Buying your first home is an exciting milestone, but understanding your financing options can feel overwhelming. If you are researching first time home buyer mortgage Utah options, exploring loan requirements, or comparing interest rates, this guide will walk you through everything you need to know. From qualification steps to down payment assistance, we’ll cover the essential details to help you move forward confidently.

Current Mortgage Rates Utah for First-Time Buyers

Before choosing a loan, most buyers begin by checking current mortgage rates Utah lenders are offering. Rates directly impact your monthly payment and long-term affordability. You may also see rates referred to as home loan rates Utah, which include conventional, FHA, and other loan types.

For new buyers, understanding first time home buyer Utah interest rates is especially important because certain programs may offer more flexible terms. Rates are influenced by:

- Credit score

- Debt-to-income ratio

- Down payment amount

- Loan type

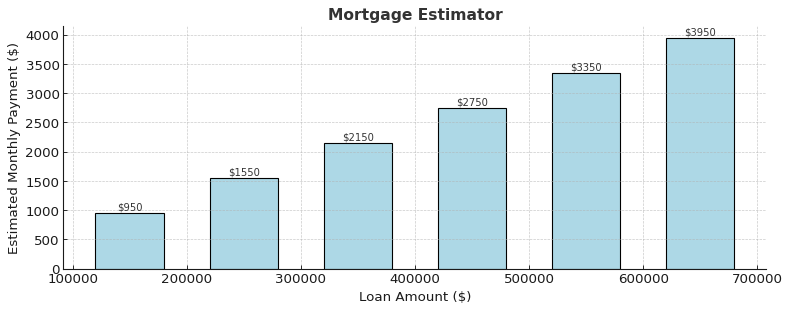

Using a mortgage affordability calculator or a first time home buyer Utah mortgage calculator can help estimate payments based on today’s market conditions.

First Time Home Buyer Programs Utah and Loan Requirements

Many buyers are unaware of the variety of first time home buyer programs Utah offers. These programs are designed to make homeownership more accessible by reducing upfront costs and easing qualification standards.

Understanding first time home owners loan requirements is critical before applying. In most cases, Utah first time home buyer loan requirements include:

- Stable employment history

- Acceptable credit score

- Manageable debt-to-income ratio

- Minimum down payment

If you are wondering how to qualify for a mortgage in Utah as a first time buyer, improving your credit, reducing debt, and saving consistently can strengthen your application.

Many first-time buyers choose FHA financing because FHA loan requirements are often more flexible than conventional loans.

FHA Loan Utah First Time Buyer Options

An FHA loan Utah first time buyer program is one of the most popular financing options for new homeowners. FHA loans are attractive because they offer lower minimum credit score thresholds and reduced upfront costs.

The FHA loan down payment can be as low as 3.5%, making it a practical solution for buyers without large savings. However, borrowers must also meet Utah FHA loan income requirements, which consider overall financial stability and debt levels.

For many buyers comparing best mortgage companies for first time buyers, FHA options are a major factor in the decision-making process.

How Much Mortgage Can I Qualify For?

A common question among new buyers is: how much mortgage can I qualify for?

Lenders evaluate income, credit history, monthly debts, and projected expenses. Using a first time home owners loan calculator can help you understand potential payments before formally applying.

If credit concerns are holding you back, you may be searching for how to get pre approved for a loan with bad credit. FHA loans and certain lenders may provide alternative pathways for buyers who are rebuilding credit.

Understanding your purchasing power early in the process helps you shop confidently within your budget.

Mortgage Preapproval Process Utah Explained

The mortgage preapproval process Utah buyers complete is an essential first step before house hunting.

Here’s how it typically works:

- Submit income documentation

- Provide authorization for credit review

- Review debt and employment history

- Receive a preapproval letter

Many buyers ask how to get pre approved for a home loan first time buyer without feeling overwhelmed. Working with an experienced mortgage broker first time home buyer specialist can simplify the process.

A knowledgeable mortgage broker salt lake city professional may also help compare multiple lenders to secure competitive terms.

Best Mortgage Lenders Utah for First-Time Buyers

Choosing the right lender can significantly impact your experience. If you are researching the best mortgage lenders Utah offers, consider factors such as:

- Loan program variety

- Rate transparency

- Customer service

- First-time buyer support

Some buyers prefer to search for the best mortgage broker in Utah for first time buyers to receive personalized guidance. Brokers often help compare options from different institutions, increasing flexibility.

You may also explore companies labeled as the best mortgage companies for first time buyers, especially those that specialize in educational resources and program guidance.