The Utah housing market is shifting, and in 2026, the traditional path to homeownership is being rewritten. For many residents, securing a Mortgage no longer means walking into a bank with a simple W-2. As the “Silicon Slopes” continue to foster a culture of independence, more buyers are entering the market as self-employed professionals, a 1099 contractors, or a Gig-worker.

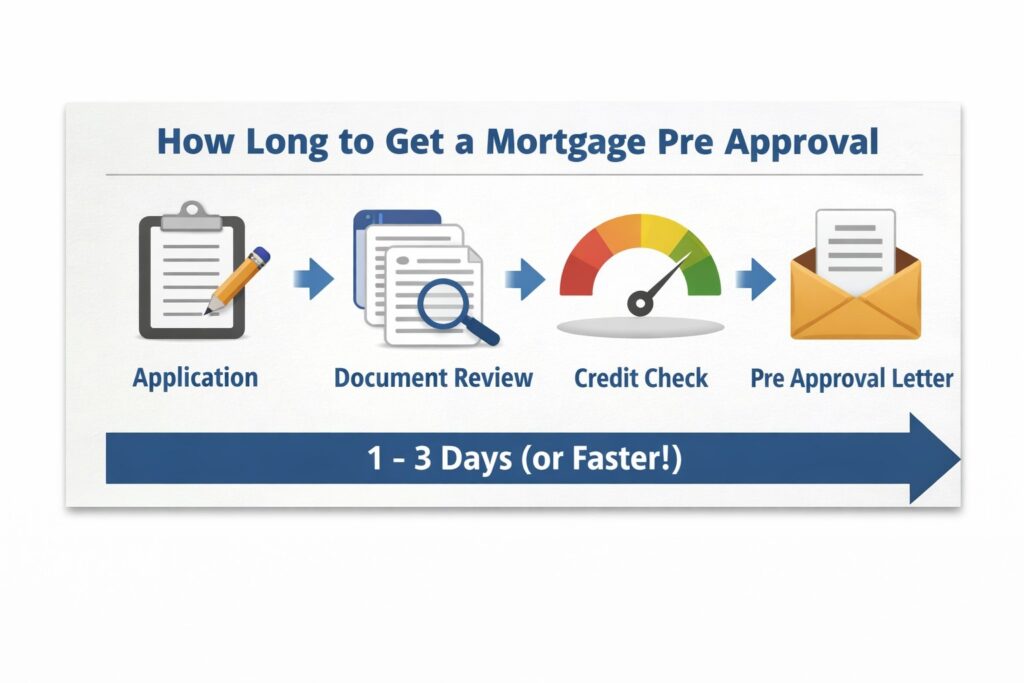

While these roles offer freedom, they often complicate the Pre-approval process. Understanding the specific Eligibility requirements for non-traditional Income is the first step toward moving from a rental to a home you own.

Utah Mortgage Strategies for the Self-Employed and 1099 Earners

For a Self-employed individual, the biggest hurdle is often proving a stable Income when tax write-offs reduce your “on-paper” earnings. In 2026, lenders have become more flexible, offering Bank Statement loans that look at actual deposits rather than net tax figures. This is a game-changer for the Gig-worker who may have multiple revenue streams.

When applying, having a CPA-prepared P&L (Profit and Loss statement) can significantly boost your Credit profile’s credibility. Whether you are looking for a Conventional loan or a government-backed FHA product, documenting your financial health accurately ensures you don’t hit unexpected Limits during underwriting.

First-Time Buyer Grants and Downpayment Assistance

If you are a First-time buyer in Utah, you have access to some of the most aggressive financial Assistance in the nation. The state continues to offer significant Grants and Subsidies designed to bridge the gap between savings and rising home prices.

Currently, a popular Utah program provides up to $20,000 for a Downpayment, which can be applied to newly built Construction. For those with a military background, VA loans remain the gold standard, often requiring $0 down. Similarly, buyers looking at rural or suburban growth boundaries may find that USDA loans offer zero-down Eligibility for those who meet specific household Income benchmarks.

Investor Opportunities and DSCR Loan Limits

The 2026 market isn’t just for primary residents; it’s a prime environment for the savvy Investor. If you are looking to acquire a rental property but want to avoid the strict debt-to-income ratios of a Conforming loan, a DSCR (Debt Service Coverage Ratio) loan is the ideal tool.

DSCR loans qualify the property based on its own potential rental Income rather than your personal salary. This allows investors to bypass traditional Mortgage hurdles, making it easier to build a portfolio of Utah real estate. Even if you are a Veteran investor or a professional with a complex 1099 tax history, these asset-based loans provide a streamlined path to closing.

Refinance and Market Outlook

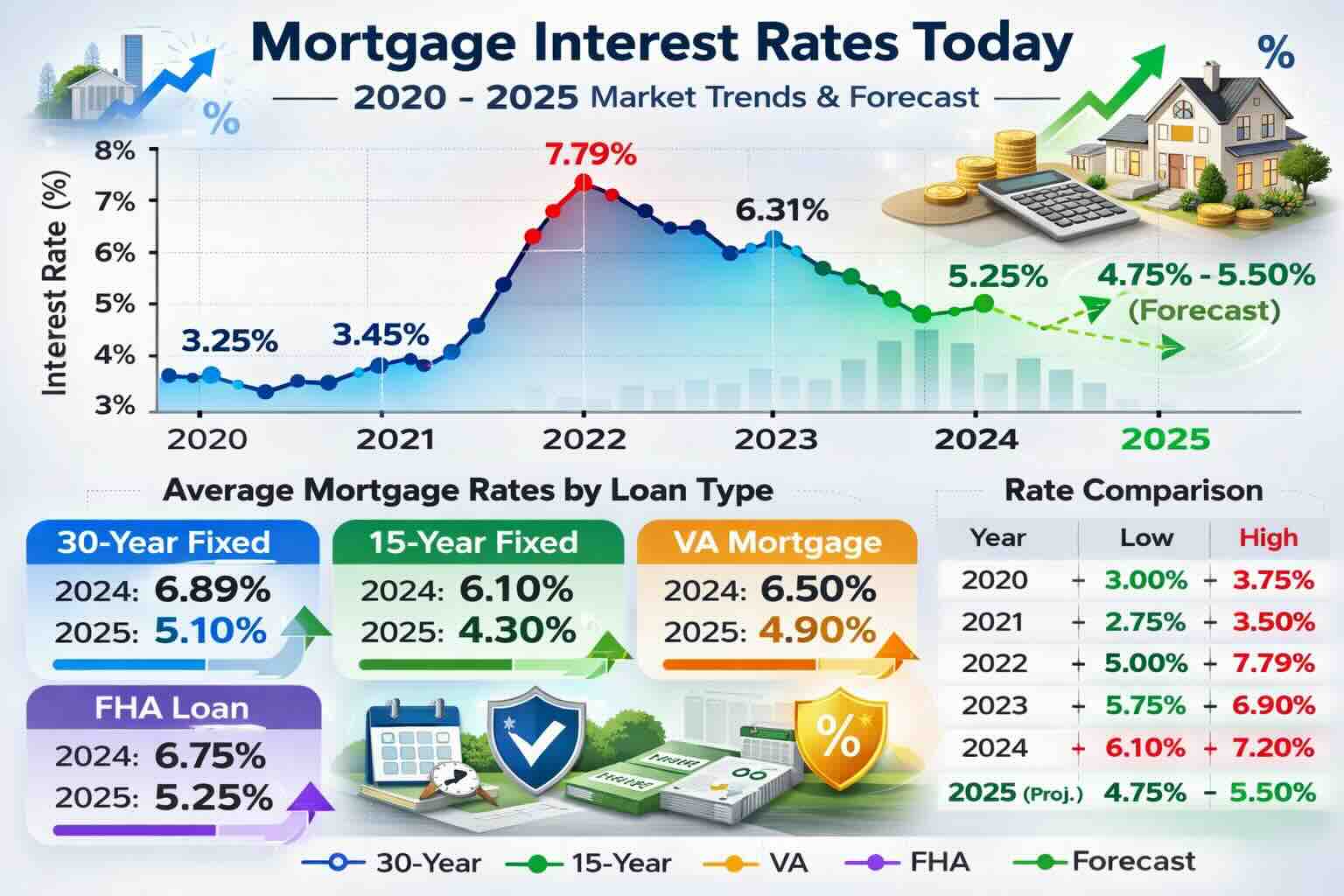

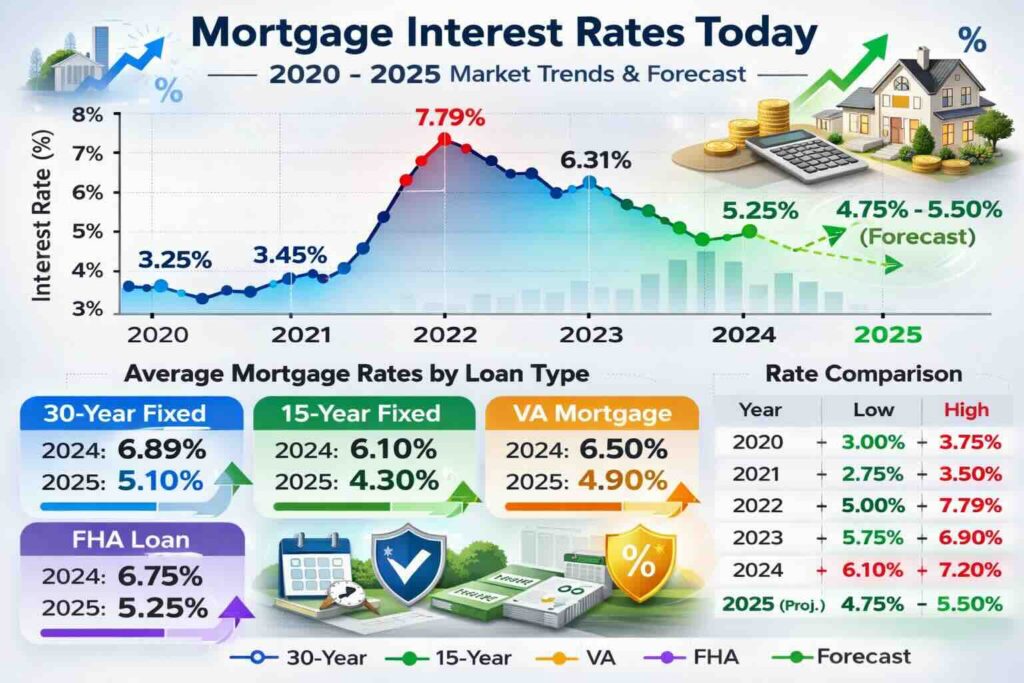

As we move through the year, many homeowners are keeping a close eye on the market to refinance existing high-interest debt. Whether you are looking to lower your monthly payment on a Conventional loan or tap into equity for home improvements, understanding the current Utah rate environment is essential. From the specialized needs of the Self-employed to the broad Assistance available for a First-time buyer, the 2026 housing landscape is built on flexibility. By mastering your Credit and choosing the right loan product—be it FHA, VA, or DSCR—homeownership in the Beehive State is more attainable than ever.