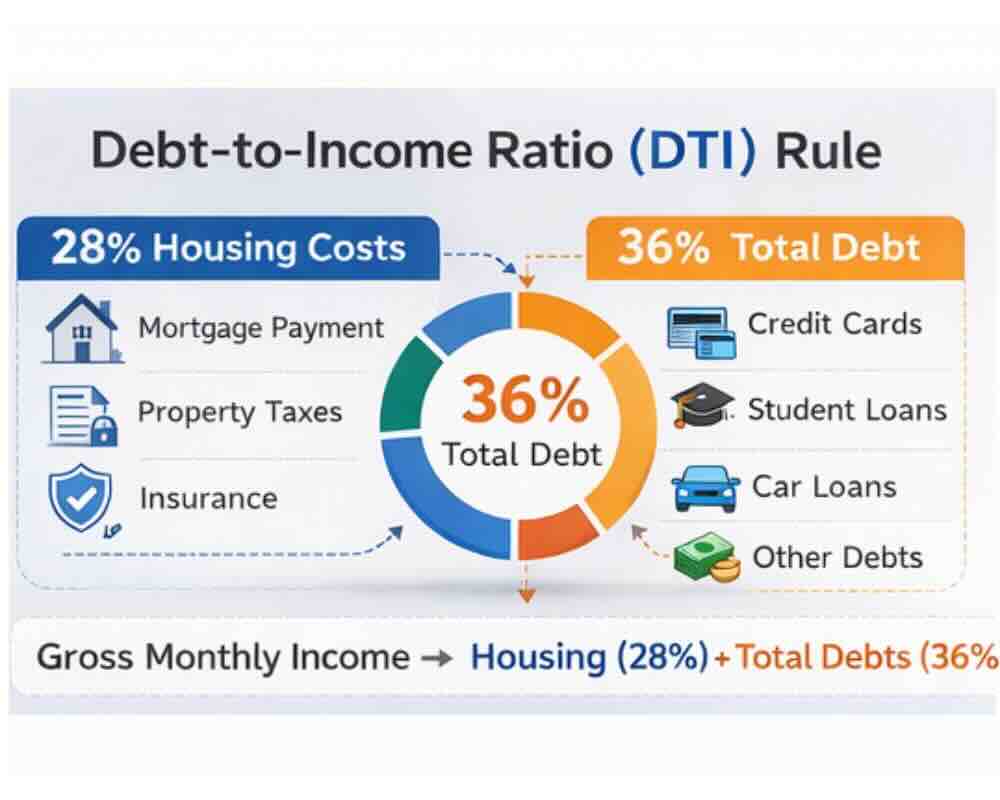

If you earn $65,000 annually, you may ask how much mortgage can I afford with 65k salary. Lenders often use the 28/36 rule, meaning no more than 28% of gross income should go toward housing and no more than 36% toward total debts.

For borrowers researching how much house can I afford 50k income, the same percentage guidelines apply, but the resulting maximum mortgage amount based on income will be lower.

Student loan debt also impacts affordability. Many buyers wonder how much house can I afford with student loans, since lenders calculate overall obligations using a mortgage affordability calculator debt to income ratio model. Some borrowers also prefer calculating conservatively and ask how much mortgage can I afford after taxes to ensure their budget remains comfortable.

Approval vs. Qualification Requirements

Lenders may require a certain minimum income for mortgage approval, but consistency of earnings often matters more than the raw number. If you are self-employed, a mortgage calculator for self-employed borrowers can help estimate potential affordability.

Those with commissions or fluctuating pay must understand how to calculate variable income for mortgage qualification. Most lenders review two years of income history to determine a stable average.

Credit Score and First-Time Buyer Considerations

Your credit profile significantly influences affordability. Securing a mortgage with 700 credit score generally provides access to competitive interest rates and better loan terms.

However, first-time buyers exploring a mortgage calculator first time buyer bad credit may see higher estimated payments due to increased risk. Lower-income households may also use a low-income mortgage calculator to determine realistic price ranges before beginning the application process.

Understanding the Full Monthly Payment

Many buyers only focus on principal and interest, but a realistic estimate requires more detail. Tools such as a mortgage calculator with insurance, mortgage calculator with HOA fees, and mortgage calculator including closing costs provide a clearer picture of total expenses.

A mortgage payment breakdown calculator separates principal, interest, taxes, insurance, and PMI. If purchasing with a partner, a dual income home loan calculator can demonstrate how combined earnings increase borrowing power.

Comparing options with a 30-year fixed mortgage calculator helps buyers understand long-term payment stability and total interest costs.

Ultimately, understanding what affects mortgage affordability ensures that you choose a loan that fits your financial goals rather than stretching to the maximum lender approval.

Mortgage Rates for 700 Credit Score in Utah | 2026 Home Buyer Guide

Navigating Current Mortgage Interest Rates in Utah: A 2026 Buyer’s Guide

In the ever-evolving Utah real estate landscape, securing a home requires more than just finding the perfect property in Salt Lake City or St. George; it requires a masterful understanding of the financial climate. As of early 2026, current mortgage interest rates in Utah have reached a point of relative stability, sitting at approximately 6.24% for a 30-year fixed term. For Utahns looking to enter the market, the difference between an average deal and the best mortgage rates available often comes down to the timing of your application and the specific lender you choose. While national headlines provide a broad overview, the local market demands a more nuanced approach to everything from conventional mortgage rates to state-specific assistance programs.

Current 30 Year Mortgage Rates and the Utah Market

Current 30 year mortgage rates serve as the primary benchmark for most buyers, and understanding their trajectory is essential for long-term planning. While these rates are influenced by national bond markets, local competition among credit union mortgage rates often provides Utah residents with unique opportunities to beat the national average. When you begin your search, looking at today’s mortgage rates is only the first step. To truly understand your purchasing power, you must utilize a mortgage payment calculator to factor in Utah’s specific property tax rates and homeowners’ insurance costs. Because mortgage interest rates today can fluctuate based on daily economic reports, staying in close contact with local mortgage lenders who understand the Wasatch Front’s inventory is a significant advantage.

Mortgage Rates for 700 Credit Score Borrowers

Mortgage rates for 700 credit score profiles represent a critical “middle ground” in the 2026 lending environment. While those searching for mortgage rates for excellent credit (typically 760 or higher) will see the lowest advertised figures, a 700 score still opens doors to highly competitive conventional mortgage rates. If you fall into this credit tier, it is vital to use a mortgage affordability calculator to see how a slight shift in interest could affect your maximum loan amount. Borrowers in this range should also investigate mortgage rates with no points, as paying “discount points” upfront might not always be the most cost-effective move if you plan to sell or move within five to seven years. For those just under this threshold, a home loan calculator can demonstrate how much monthly savings you could achieve by boosting your score just 20 points before locking in your rate.

Best Mortgage Lenders for First-Time Buyers in Utah

The best mortgage lenders are often defined by their ability to pair a low rate with specialized programs for those just starting out. For many, the search for a first home buyer loan leads to a choice between large online mortgage lenders and community-based institutions. While online platforms offer speed, local mortgage lenders are often more adept at integrating low down payment mortgage rates with Utah-specific grants, such as those offered by the Utah Housing Corporation. If you are a first-time buyer, comparing mortgage rates for first time buyers across different institutions is essential. You may find that credit union mortgage rates offer lower fees, while a national bank might provide a more robust mortgage refinance path for the future.

Current Refinance Rates and Home Equity Strategies

Current refinance rates have recently become a hot topic for Utahns over the last few years. When monitoring refinance mortgage rates today, the goal is typically to find a “break-even” point. When looking for mortgage lenders near me to handle a refinance, look at mortgage rates by credit score. This way, you can see if your improved financial standing now qualifies you for a “prime” tier. It’s also important to watch out for current refinance rates to ensure you don’t miss the opportunity to optimize your household expenses. By using a home loan calculator to test various scenarios and researching mortgage rates for a 700 credit score versus higher tiers, you take control. Utah remains a high-demand state. However, with the right data and a clear understanding of current mortgage interest rates, your dreams are well within reach.

Refinancing can be a smart move when mortgage refinance rates today are lower than what you currently pay, or when you want to change your loan structure to better fit your goals. The key is making the decision with real numbers, not vibes—and that means understanding rates, costs, and how long it takes to “break even.”

If you’re trying to refinance my mortgage because your payment feels too high, you want to shorten your term, or you’re looking to pull equity out, this guide will walk you through the process in a simple way and show you how to compare lenders, calculators, and programs.

Most people start by checking current refinance rates and then running the math. That’s exactly what we’ll do here—step by step—so you can confidently decide whether to refinance my home loan now or hold off.

On-Page SEO Template Fields

Primary Focus Keyword: mortgage refinance rates today Secondary Keywords (to include in-body): current refinance rates, current refinance mortgage rates, refi rates today, house refinance rates, current refinance mortgage rates, best refinance mortgage rates, lowest refinance rates, best refinance companies, best refinance lenders, no closing cost refinance, refinance investment property, refinance my mortgage, refinance my home loan, refinance home loan rates, refinance home loan calculator, refinance home loan rates, refinance mortgage calculator, refinance mortgage rates calculator, refi mortgage calculator, refinance mortgage calculator, refinance house calculator, refinance mortgage calculator, cash out refinance calculator, cash out refinance rates, fha cash out refinance, va refinance rates, va cash out refinance Suggested URL Slug: /mortgage-refinance-rates-today-guide Meta Title: Mortgage Refinance Rates Today: Rates, Calculators, and Best Refinance Lenders Meta Description: Learn how to compare mortgage refinance rates today, use refinance calculators, explore cash-out options (FHA/VA), and choose the best refinance companies for your goals. Estimated Word Count: 900+

Current Refinance Rates: What They Mean and How to Compare Them

Current refinance rates change daily, so it helps to zoom out and compare multiple lender quotes on the same day. When people search refi rates today, they’re usually trying to answer one question: “Is today a good day to lock?”

You’ll see lenders advertise different flavors of the same idea—current refinance mortgage rates, house refinance rates, and even “best” or “lowest” offers. In reality, the lowest refinance rates often assume top-tier credit, strong income, and a clean loan profile. Your rate depends on your credit score, loan-to-value, debt-to-income ratio, and whether you’re refinancing a primary home or planning a refinance investment property loan.

To compare accurately, request quotes that include both the interest rate and APR, and ask what points or lender fees are baked into the offer. That’s how you’ll know whether you’re actually seeing best refinance mortgage rates or just a marketing headline.

Refinance Mortgage Calculator: The Fastest Way to Know If It’s Worth It

A refinance mortgage calculator is where clarity happens. Before you spend time gathering documents or calling lenders, run a few scenarios so you know what you’re aiming for.

A good refinance mortgage calculator (or refinance mortgage rates calculator) helps you estimate your new monthly payment, total interest over the life of the loan, and how long it takes to recover closing costs. You can also use a refi mortgage calculator if you want a quick side-by-side comparison between your current loan and a proposed refinance.

If you prefer more specific tools, you can also use a refinance home loan calculator when you’re comparing terms for a standard mortgage refinance, or a refinance house calculator if you want a simpler, homeowner-friendly layout. The best approach is to run the numbers at least three ways: conservative, realistic, and best-case.

Once you have the calculator output, you’ll be able to make a clean decision: refinance for payment relief, refinance to reduce long-term interest, or don’t refinance at all.

Cash Out Refinance Calculator: How to Tap Equity Without Guessing

If you want to convert home equity into cash, a cash out refinance calculator is your best starting point. It shows how much you might be able to access after paying off your current loan balance (and factoring in loan-to-value limits).

After you estimate your cash-out amount, compare cash out refinance rates with standard refinance rates. Cash-out loans can sometimes come with slightly higher pricing because the lender is taking on more risk.

Two common cash-out paths are fha cash out refinance and va cash out refinance. FHA options can be useful for borrowers who need more flexible credit guidelines, while VA cash-out programs may offer strong terms for eligible service members and veterans. Either way, the calculator step comes first—because it keeps your expectations realistic and your planning tight.

VA Refinance Rates and FHA Options: Picking the Right Program for Your Situation

VA refinance rates can be very competitive, and VA programs often have borrower-friendly features. If you’re eligible, it’s worth comparing VA quotes against conventional quotes to see which option gives you the best combination of rate and fees.

If you’re looking at an fha cash out refinance, pay close attention to mortgage insurance costs. FHA can open doors, but the insurance premiums can change the “true cost” of the loan. This is where a refinance mortgage rates calculator (and a careful APR comparison) can make the decision obvious.

The goal is not just to refinance—it’s to refinance into the right structure for your financial life.

No Closing Cost Refinance: Convenient, But Not Always Cheaper

A no closing cost refinance can be helpful if you don’t want to pay fees upfront. But “no closing cost” usually means the costs are shifted somewhere else—either rolled into the loan amount or offset by a higher interest rate.

Use a refinance home loan calculator to compare a no-cost option against a standard refinance with fees paid at closing. If you plan to sell or refinance again soon, no-cost can make sense. If you’re staying long-term, paying costs upfront might deliver bigger lifetime savings.

This is one of those decisions where the math beats intuition every time.

Best Refinance Companies: How to Choose and What to Ask

Choosing between the best refinance companies isn’t just about who has the lowest advertised rate. You’re picking a partner to handle underwriting, timelines, documentation, and funding. The best refinance lenders usually win because they’re transparent about fees, fast with communication, and consistent during the closing process.

When comparing lenders, ask:

What are the total lender fees and third-party costs?

How long is the rate lock, and what happens if closing is delayed?

Can you provide a full Loan Estimate?

Do you specialize in my scenario (self-employed, high DTI, refinance investment property, etc.)?

Also compare refinance home loan rates across at least three lenders on the same day. That’s how you’ll see what’s truly competitive in the market and identify which offer actually matches the current refinance mortgage rates environment.

Refinance My Mortgage: A Simple Step-by-Step Plan

If your goal is to refinance my mortgage without wasting time, here’s a simple plan that works:

Check mortgage refinance rates today and confirm the general trend.

Run a refinance mortgage calculator to estimate savings and break-even.

Decide your purpose: lower payment, shorten term, or cash-out.

Collect quotes and compare current refinance rates and fees side-by-side.

Pick your lender, lock the rate, and submit documents quickly.

Review the Loan Estimate and Closing Disclosure carefully before you sign.

If you’re doing this to refinance my home loan for a better monthly payment, focus on break-even time and total costs. If you’re doing it for cash-out, focus on new loan balance and long-term affordability.

Quick Wrap-Up: What to Do Next

Refinancing gets easier when you treat it like a decision system: rates → calculator → quotes → program fit → lender choice. Start with refi rates today, confirm the current refinance rates trend, and then use the right tools—whether that’s a refi mortgage calculator, refinance mortgage rates calculator, or a cash out refinance calculator—to make the outcome predictable.

If you want, paste your focus website URL and I’ll tailor this exact post to match the site’s tone, add an FAQ section for featured snippets, and tighten keyword placement even further while keeping the flow natural.

[IMAGE PLACEMENT NOTE — Hero Image] Image Title: Mortgage Refinance Rates Today Hero File Name: mortgage-refinance-rates-today-hero-v4.jpg Where it goes: Directly under this H1 title at the top of the blog post Alt text (description only): “Mortgage refinance rates today hero image showing homeowners reviewing refinance options with a home and rate visuals in the background.”

Refinancing can be a smart move when mortgage refinance rates today are lower than what you currently pay, or when you want to change your loan structure to better fit your goals. The key is making the decision with real numbers—not vibes—and that means understanding rates, costs, and how long it takes to “break even.”

If you’re trying to refinance my mortgage because your payment feels too high, you want to shorten your term, or you’re looking to pull equity out, this guide will walk you through the process in a simple way and show you how to compare lenders, calculators, and programs.

Most people start by checking current refinance rates and then running the math. That’s exactly what we’ll do here—step by step—so you can confidently decide whether to refinance my home loan now or hold off.

Current Refinance Rates: What They Mean and How to Compare Them

Current refinance rates change daily, so it helps to zoom out and compare multiple lender quotes on the same day. When people search refi rates today, they’re usually trying to answer one question: “Is today a good day to lock?”

You’ll see lenders advertise different versions of the same idea—current refinance mortgage rates, house refinance rates, and even “best” or “lowest” offers. In reality, the lowest refinance rates often assume top-tier credit, strong income, and a clean loan profile. Your rate depends on your credit score, loan-to-value, debt-to-income ratio, and whether you’re refinancing a primary home or planning a refinance investment property loan.

To compare accurately, request quotes that include both the interest rate and APR, and ask what points or lender fees are baked into the offer. That’s how you’ll know whether you’re actually seeing best refinance mortgage rates or just a marketing headline.

Refinance Mortgage Calculator: The Fastest Way to Know If It’s Worth It

[IMAGE PLACEMENT NOTE — Calculator Image] Image Title: Refinance Mortgage Calculator Guide File Name: refinance-mortgage-calculator-guide-v4.jpg Where it goes: Directly under this H2 section title Alt text (description only): “Refinance mortgage calculator guide showing a break-even timeline, monthly payment comparison, and estimated refinance savings.”

A refinance mortgage calculator is where clarity happens. Before you spend time gathering documents or calling lenders, run a few scenarios so you know what you’re aiming for.

A good refinance mortgage calculator (or refinance mortgage rates calculator) helps you estimate your new monthly payment, total interest over the life of the loan, and how long it takes to recover closing costs. You can also use a refi mortgage calculator if you want a quick side-by-side comparison between your current loan and a proposed refinance.

If you prefer more specific tools, you can also use a refinance home loan calculator when you’re comparing terms for a standard mortgage refinance, or a refinance house calculator if you want a simpler, homeowner-friendly layout. The best approach is to run the numbers at least three ways: conservative, realistic, and best-case.

Once you have the calculator output, you’ll be able to make a clean decision: refinance for payment relief, refinance to reduce long-term interest, or don’t refinance at all.

Cash Out Refinance Calculator: How to Tap Equity Without Guessing

[IMAGE PLACEMENT NOTE — Cash-Out Image] Image Title: Cash Out Refinance Calculator File Name: cash-out-refinance-calculator-v4.jpg Where it goes: Directly under this H2 section title Alt text (description only): “Cash out refinance calculator visual showing home equity access, cash-out amount, and refinance options including FHA cash out refinance and VA cash out refinance.”

If you want to convert home equity into cash, a cash out refinance calculator is your best starting point. It shows how much you might be able to access after paying off your current loan balance (and factoring in loan-to-value limits).

After you estimate your cash-out amount, compare cash out refinance rates with standard refinance rates. Cash-out loans can sometimes come with slightly higher pricing because the lender is taking on more risk.

Two common cash-out paths are fha cash out refinance and va cash out refinance. FHA options can be useful for borrowers who need more flexible credit guidelines, while VA cash-out programs may offer strong terms for eligible service members and veterans. Either way, the calculator step comes first—because it keeps your expectations realistic and your planning tight.

VA Refinance Rates and FHA Options: Picking the Right Program for Your Situation

VA refinance rates can be very competitive, and VA programs often have borrower-friendly features. If you’re eligible, it’s worth comparing VA quotes against conventional quotes to see which option gives you the best combination of rate and fees.

If you’re looking at an fha cash out refinance, pay close attention to mortgage insurance costs. FHA can open doors, but the insurance premiums can change the “true cost” of the loan. This is where a refinance mortgage rates calculator (and a careful APR comparison) can make the decision obvious.

The goal is not just to refinance—it’s to refinance into the right structure for your financial life.

No Closing Cost Refinance: Convenient, But Not Always Cheaper

A no closing cost refinance can be helpful if you don’t want to pay fees upfront. But “no closing cost” usually means the costs are shifted somewhere else—either rolled into the loan amount or offset by a higher interest rate.

Use a refinance home loan calculator to compare a no-cost option against a standard refinance with fees paid at closing. If you plan to sell or refinance again soon, no-cost can make sense. If you’re staying long-term, paying costs upfront might deliver bigger lifetime savings.

Best Refinance Companies: How to Choose and What to Ask

Choosing between the best refinance companies isn’t just about who has the lowest advertised rate. You’re picking a partner to handle underwriting, timelines, documentation, and funding. The best refinance lenders usually win because they’re transparent about fees, fast with communication, and consistent during the closing process.

When comparing lenders, ask:

What are the total lender fees and third-party costs?

How long is the rate lock, and what happens if closing is delayed?

Can you provide a full Loan Estimate?

Do you specialize in my scenario (self-employed, high DTI, refinance investment property, etc.)?

Also compare refinance home loan rates across at least three lenders on the same day. That’s how you’ll see what’s truly competitive in the market and identify which offer actually matches the current refinance mortgage rates environment.

Refinance My Mortgage: A Simple Step-by-Step Plan

If your goal is to refinance my mortgage without wasting time, here’s a simple plan that works:

Check mortgage refinance rates today and confirm the general trend.

Run a refinance mortgage calculator to estimate savings and break-even.

Decide your purpose: lower payment, shorten term, or cash-out.

Collect quotes and compare current refinance rates and fees side-by-side.

Pick your lender, lock the rate, and submit documents quickly.

Review the Loan Estimate and Closing Disclosure carefully before you sign.

If you’re doing this to refinance my home loan for a better monthly payment, focus on break-even time and total costs. If you’re doing it for cash-out, focus on new loan balance and long-term affordability.

Saving for a down payment can be one of the biggest hurdles. Fortunately, there are programs offering down payment assistance for first time home buyers in Utah.

These programs may include:

Grants that do not require repayment

Deferred payment second mortgages

Low-interest assistance loans

Combining assistance programs with competitive first time home buyer mortgage Utah options can dramatically reduce upfront costs.

Who Qualifies for Down Payment Assistance in Utah?

Eligibility requirements may vary by program, but most Utah down payment assistance programs consider:

Income limits based on household size

Minimum credit score requirements

Completion of a homebuyer education course

Purchasing a primary residence

Programs are often offered through organizations such as the Utah Housing Corporation and approved lenders statewide.

You can move through the homebuying process with clarity and confidence.

Whether you are comparing the best mortgage lenders Utah, working with a trusted mortgage broker first time home buyer specialist, or calculating affordability with a mortgage affordability calculator, preparation is key.

Your first home in Utah is within reach — and with the right loan program and guidance, homeownership can become a reality sooner than you think.

How to Apply for Down Payment Assistance

To apply, buyers typically work with a participating lender who can determine program eligibility and submit the required documentation. Many assistance programs are combined with FHA or conventional loans, allowing buyers to reduce upfront costs while securing competitive mortgage terms.

Buying your first home is an exciting milestone, but understanding your financing options can feel overwhelming. If you are researching first time home buyer mortgage Utah options, exploring loan requirements, or comparing interest rates, this guide will walk you through everything you need to know. From qualification steps to down payment assistance, we’ll cover the essential details to help you move forward confidently.

Current Mortgage Rates Utah for First-Time Buyers

Before choosing a loan, most buyers begin by checking current mortgage rates Utah lenders are offering. Rates directly impact your monthly payment and long-term affordability. You may also see rates referred to as home loan rates Utah, which include conventional, FHA, and other loan types.

For new buyers, understanding first time home buyer Utah interest rates is especially important because certain programs may offer more flexible terms. Rates are influenced by:

Credit score

Debt-to-income ratio

Down payment amount

Loan type

Using a mortgage affordability calculator or a first time home buyer Utah mortgage calculator can help estimate payments based on today’s market conditions.

First Time Home Buyer Programs Utah and Loan Requirements

Many buyers are unaware of the variety of first time home buyer programs Utah offers. These programs are designed to make homeownership more accessible by reducing upfront costs and easing qualification standards.

Understanding first time home owners loan requirements is critical before applying. In most cases, Utah first time home buyer loan requirements include:

Stable employment history

Acceptable credit score

Manageable debt-to-income ratio

Minimum down payment

If you are wondering how to qualify for a mortgage in Utah as a first time buyer, improving your credit, reducing debt, and saving consistently can strengthen your application.

Many first-time buyers choose FHA financing because FHA loan requirements are often more flexible than conventional loans.

FHA Loan Utah First Time Buyer Options

An FHA loan Utah first time buyer program is one of the most popular financing options for new homeowners. FHA loans are attractive because they offer lower minimum credit score thresholds and reduced upfront costs.

The FHA loan down payment can be as low as 3.5%, making it a practical solution for buyers without large savings. However, borrowers must also meet Utah FHA loan income requirements, which consider overall financial stability and debt levels.

For many buyers comparing best mortgage companies for first time buyers, FHA options are a major factor in the decision-making process.

How Much Mortgage Can I Qualify For?

A common question among new buyers is: how much mortgage can I qualify for?

Lenders evaluate income, credit history, monthly debts, and projected expenses. Using a first time home owners loan calculator can help you understand potential payments before formally applying.

If credit concerns are holding you back, you may be searching for how to get pre approved for a loan with bad credit. FHA loans and certain lenders may provide alternative pathways for buyers who are rebuilding credit.

Understanding your purchasing power early in the process helps you shop confidently within your budget.

Mortgage Preapproval Process Utah Explained

The mortgage preapproval process Utah buyers complete is an essential first step before house hunting.

Here’s how it typically works:

Submit income documentation

Provide authorization for credit review

Review debt and employment history

Receive a preapproval letter

Many buyers ask how to get pre approved for a home loan first time buyer without feeling overwhelmed. Working with an experienced mortgage broker first time home buyer specialist can simplify the process.

A knowledgeable mortgage broker salt lake city professional may also help compare multiple lenders to secure competitive terms.

Best Mortgage Lenders Utah for First-Time Buyers

Choosing the right lender can significantly impact your experience. If you are researching the best mortgage lenders Utah offers, consider factors such as:

Loan program variety

Rate transparency

Customer service

First-time buyer support

Some buyers prefer to search for the best mortgage broker in Utah for first time buyers to receive personalized guidance. Brokers often help compare options from different institutions, increasing flexibility.

You may also explore companies labeled as the best mortgage companies for first time buyers, especially those that specialize in educational resources and program guidance.